What Happened in India’s PC Market in Q1 2026?

India’s traditional PC market (encompassing desktops, notebooks, and workstations) delivered a standout performance in Q1 2026, with total shipments reaching 4.4 million units, representing 31.1% year-over-year growth, according to IDC’s Worldwide Quarterly Personal Computing Device Tracker. Notably, this marked the third consecutive quarter in which shipments exceeded the 4-million-unit threshold, a milestone that underscores the market’s sustained momentum. The growth came even as PC prices continued to rise due to component shortages. Nonetheless, this reflects strong demand across both consumer and commercial segments, fuelled by digital transformation, enterprise investment, and large-scale education procurement.

Why It Matters

The Q1 2026 results signal the resilience of India’s PC market in the face of structural pricing pressures. Here’s what stakeholders should take away:

- Vendors should limit dependency on education-led demand and monitor the durability of government procurement pipelines. ELCOT was a major volume driver this quarter, but such big volume projects are rare.

- Rising prices are accelerating premiumisation, but they also risk squeezing out price-sensitive buyers in the consumer and SMB segments if unchecked.

Market Dynamics: What Drove the Outcome?

Three converging forces shaped the quarter’s strong performance:

- ELCOT education project led to notebook surge: The execution of the Tamil Nadu government’s ELCOT education procurement programme was the single largest growth catalyst. It drove the education segment to an exceptional 455.2% YoY growth and propelled the overall notebook segment to 3.3 million units, or a 55.4% YoY increase.

- Enterprise investment providing commercial resilience: Sustained domestic and global enterprise spending supported 24.2% YoY growth in the enterprise segment. Workstations, driven by high-performance computing needs in engineering and design, rose 31.8% YoY.

- AI adoption and premium segment expansion: Rising demand for AI-capable notebooks helped drive the premium notebook segment (above US$1,000) up 70.1% YoY. Consumer demand for premium devices outpaced commercial, growing 92.4% versus 56.1% YoY.

Segment Snapshot: Winners and Laggards

Notebooks: 3.3 million units | +55.4% YoY | Majority of total shipments

Workstations: +31.8% YoY | Driven by engineering, design, and data-intensive sectors

Desktops: −13.5% YoY | Elevated prices led to order deferments and cancellations

Premium Notebooks (>US$1,000): +70.1% YoY | Consumer: +92.4% | Commercial: +56.1%

AI Notebooks (total): +96.1% YoY

India PC Market at a Glance: Q1 2026

- Total shipments: 4.4 million units (+31.1% YoY)

- Third consecutive quarter above 4 million units

- Commercial segment: 2.8 million units | Education: +455.2% YoY | Enterprise: +24.2% YoY

- Consumer segment: +11.7% YoY | eTailer: +23.1% YoY | Traditional retail: +8.7% YoY

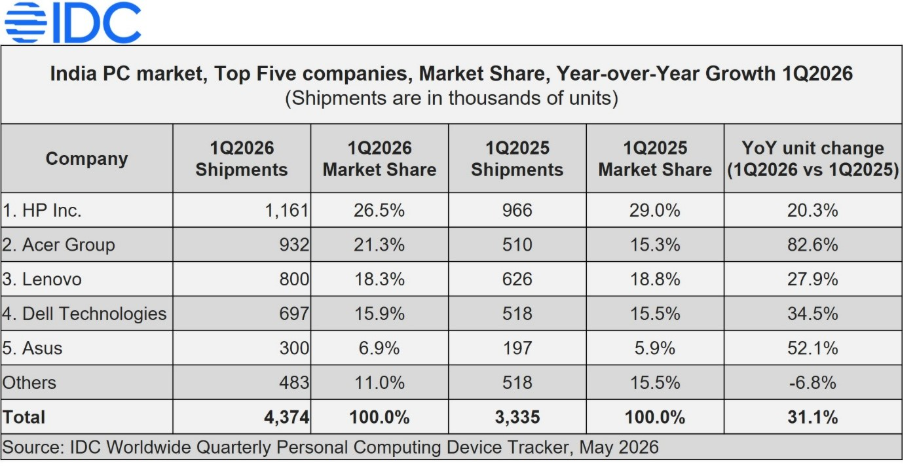

- Top five vendors: HP Inc. (#1), Acer Group (#2), Lenovo (#3), Dell Technologies (#4), ASUS (#5)

Analyst Insight

“Despite persistent upward pressure on PC prices due to rising component costs, particularly DRAM and GPUs, consumer demand has remained resilient. With prices having increased over the past two quarters and expected to rise further in the coming months, proactive and transparent communication from vendors, partners, and channel stakeholders has encouraged early purchase decisions, thereby helping sustain overall market demand.”

— Bharath Shenoy, Research Manager, Devices Research, IDC

Vendor Landscape: Who Won the Quarter?

HP Inc. retained the top spot with 26.6% market share, driven by ELCOT execution and solid enterprise demand (+27% YoY in commercial). Consumer growth was steady at 8.2% YoY, supported by strong large format retail (LFR) traction.

Acer Group surged to second place with 21.3% market share, overtaking both Lenovo and Dell. ELCOT billing in the commercial segment, where it captured 25.5% share, was the key driver. A marginal 1.2% YoY dip in consumer shipments due to entry-level supply constraints was the only blemish.

Lenovo held third with 18.3% market share. Commercial grew 32.3% YoY on enterprise and SMB strength, while consumer grew 20.8% YoY, bolstered by a gaming portfolio surge and e-commerce shipments up 58% YoY.

Dell Technologies ranked fourth at 15.9% market share. Enterprise demand drove a 37.5% YoY segment increase, with overall commercial growing 38.7% YoY partly from ELCOT fulfilment. Consumer shipments grew 17% YoY despite pricing pressures.

ASUS rounded out the top five at 6.9% market share. Gaming notebook demand lifted consumer growth 31.9% YoY, and an exceptional 241.1% YoY commercial surge reflected rising SMB momentum.

IDC Outlook: What’s Next?

The first half of 2026 is expected to sustain positive momentum, supported by favourable supply allocations, aggressive channel stocking, and front-loaded procurement ahead of anticipated price hikes. However, the second half presents a more cautious picture.

- What could sustain growth? Strong enterprise and SMB pipelines would drive 2Q 2026, continued AI notebook adoption, and successful rollout of products like Apple’s mass-market MacBook Neo (launched March 2026) might be some positive drivers for 2H 2026.

- What could slow it down? Inventory corrections in Tier 1 and Tier 2 channels, supply-side constraints, rising DRAM and GPU costs, and budget pressures in government and education segments.

- What should readers watch next quarter? Whether channel inventory levels normalise, how consumer demand responds to further price increases, and the pace of AI notebook adoption in SMBs.

“Vendors have so far benefited from favourable supply allocations and are currently managing relatively high inventory levels across Tier 1 and Tier 2 channels. While enterprise and SMB segments continue to support volume-led procurement, shipments might decline in second half of the year. The government and education sectors could face challenges amid rising device prices and constrained budget allocations. The consumer segment may also witness a decline in the second half of the year unless pricing stabilizes. At the same time, Apple’s launch of the mass-market-focused MacBook Neo in March is expected to strengthen its position and potentially expand its presence across both consumer and SMB segments.”

— Navkendar Singh, AVP, Devices Research, IDC

Frequently Asked Questions

Why did the PC market grow so strongly despite rising prices?

The primary catalyst was the ELCOT education procurement project, which alone drove the education segment up 455.2% YoY and turbocharged notebook shipments. This institutional demand, combined with enterprise investments and early purchasing by both enterprises and consumers ahead of further price increases, more than offset the headwinds from elevated pricing.

What risks could impact the PC market in 2026?

The key risks include prolonged component cost inflation (especially DRAM and GPUs), potential inventory overhang in distribution channels, and weakening budget availability in government and education. If prices continue to climb, consumer spending moderation could also temper growth.

About IDC

International Data Corporation (IDC) is the premier global provider of trusted technology intelligence, advisory services, and events. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 100 countries. IDC’s analysis and insights help IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. To learn more about IDC, please visit www.idc.com. Follow IDC Asia/Pacific on X at @IDCAP and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

All product and company names may be trademarks or registered trademarks of their respective holders.

For more information, contact Bharath Shenoy, Research Manager — Devices Research, or Navkendar Singh, AVP – Devices Research.