Artificial intelligence is no longer a future promise; it’s an economic force actively reshaping industries, workforces, and GDP projections around the world. While AI is expected to lead to major workforce transformation in the next five years, the timeline remains uncertain, as organizations continue to struggle with identifying optimal use cases and measurable business outcomes. Despite widespread predictions that AI will replace jobs, there’s little evidence of this happening yet at large scale, and the greater productivity benefits may come through replacing work instead of workers.

Here are the key takeaways of this year’s report on the Economic Impact of AI.

The big story: Investment is driven by projected economic impact

We’re heading into what is projected to be a ‘second wave’ of AI-driven IT spending in 2027, whereby AI investment drives overall technology spend to levels last seen in the mid-1990s.

Worldwide IT spending grew by more than 14% in 2025, mostly driven by service provider spending on AI infrastructure. Service providers continue to invest aggressively, but the ‘second wave’ is an expected surge in enterprise spending on use cases tied to agentic AI. Business IT budgets are forecast to increase at the fastest rate in almost 30 years.

This coming wave is dependent on the economic impact which organizations are anticipating. There are important caveats here: so far, this planned investment is largely supported by expected productivity gains, which will depend on measurable business outcomes.

Many business leaders report spending which is at least partly driven by FOMO (fear of missing out). There are gaps in AI maturity which many organizations need to bridge in the next 6-12 months.

At the beginning of 2026, IDC called this a ‘year of reckoning’ for the global economy and AI. Economic growth and AI are now closely linked, with AI having been largely responsible for stable GDP growth in the past two years, especially in the US and China. With inflation challenging the economics of AI in 2026, there are downside risks.

But if the current rate of adoption continues, and if measurable business outcomes support IT spending, AI will drive a productivity reset, global workforce transformation, and more than $22 trillion in value by 2031.

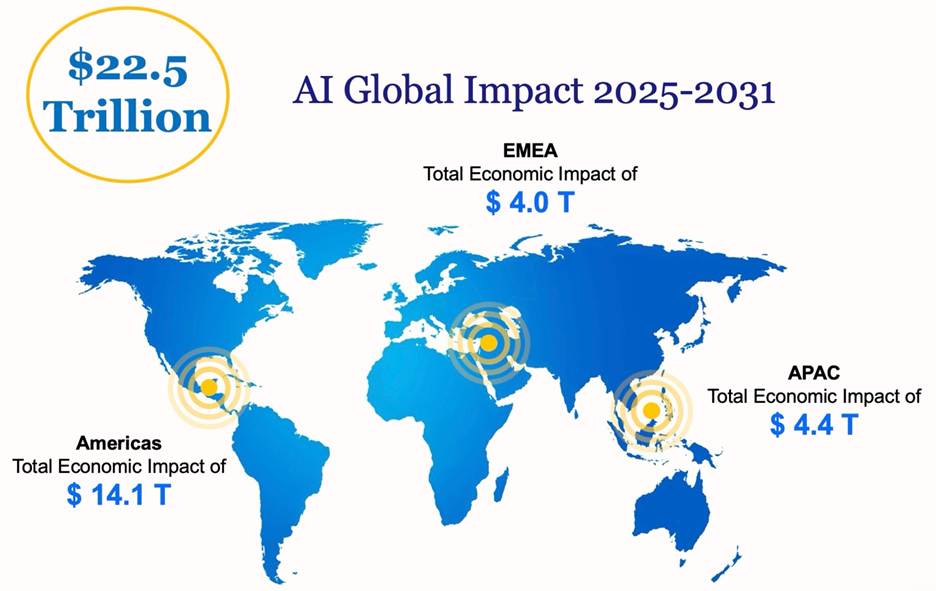

The big number: $22.5 trillion in cumulative value by 2031

Under the baseline scenario, AI is projected to generate $22.5 trillion in cumulative economic value between 2025 and 2031, a compound annual growth rate of 35.6%. Even in a constrained, downside scenario (factoring in geopolitical shocks, regulatory friction, and slower enterprise adoption), the figure stands at $18.1 trillion. In an accelerated, high-growth scenario, it climbs to $24.5 trillion.

These aren’t abstract figures. They reflect real flows across direct AI revenues, supply chain effects, and the induced economic activity that follows as workers and households benefit from productivity gains.

The economic impact breaks down regionally:

- Americas: $14.1 trillion: more than 60% of global impact, driven by U.S. dominance in hyperscalers, foundation models, and semiconductors.

- Asia/Pacific: $4.4 trillion: the fastest-scaling region, with China as a supply engine and advanced markets like Japan, Korea, and Singapore driving enterprise innovation.

- EMEA: $4.0 trillion: Europe setting the regulatory gold standard via the EU AI Act, while the Middle East (UAE and Saudi Arabia in particular) emerges as a new growth engine.

For all the headline numbers, AI’s impact on macroeconomic data remains difficult to isolate so far. We’re only now moving from survey-based assessments of AI impact to the point where measurable divergence from historical trends should become visible in the next 12 months.

What’s changing the calculus is agentic AI. Unlike earlier waves of AI, agents can perform complex, multi-step tasks with minimal human intervention, cutting inefficiencies from business workflows at a scale that prior automation tools never achieved. IT buyers anticipate savings in operating costs as a result of deploying AI-driven automation.

The risks are real, and largely external

The report identifies four major wildcards that could disrupt the timeline for AI-driven value creation:

1. Geopolitics and trade fragmentation. Export controls on semiconductors are already reshaping supply chains. If tensions escalate, access to critical AI hardware becomes unpredictable for both businesses and governments.

2. Energy infrastructure. AI’s power demands are outpacing grid capacity. Electricity availability is becoming a genuine bottleneck for datacenter expansion, and a strategic variable that no serious AI roadmap can ignore.

3. The workforce skills gap. The demand for professionals skilled in AI development, deployment, and governance is growing faster than training programs can respond. Reskilling is now as critical as infrastructure.

4. Governance lagging adoption. Fewer than one-third of businesses have fully implemented AI governance structures. With regulatory approaches diverging sharply between the EU and the U.S., multinational organizations face a genuinely complex compliance landscape.

AI is replacing work, not workers (for now)

The headline finding is straightforward: there is no evidence in official unemployment data of AI driving meaningful job displacement. US unemployment remains near historic lows.

But the absence of mass job replacement is not the same as business as usual. What’s happening, and will accelerate, is workforce transformation: a shift away from routine tasks toward non-routine cognitive and interpersonal work.

This shift has been underway for decades and largely tied to IT spending. Routine tasks fell from roughly 60–65% of employment in 1960 to around 40–45% by 2020. AI doesn’t create a new direction, but it dramatically accelerates the trajectory. We project routine tasks falling further to around 30% of employment by 2031.

The report uses software development as a concrete example: AI can largely automate routine coding and documentation (up to 70% task-time reduction), while testing and architecture work is augmented rather than replaced. Developers who adapt will spend more time on strategic, judgment-intensive work, which is ultimately where the value lies.

What this means for IT vendors: Three imperatives

IT vendors must engage urgently with the following strategic directions:

1. Capture short-term revenue through agentic AI

The highest-impact near-term opportunity lies in AI agents, at the task level, within workflows, and across applications. Products need to reflect rapidly evolving use cases and help customers achieve economic impact at scale, not just run pilots.

2. Invest in long-term customer success

Knowledge transfer matters more than support contracts. IT buyers need help with change management, upskilling, and realizing genuine business outcomes from agentic AI. If end-users can’t achieve economic benefits at scale, investment momentum will stall.

3. Accept responsibility for AI stewardship

The societal implications of widespread AI adoption are profound. Vendors that proactively engage with policymakers and business leaders, guiding toward outcomes that unlock human potential rather than simply automate it, will be better positioned for long-term relevance and trust.

The bottom line

The updated 2026 report paints a picture of an AI economy that is large, accelerating, and uncertain in its timing. The $22.5 trillion increase in economic value is not a guarantee; it depends on organizations moving from pilot projects to scaled deployment, on energy and skills infrastructure keeping pace, and on governance frameworks that enable rather than obstruct innovation.

What is clear: the businesses and vendors that treat AI as a strategic priority, investing in workforce transformation, change management, and responsible deployment, will be best positioned to capture the upside, even if the timeline is disrupted. Those that wait for certainty may find the window for competitive differentiation has already closed.