Cutting Through the Noise with a Clear, Side-by-Side View of Performance

Starting with their 1Q25 results, IDC’s European Enterprise Communications Services program will publish a quarterly comparison and analysis of Europe’s top 5 telcos: BT, Deutsche Telekom, Orange, Telefónica, and Vodafone. A main goal of this initiative is to identify which telcos are most successful in transforming their monetization strategies.

Our analysis of telco performance will be based on new research by the IDC European analyst team. Other IDC products, including those from our colleagues in the Data & Analytics team, focus on telco revenue across individual product lines.

This blog post provides a high-level view of the operators’ 2024 global performance as a prelude to the quarterly analyses. Here, we compare the companies’ revenue performance, development of their geographical markets and strategic growth portfolios, and major announcements and events during the period.

The financial data has been adjusted for consistency and comparability:

- Figures have been converted to USD on a constant currency basis at IDC’s published 2024 rate (EUR/USD 0.92420; GBP/USD 0.78269).

- Reporting periods have been aligned to the calendar year (CY). For Deutsche Telekom, Orange, and Telefónica, this aligns to their financial year (FY). For BT and Vodafone, we have summed their quarterly results within each CY (e.g., CY 1Q24 to CY 4Q24, corresponding to their published FY 4Q24 to FY 3Q25 reports).

Group Revenue Performance

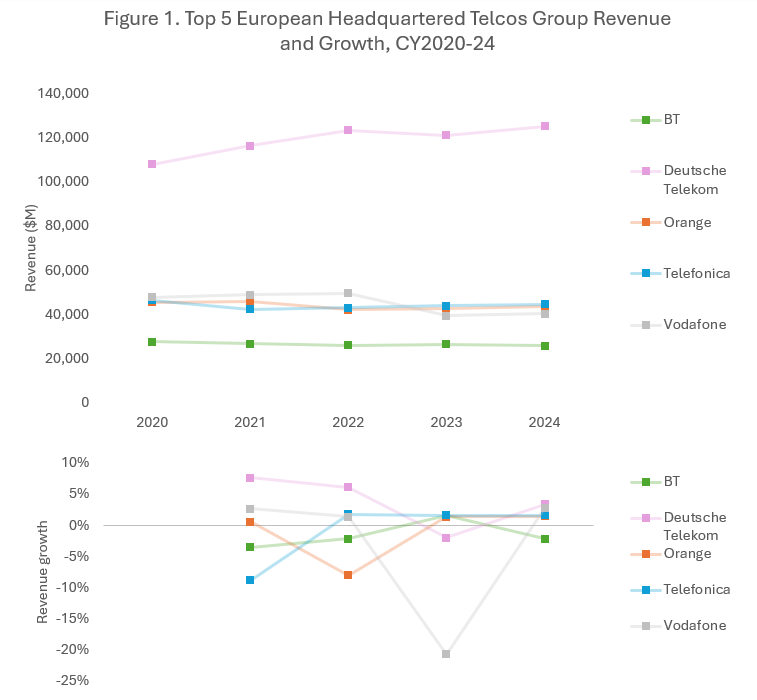

Figure 1 shows total group revenue and YoY growth for BT, Deutsche Telekom, Orange, Telefónica, and Vodafone from CY20 to CY24.

Converting all results to USD and aligning BT and Vodafone to CYs highlights the relative size differences between Deutsche Telekom (due to T-Mobile US) and BT, and the similarity between Orange, Telefónica, and Vodafone.

It also shows that CY24, like CY23, was relatively flat for Europe’s leading telcos, with top line growth between -2.2% and 3.4%. The exception is Vodafone, which posted a large decline in CY23 due to the disposal of two major country operations during 2024 (Vodafone Italy and Vodafone Spain). Vodafone’s restated historical financials omit Italy and Spain going back to CY 1Q23. As the figures presented in this blog post are based on the restated numbers, the drop in revenue resulting from those disposals appears to occur in CY23.

Notes:

- BT and Vodafone figures are for the CY, based on quarterly reports.

- Growth rates reflect operators’ reported figures and include conversion from local currency to reporting currency (EUR for Deutsche Telekom, Orange, Telefónica, and Vodafone, and GBP for BT).

- Vodafone’s negative growth in CY23 is due to the disposal of Vodafone Italy and Vodafone Spain in CY24 and subsequent revenue restatements.

- BT remains the smallest of the top five telcos by revenue and in growth terms has been a mid-pack performer in recent years, although it was the only company in the group to post negative top-line growth in CY24, of -2.2%. In addition to several country operation disposals over the last few years, BT has signalled its clear intent through CY24 under CEO Allison Kirkby to focus on the domestic U.K. market and is exploring options for its underperforming international business.

- Deutsche Telekom is far ahead of its European peers in total revenue due to the contribution of T-Mobile US, with group revenue between $114B and $125B. However, revenue from Europe totaled €41.2B in CY24, placing it in line with Orange, Telefónica, and Vodafone (see figure 5 for side -by -side view for the 4 operators). Deutsche Telekom posted the highest YoY growth rate in CY24 at 3.4%, largely driven by the strong performance of its mobile and broadband services. Notably, this growth is primarily attributed to T-Mobile US, fueled by rising postpaid and prepaid revenues and a slight increase in terminal equipment sales. The contribution of approximately 65% of group revenue from T-Mobile US clearly sets Deutsche Telekom apart.

- Orange’s YoY revenue growth in CY24 was limited to 1.5%, mainly due to the deconsolidation of Orange Spain after the creation of the MásOrange joint venture, and a decline in Orange Business’ revenue of -1.9%, primarily from fixed services. However, strong growth from the META region of 7.4% stabilized Orange’s overall business.

- Telefónica, which ranks second in group revenue, reported modest YoY growth of 1.6% in CY24. This was due to growth in service revenues (up 2.5%) driven by a stronger B2B performance (up 4.8%) but offset in part by the depreciation of various Latin American currencies (in particular the Brazilian real) against the euro.

- Vodafone, from CY20 to CY22 Vodafone was ahead of, and accelerating away from, Orange and Telefónica. However, the disposal of its Italy and Spain operations meant a loss of over $8 billion annual revenue, effective in its restated financials from 2023. This resizes Vodafone below Orange and Telefonica but, as of CY2024, it remains on a higher growth trajectory. Vodafone completed the sale of its Spain operation (to Zegona Communications) in May 2024 for €5 billion and its Italy operation in January 2025 (to Swisscom) for €8 billion. Around the same time it received regulatory approval for its merger with Three in the U.K.

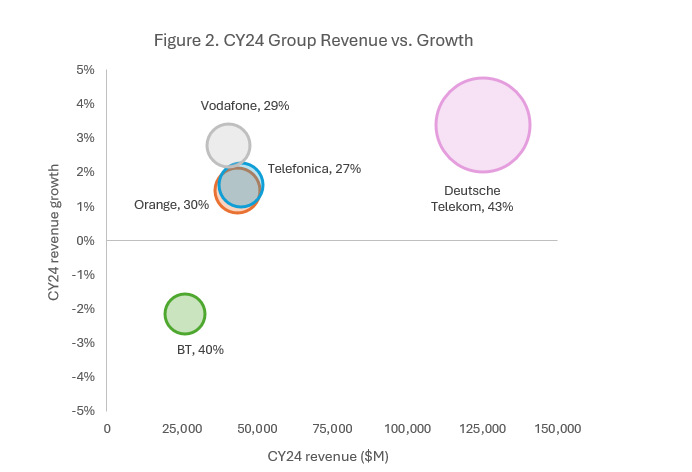

Figure 2 positions the operators based on their CY24 group revenue and growth rate over CY23, with bubble sizes representing the absolute EBITDA or EBITDAaL (EBITDA after leases) values for CY24. It brings out the similarity of Orange and Telefónica’s businesses in terms of all three metrics (size, growth, and EBITDA). Deutsche Telekom and BT, while differing significantly in both revenue and growth, show nearly identical EBITDA margins—43% and 40% respectively—indicating comparable efficiency in generating operating profit.

Notes:

- Size of bubble refers to the value of CY24 EBITDA (BT, Deutsche Telekom, and Telefónica) or EBITDAaL (Orange and Vodafone).

- The percentages next to operator’s name plotted on the chart represent the EBITDA margin for (BT, Deutsche Telekom, and Telefónica) or EBITDAaL margin (Orange and Vodafone).

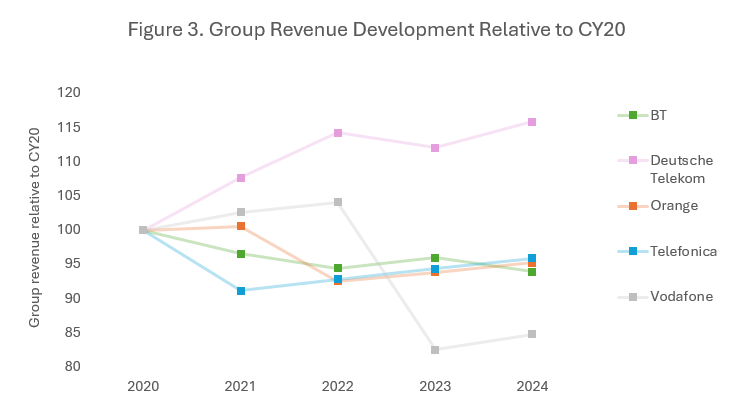

Figure 3 rebases each operator’s group revenue to a value of 100 in CY20 and plots relative development from that point. This clearly shows Deutsche Telekom’s outperformance over the others, the similar relative performance of BT, Orange, and Telefónica over the last three years, and again the temporary drop in Vodafone’s revenue due to major disposals.

Notes:

- Revenue is plotted relative to a baseline of 100 for all operators in CY20.

- Vodafone’s negative growth in CY2023 is due to the disposal of Vodafone Italy and Vodafone Spain in CY2024 and subsequent revenue restatements.

Geographical Markets

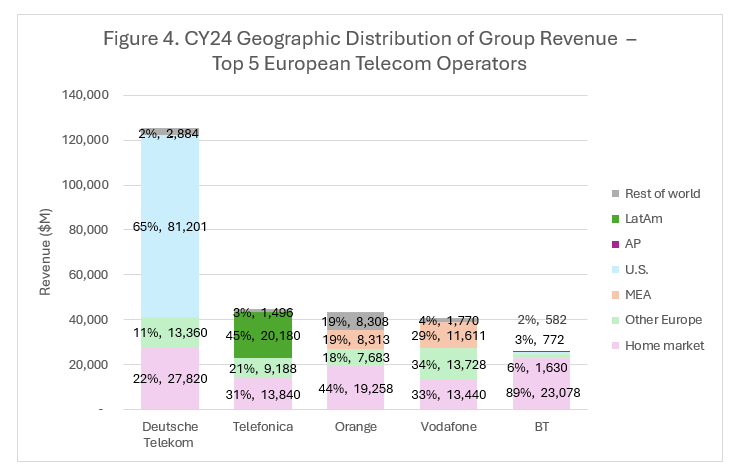

Figure 4 shows how operators’ total CY24 revenue breaks down geographically. Each operator’s domestic operations are labeled as its home market on the chart. For Vodafone, we assigned its largest country market of Germany as, not being an ex-incumbent, the concept of home market is less clearly defined.

The chart highlights how international businesses, primarily opcos, gained via historical acquisitions, are a sizeable fraction of each operator’s total business. The exception is BT. Following a series of divestments in recent years, BT is now very heavily concentrated on the U.K., contributing 89% of group revenue in FY24 (the year ending March 2024, BT’s most recent geographical reporting). BT CEO Allison Kirkby’s decision to focus on the U.K. still further is an extension of a trend already well established.

Notes:

- Vodafone’s home market is assigned as Germany, its largest revenue-contributing market.

- BT does not publish geographical splits on a quarterly basis, so CY splits are unavailable. We applied the latest published breakdown (year ending March 2024) to CY24 revenue for illustration.

- The chart is organized in descending order of group revenue, progressing from the highest to the lowest value along the horizontal axis.

- The percentage shows each region’s share of the overall group revenue, and the number shows the total revenue that region produced in CY24.

B2B Revenue Performance

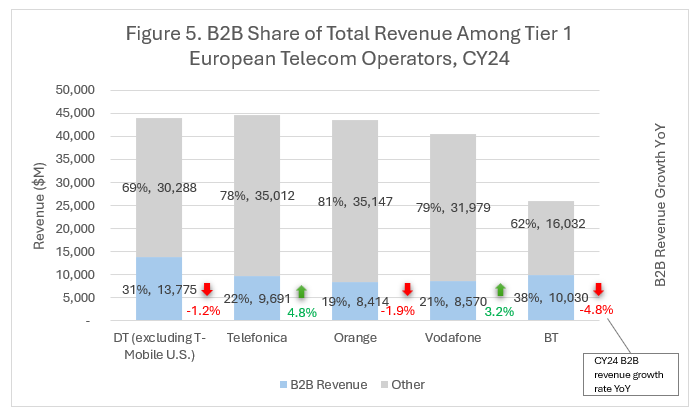

Figure 5 shows how operators’ CY24 revenue from business customers compares with total group revenue. We aimed to capture all B2B revenue, including dedicated enterprise units (BT Business, Deutsche Telekom’s System Solutions/T-Systems, Orange Business, Telefónica Tech, and Vodafone Business), as well as other reported business revenue generated by the group organization. In practice, some very small business customers buy consumer products and are served by the consumer division of an operator. We don’t attempt to break out this revenue.

Notes:

- Growth rates shown in red (decline) and green (growth) refer to CY24 B2B revenue growth.

- Figures represent overall B2B revenue, including enterprise business units and services sold to business customers by the parent organization.

- The chart is organized in descending order of CY24 group revenue, with operators arranged left to right from highest to lowest.

- Deutsche Telekom (DT) is placed first as it recorded the highest total revenue in CY24. However, in this graph T-Mobile US has been excluded from DT’s revenue in this analysis, as the company does not report a segmented B2B vs B2C revenue breakdown for the U.S. market. This exclusion ensures a more accurate and consistent comparison of DT’s European B2B revenue contribution.

Deutsche Telekom

Deutsche Telekom’s B2B revenue comes from the summation of two segments: German Business Customers and Systems Solutions (T-Systems). Deutsche Telekom serves enterprise clients globally, but only these two components are reported in the operator’s annual statements. German Business Customers, part of Deutsche Telekom’s Germany segment, generated €8.7B in CY24, down 5.7% YoY (mainly due to reclassification of some revenue as wholesale since January 2024).

Systems Solutions, operating under the T-Systems brand, focuses on ICT services in the DACH region, spanning cloud, digital, security, and advisory services as well as road toll systems. Revenue rose to €4.0B in CY24, up 2.8% YoY, reflecting steady strategic growth.

System Solutions’ growth was driven by:

• Expanding demand for digital, cloud, and road charging services

• Strong momentum in public sector IT contracts, a key vertical for T-Systems

• Ongoing customer migration from legacy infrastructure to digital platforms

Despite ongoing pressure in traditional services, the gains in high-growth areas allowed Systems Solutions to post a 3.7% increase in external revenue and a 2.3% rise in service revenue, signaling healthy market traction and improved portfolio relevance.

The overall YoY revenue decline of -1.2% shown in figure 5 for Deutsche Telekom is the result of growth in its System Solutions segment being offset by a decline in revenue from its German business segment. Together they represent 31% of DT total revenue of $44,063063M excluding the U.S. region.

Telefónica

Telefónica Tech (TTech) is the digital services arm within Telefónica’s broader B2B segment. It focuses on services such as cloud, cybersecurity, IoT and Big Data, and AI and automation, while the B2B segment overall includes traditional connectivity and managed services. In CY24, TTech generated €2,065M in revenue, growing 10% YoY and contributing to total B2B revenue of €8,957M, up 4.8% YoY.

Main B2B growth drivers included:

• Bookings and commercial funnel growing at 30% YoY and 15% respectively in CY24

• Enhanced business sustainability and larger, higher-value projects in the backlog

TTech’s cybersecurity and cloud revenue amounted to €1,821M (up 12.3% YoY), and its IoT and data revenue totaled €246M (down 4.8% YoY) in CY24.

Orange

Orange Business contributed 19% of Orange’s total revenue in CY24, at €7.8B, down 1.9% YoY due to the decline in fixed service revenues. Although declining modestly, the segment demonstrated strategic resilience and a relative shift toward higher-value digital services.

B2B growth was driven by:

• IT and integration services, up slightly (by 2.7% comparable growth, or €102M) in a complex IT market

• Orange Cyberdefense (part of IT services), up 11.2% or €120M

Despite ongoing pressure on legacy product lines and equipment sales, positive momentum in IT and mobile segments demonstrates good portfolio realignment and robust underlying market traction.

Vodafone

Enterprise customers of all sizes are handled through Vodafone Business. The unit reports service (as opposed to total) revenue, which amounted to €7.9 billion in CY24, 21% of (total) group revenue. This was up 3.2% on CY23 (based on restated figures that exclude Italy and Spain), making Vodafone one of only two telcos in the group to be growing its B2B business.

Vodafone’s B2B growth drivers include:

• Strong demand for digital services (cloud, security, and IoT), particularly in the MEA region. Cloud revenue grew 25% YoY on average per quarter, and digital services grew from 17% of total business service revenue at the start of CY24 to 20% by the end.

• Demand for fixed connectivity, again particularly in MEA.

• Project work, often in the public sector, in some markets including the U.K.

Against the growth in digital services and fixed connectivity, Vodafone’s B2B mobile business was challenged during the year, from falling inflation-linked price increases as well as ARPU erosion during large contract renewals, notably in Germany.

BT

BT Business, the merger of the former U.K.-focused BT Enterprise with BT Global, accounted for 38% of BT’s total revenue in CY24. While this is a higher relative contribution than the other operators, and in absolute terms is larger than Telefonica, Orange, and Vodafone, the unit has underperformed for several years, being 23% smaller at the end of CY24 compared with the start of CY20.

There are few positive growth drivers to report, with most B2B segments in decline. U.K. SMB was a relatively strong performer up to CY24 but growth has since flattened and turned negative. The U.K. CPS (corporate and public sector) business, conversely, has turned from strongly negative to broadly stable in CY24.

In terms of service offerings, security is a consistent growth area, and BT is betting on its global NaaS platform, Global Fabric, to revitalize its B2B portfolio and boost its international business over the next few years. The first customer went live on Global Fabric in March 2025 and the roadmap sees many of BT’s network services being offered via the platform over the next two years.

Major Announcements and Events

These are some of the main revenue-impacting developments by operator during CY24:

BT

- December 2024: BT Group signed a new £1.29B contract with the U.K. Home Office to deliver mobile services for the government’s Emergency Services Network, aiming to enhance communication capabilities for emergency responders.

- November 2024: Reports, later confirmed by BT, suggested that the company was looking at options for its international business following a long period of underperformance globally and a strategic focus on the U.K. market.

- August 2024: Indian Bharti Enterprises agreed to purchase a 24.5% stake in BT Group from Altice, making Bharti the largest shareholder in BT.

- February 2024: BT Group welcomed Allison Kirkby as its CEO, the first woman to lead the U.K. telecom giant.

Deutsche Telekom

- November 2024: Deutsche Telekom awarded Nokia a contract to roll out a large-scale commercial Open Radio Access Network (O-RAN) across more than 3,000 sites in Germany, supporting the operator’s strategy to diversify its supplier base and enhance network efficiency.

- July 2024: Deutsche Telekom’s U.S. subsidiary T-Mobile US announced a joint venture with KKR to acquire fiber ISP Metronet. T-Mobile is investing about $4.9 billion for a 50% stake in the JV, which will absorb Metronet’s two million FTTH customers across 17 states.

Orange

- May 2024: Orange announced the completion of the merger between Orange Romania SA and Orange Romania Communications SA as of June 1, 2024.

- March 2024: Orange and MásMóvil completed the creation of a 50:50 JV valued at €18.6 billion in Spain, combining their operations to form a leading operator in terms of customers.

- February 2024, Orange SA exited the retail banking business, after years of losses, by transferring its Orange Bank customers to BNP Paribas.

Telefónica

- November 2024: The Spanish government approved Saudi Arabian STC Group’s acquisition of a 9.9% stake in Telefónica, allowing STC to appoint a board member, with conditions to safeguard national interests.

- July 2024: Telefónica and Vodafone Spain (now owned by Zegona) agreed to form a joint fiber venture in Spain. The non-binding MOU outlines plans to combine and expand FTTH networks to cover ~3.5 million premises.

- February 2024: Telefónica finalized an agreement to sell its Telefónica Argentina unit for about $1.245B to Telecom Argentina.

Vodafone

- December 2024: Vodafone Group’s merger with Three U.K. received conditional approval from the U.K.’s Competition and Markets Authority (CMA), forming the largest mobile operator in Britain.

- December 2024: Vodafone, in partnership with AST SpaceMobile, achieved a world-first: a direct-to-mobile satellite video call using a standard smartphone.

- May 2024: Vodafone sold its Spanish operations to Zegona Communications for €5B, as part of its strategy to simplify its portfolio and focus on core markets.

- March 2024: Swisscom agreed to acquire 100% of Vodafone Italia for €8B, aiming to merge it with its subsidiary Fastweb to create a leading converged operator in Italy.

- January 2024: The U.K. government raised national security concerns over the 14.6% stake in Vodafone Group acquired by Emirates telecom e& (formerly Etisalat).

Conclusion

This post has provided comparisons over a limited selection of metrics. Starting with CY 25Q1 results, we will publish more detailed comparisons and analyses in IDC’s European Enterprise Communications Services program, initially across the five operators presented here.