The story being written by the AI market is extraordinary by almost any measure. OpenAI’s revenue grew from $2 billion in 2023 to $20 billion in 2025. Anthropic’s annualized revenue run rate surged from $87 million in January 2024 to $30 billion by April 2026, a trajectory that Salesforce took 20 years to achieve. NVIDIA’s revenue grew eightfold from $27 billion to over $216 billion between 2023 and 2026, achieving that growth in just one-third of the time it took Apple to do so during its heyday between 2007 and 2015. By nearly every reported metric, the AI market is delivering growth at a scale and speed that defies historical comparison.

Yet a narrative has emerged about how much of that growth reflects genuine market demand and how much reflects the circular financing structures that have become a defining feature of AI infrastructure investment. Circular financing in AI describes investment structures where the same capital flows simultaneously as vendor payment and equity stake. A company funds its own customer’s revenue while also supplying that customer’s core infrastructure. The result is reported revenue growth that is real but not cleanly separable from investment activity. The answer matters enormously, not just for investors in AI infrastructure companies, but for every enterprise software vendor and technology buyer trying to make sense of what’s actually happening in the market.

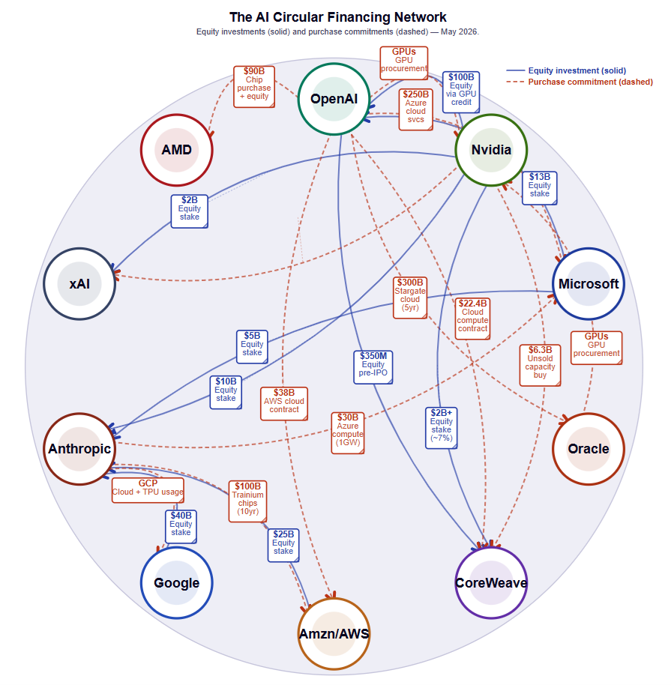

Without getting into any financial analysis of the diagram below, I include it simply to demonstrate the extreme complexity and circular nature of these financial relationships.

Figure 1:

The circular financing problem

Circular financing in AI works through a self-reinforcing loop. NVIDIA committed $30B as part of OpenAI’s $110B financing announced in February 2026, while simultaneously serving as OpenAI’s primary GPU supplier, making it both a major investor in and a vendor to the same company. NVIDIA simultaneously holds equity in CoreWeave, which supplies infrastructure to Oracle, which signed a $300 billion Stargate commitment with OpenAI. Microsoft has invested more than $13 billion in OpenAI while serving as its primary cloud provider, meaning a substantial portion of OpenAI’s rapidly escalating compute spend flows back into Azure revenue. Microsoft has disclosed more than $600 billion in AI-driven remaining performance obligations, of which management confirmed approximately 45% is attributable to OpenAI-related activity. These are just some of the interdependencies that exist, and while they do not make the revenue fabricated, they do make it very difficult to read reported growth figures as clear evidence of external market demand expanding at the rates that match recent headlines.

Stripping out circular flows to estimate genuine arm’s-length revenue is nearly impossible from the outside because none of these companies has any incentive to disaggregate them. What is clear is that OpenAI’s compute costs, projected to reach tens of billions annually, still dramatically exceed its current revenue. While their internal projections point to massive revenue growth over the longer term, the company is expected to remain unprofitable through at least 2029, with positive cash flow not expected until 2030. The infrastructure layer is being built on a combination of genuine demand and financial engineering, and the two are not currently separable from reported figures alone.

Why the application layer is the real signal

This is why revenue growth on the enterprise application layer has become the most important signal in the entire AI market. Enterprise application software does not carry a circularity problem. When an ERP vendor reports AI-driven ARR expansion, when an HCM platform demonstrates higher attach rates on AI-enabled capabilities, when a finance or procurement solution delivers measurable process efficiency gains that a CFO chooses to fund again at renewal, those signals reflect real buyers making real budget decisions based on perceived business value. There is no investment web distorting the demand signal. The revenue either reflects a genuine willingness to pay for demonstrated outcomes, or it does not.

What’s interesting is that we’ve seen this same exact pattern play out multiple times before during historical tech market revolutions. In each of the last several significant platform transitions, the application layer lagged the infrastructure layer in value creation, but eventually surpassed it as the platform matured.

The historical pattern

During the internet buildout, infrastructure companies captured the overwhelming share of market value. Cisco dominated with networking equipment and briefly became the most valuable company on earth, reaching a market cap of nearly $560 billion in March 2000. Companies like Sun Microsystems and Dell supplied servers, and even fiber optic cable makers like Corning and JDS Uniphase had their moment. Meanwhile, the application layer was largely characterized by money-losing dot-com ventures that collapsed when the bubble burst. But over the long term, application layer players like Amazon, Salesforce, and Google eventually dwarfed those companies.

The cloud era was no different. AWS launched in 2006 and, for years, held a dominant share of the cloud market, while enterprise SaaS applications were still proving their business model viability. IDC’s Worldwide Semiannual Public Cloud Services Tracker shows that by 2020, the SaaS application layer had grown to $148 billion in revenue, nearly half of the total $312 billion public cloud market, while IaaS, despite its faster growth rate, remained a significantly smaller share of the overall pie. Once the cloud infrastructure platform matured, value creation in the application layer far exceeded it.

Looking at the current AI boom, it’s following the same early-stage script. NVIDIA first became the world’s most valuable company in mid-2024, and we are in the middle of an AI infrastructure super cycle with trillions of dollars flowing into compute, datacenter construction, and power generation. Meanwhile, enterprise AI application revenues remain nascent relative to the trillions being invested in the infrastructure layer beneath them.

Agentic AI is triggering a fundamental reconsideration of how companies invest in packaged software, as AI agents effectively become the new enterprise apps. IDC’s spending forecasts project AI investment growing 31.9% annually between 2025 and 2029, reaching $1.3 trillion. These are real demand signals, and they are large enough to sustain significant growth at the application layer if enterprise software vendors can connect their AI capabilities to the business outcomes buyers are seeking.

The monetization gap that still needs closing

The monetization gap, however, remains significant and is not yet closing at the pace the market requires. IDC’s Future Enterprise Resiliency and Spending Survey (FERS) finds that few organizations report measurable financial results from their AI projects, despite widespread improvements in individual productivity. While most organizations aspire to grow revenue through AI initiatives, the majority have yet to achieve that goal. This distinction between individual productivity gains and organizational-level financial outcomes is one that enterprise software vendors have been slow to confront directly. Productivity at the individual level is real, documented, and genuinely valuable. Translating those gains into measurable business results that justify enterprise software pricing premiums is a fundamentally different challenge, and one that buyers are increasingly demanding vendors address more explicitly during renewal and contract-expansion discussions.

What vendors must do now

Closing that gap is the defining commercial challenge for enterprise software vendors over the next 12 months. The most urgent shift is from feature availability to outcome accountability: specific, auditable improvements in process efficiency or cost reduction that survive CFO scrutiny at renewal. Transparent commercial models follow from that. If buyers have to build the business case themselves, or fund significant professional services to reach value, adoption curves will flatten and renewal risk will rise. The competitive differentiator in this environment is not model sophistication. It is workflow transformation. Enterprises evaluate software on whether it changes the workflows that actually drive their business.

The infrastructure layer of the AI market may ultimately prove resilient. The circular financing dynamics, while real, are not unlike the capital formation structures that funded prior technology infrastructure buildouts, and genuine demand for compute at scale is not in dispute. The application layer is not a downstream beneficiary of the AI infrastructure boom. It is the proof point on which the entire narrative depends.