AI 产业化正从“模型竞赛”迈入“应用深水区”。2025 年,中国 AI 应用公有云服务市场规模突破 137 亿元人民币,已显著超过大模型训推公有云市场的 79.4 亿元。IDC 认为,这一结构性变化表明:企业客户正从“探索模型能力”转向“为业务价值付费”。未来 12–18 个月,能够将 AI 封装为行业应用、并支持智能体(Agent)工程化的云厂商,将成为新一轮增长的主导者。单纯提供模型 API 或通用算力的服务商,将面临被市场边缘化的风险。

从“模型竞赛”到“应用深水区”

AI 产业化正从“模型竞赛”步入“应用深水区”。谁能将 AI 能力真正嵌入业务流程、带动规模化落地,谁就将在未来的云服务竞争中赢得先机。那些能够将 AI 从“演示 Demo”转化为“业务系统”的厂商,正在加速拉开与跟随者之间的差距。IDC 追踪了公有云上 AI 应用市场,以及支持 AI 应用的大模型训推平台市场,可以看到公有云上 AI 市场格局正在发生巨变。

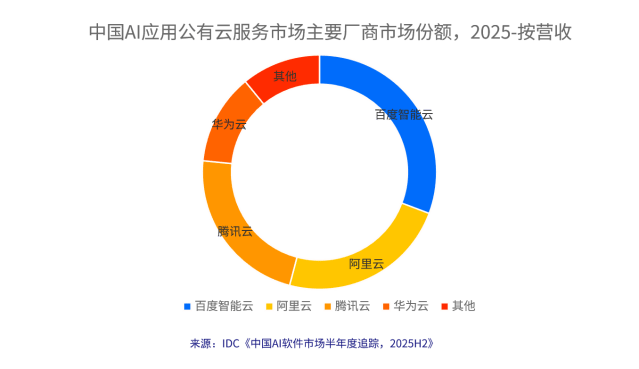

AI 应用公有云服务:137.3 亿元,应用落地成为核心战场

2025 年,中国 AI 应用公有云服务市场保持高速增长,市场规模突破 137 亿元人民币。在这一赛道上,头部云厂商凭借全栈 AI 能力和丰富应用场景占据领先地位。

百度智能云以 30.7% 的市场份额位居第一,依托包括智能客服、内容创作、知识管理等全面的企业级 AI 应用场景实现广泛落地。阿里云凭借智能语音、客服及视觉 AI 能力,在智能办公、营销创意等场景表现突出。腾讯云依托视觉 AI 能力、智能客服等在消费互联网、媒体、金融等场景持续发力。华为云则凭借盘古大模型在政务、金融、制造等行业的深度耕耘,稳居第四。

AI 应用市场的本质竞争,已从模型参数的“军备竞赛”转向场景价值的“落地之争”。 用户所需要的,并非孤立的模型 API 调用,而是一个能够真正解决业务问题、提升效率的完整应用。无论是智能客服、内容生成、数字人营销,还是企业知识库问答、代码辅助开发,云厂商需要将大模型能力封装为开箱即用的产品,方能打动最广泛的企业级客户。考虑到这一点,领先厂商均应将 AI 应用服务的投入重心,从底层模型能力向行业解决方案、数据接入、工作流编排等“最后一公里”能力快速倾斜。

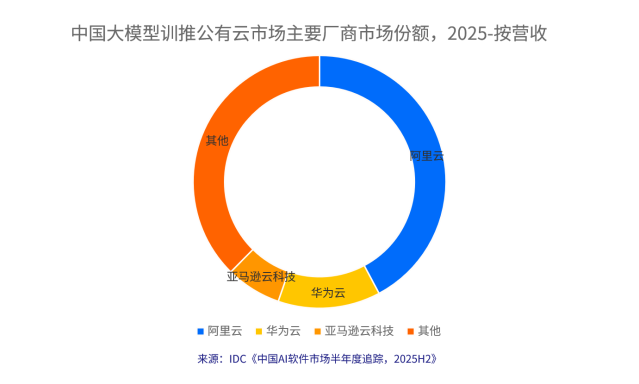

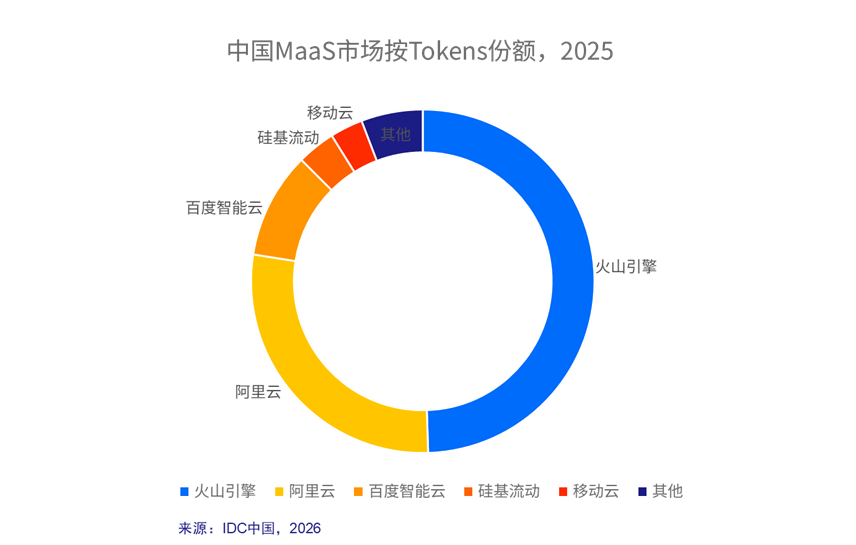

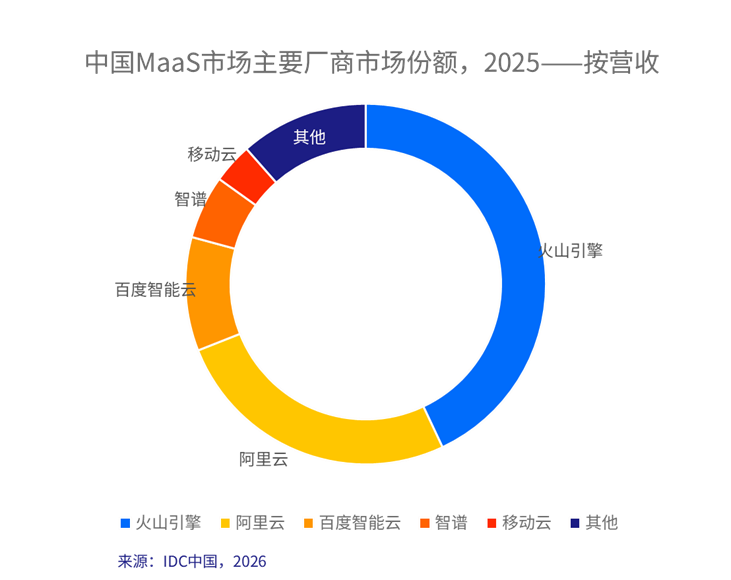

应用背后的“算力暗流”:大模型训推市场持续扩张

AI 应用市场的繁荣并非凭空而来。每一次智能客服的响应、每一次营销文案的生成,背后都是大模型推理能力的消耗;而企业为打造差异化应用所进行的模型微调与训练,则构成了另一层刚需——大模型训推公有云服务市场。该市场虽然规模小于应用层,但其增长稳定性与客户粘性更高。

2025 年,大模型训推公有云服务市场规模达到 79.4 亿元人民币,呈现出与前文 AI 应用市场不同的竞争格局。

阿里云以 42.2% 的市场份额遥遥领先,凭借在 AI 算力领域的长期积累和完善的 MLOps 工具链,成为大模型训练和推理的首选平台。华为云(13.1%)依托昇腾 AI 芯片和全栈自主可控能力,在政企市场获得广泛认可。亚马逊云科技(7.1%)则凭借全球化的 GPU 资源和先进的模型训练框架,在出海企业和外资企业中保持优势。

大模型训推市场的快速增长,背后有三大驱动力

第一,生成式 AI 应用爆发驱动训推需求激增。 从文本生成到图像创作,从代码辅助到多模态理解,生成式 AI 应用的繁荣带来了对模型训练和推理的海量需求。企业不仅需要调用预训练模型进行推理,更需要基于自有数据对模型进行微调,以打造差异化的 AI 能力。

Yanxia Lu is a research director, focusing on big data and artificial intelligence (AI). Her responsibilities include big data information management platform, and big data analytics and applications. She is also involved in research on AI technology and enterprise…

Quorra Liu is a Research Manager for the Client Systems Research team at IDC China. She is responsible for China's smart home device research. Her responsibilities include tracking the monthly and quarterly market development, conducting research in fully managed services market,…

Hangzhou has always defied expectations. Once celebrated for the serene beauty of West Lake, it reinvented itself as the birthplace of China’s digital economy through the rise of Alibaba. Now, it’s doing it again — emerging as one of China’s most serious players in artificial intelligence and embodied intelligence.

That’s why IDC Directions 2026 is coming to Hangzhou for the first time.

In 2025, the added value of Hangzhou’s core digital economy industries reached RMB 678 billion — accounting for 29.5% of the city’s GDP, with annual growth of 9.3%, according to the Hangzhou Municipal Bureau of Statistics. That momentum outpaces the broader national trend for digital sectors, underscoring the city’s leading position as a regional innovation hub. This isn’t a city on the rise. It’s a city already there.

Why Hangzhou, and Why Now

IDC Directions Beijing and Shenzhen have long been the go-to forum for China’s ICT community — drawing hundreds of industry participants, delivering senior analyst insights on AI, cloud, cybersecurity, and emerging technologies, and offering one-on-one sessions where ICT leaders dig into their real challenges and growth opportunities. The 2025 edition alone attracted nearly 300 industry leaders, digital experts, and investors when it launched in Shenzhen.

Now, that same calibre of conversation is coming to the Yangtze River Delta — and Hangzhou is the right city for it.

Three things set Hangzhou apart:

A proven innovation ecosystem. Hangzhou is home to a dense mix of startups, scaled enterprises, and specialized industry clusters. It’s not an emerging hub — it’s an active one, with real deal flow and real decision-makers already operating here.

Leadership in tomorrow’s technologies. Robotics, intelligent computing, and smart home industries are growing fast here, and Hangzhou’s engineering and R&D capabilities have already been showcased on a national stage at the CCTV Spring Festival Gala. This is a city that builds things.

Strong institutional backing. The Hangzhou municipal government’s Future Industry Cultivation Action Plan (2025–2026) is already in motion, and major national gatherings — including the China (Hangzhou) Embodied Intelligent Robot Industry Conference and the National Artificial Intelligence Industry Development Conference — have firmly established the city as a destination for serious tech collaboration.

What to Expect at IDC Directions 2026 Hangzhou

What we can already say: Curated event sessions will center squarely on Hangzhou’s flagship strength sectors—robotics, smart home ecosystems, and intelligent computing—while linking local innovation to the transformative trends reshaping China’s broader ICT industry agenda.

The event will feature keynote and breakout sessions delivered by IDC China’s most senior analyst team, with deep expertise spanning enterprise AI, emerging technology, digital economy, and industry transformation across core verticals.

Featured discussion themes will dive into tangible, high-impact topics: the rapid commercial adoption of AI Agents, full-stack cloud and computing platform evolution fueled by open-source models such as DeepSeek, and projected industrial AI investment in China set to hit RMB 900 billion by 2028.

Beyond insightful content, the event will gather a high-caliber audience pool including enterprise CxOs, top tech solution vendors, industry innovators, and institutional investors from Hangzhou and across the Yangtze River Delta—covering Shanghai, Nanjing, Suzhou and surrounding tier-one innovation cities. It offers a chance to network with regional decision-makers, benchmark industry best practices, and align long-term business strategies with local growth momentum as well as the strategic priorities outlined in China’s 15th Five-Year Plan.

Join Us in IDC Directions 2026 in Hangzhou

IDC Directions 2026 Hangzhou is where the region’s most important technology conversations will happen. Whether you’re sharpening your AI strategy, exploring opportunities in robotics and embodied intelligence, or building the partnerships that will define the next phase of your business — this is where you need to be. Register now!

Elly Hao is Senior Marketing Manager, Demand Generation, at IDC China, where she drives data-backed, integrated marketing initiatives that deliver qualified leads and support business growth. A seasoned cross-functional collaborator, she has overseen key programs including the annual FutureScape campaign. This year, Elly is leading the marketing efforts for IDC Directions Hangzhou, a key strategic growth initiative.

当前智能体在企业业务中的渗透率依然较低,仅有18%(IDC Syndicated Survey 2026: China AI Agents Market)。智能体没有在企业业务中真正规模化应用起来,核心在于缺少清晰的切入场景和可复用的落地路径。政策在这个角度提供了场景牵引,通过典型应用场景帮助智能体走向业务落地,并进一步形成规模化应用。

Zhenya Sun is a research manager for the IDC team focused on exploring the application of technology and industrial development of AI and AI agents. He is also responsible for providing clients with consulting services on technologies, products, and markets…

Joe Zhao is a senior research manager of Enterprise Research for IDC China. He focuses on research and analysis of the China security market. Joe has more than 12 years of domestic and international work experience in ICT. Prior to…

Yanxia Lu is a research director, focusing on big data and artificial intelligence (AI). Her responsibilities include big data information management platform, and big data analytics and applications. She is also involved in research on AI technology and enterprise…

Lizzie Li is Associate Research Director of IDC China's Enterprise System and Software Research that focuses on research and analysis of the China Datacenter, Cloud Computing, and IT infrastructure markets. She also provides intelligence and consulting services in customized projects for…

IDC Environmental Policy

International Data Group is committed to protecting the environment, the health and safety of our employees, and the community in which we conduct our business. It is our policy to seek continual improvement throughout our business operations to lessen our impact on the local and global environment. We are committed to environmental excellence, pollution prevention and to purchasing products that reduce the use of natural resources.

We fulfill this mission by a commitment to:

Encouraging all partners to share in our mission

Understanding environmental issues and sharing information with our partners

Recognizing that fiscal responsibility is essential to our environmental future

Instilling environmental responsibility as a corporate value

Developing innovative and flexible solutions to bring about change

Using our platforms and position in the IT industry to promote sustainability

Minimize air travel to help reduce our impact on the environment

Minimize use of materials and energy consumption in our offices

Create a working environment that efficiently uses our office space

Develop and maintain a hybrid working model that benefits both our employees and business partners

Encourage employees to measure, minimize and collaborate on reducing energy consumption at home and in the office

Engaging employees and promoting active participation in environmental and sustainability initiatives

Leaving?

You are about to leave this section. Do you wish to continue?