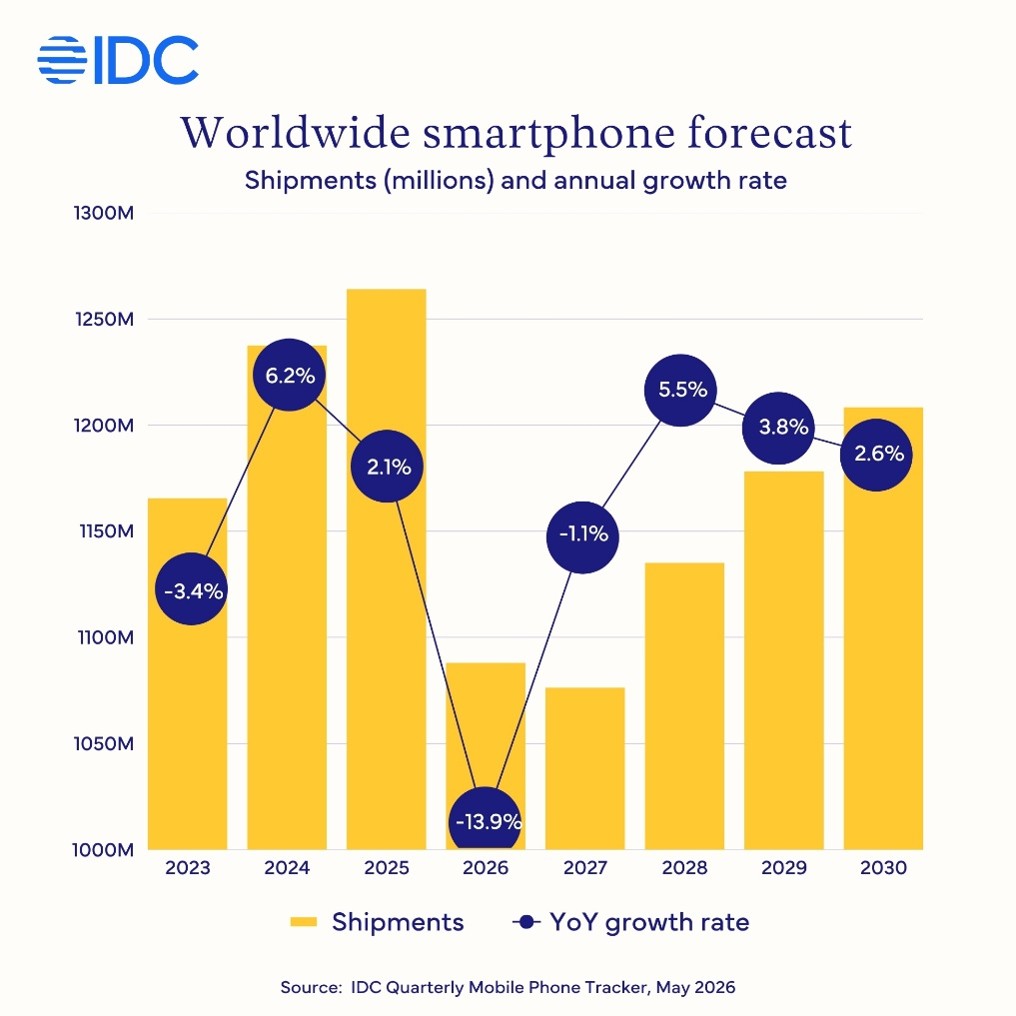

The smartphone market is headed into its worst year on record.

According to IDC’s Worldwide Quarterly Mobile Phone Tracker, worldwide smartphone shipments are forecast to decline 13.9% year-on-year in 2026 to 1.09 billion units. That is a further downward revision from IDC’s February forecast of a 12.9% decline, and it would mark the steepest annual contraction in smartphone history. A second consecutive decline of 1.1% is now expected in 2027, with a 5.5% rebound forecast in 2028 as memory supply normalises.

So what is behind the numbers, and what do they mean for vendors, regions, and operating systems trying to navigate this moment?

Why will the smartphone market see a record decline in 2026?

The memory shortage that began reshaping the market in 2025 is still the primary driver. But it is no longer working alone.

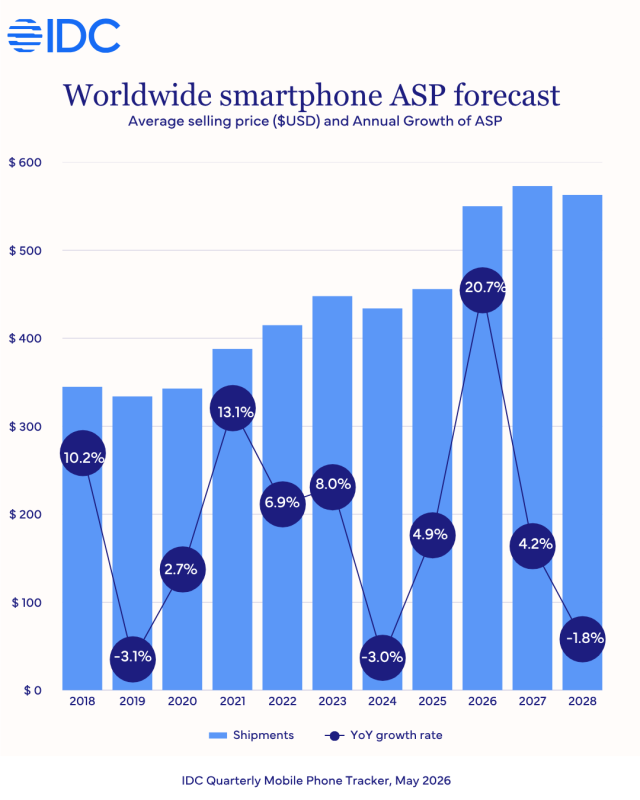

“The deepening memory shortage crisis remains the dominant force behind the record 14% drop this year, but it is no longer the only one,” said Nabila Popal, Senior Research Director with IDC’s Worldwide Quarterly Mobile Phone Tracker. “The US-Iran war has added a fresh layer of cost pressure for smartphone OEMs, driven by rising oil prices and transportation costs. Combined, these pressures are compelling vendors to reduce shipments, raise prices and concentrate on higher price tiers — elevating smartphone ASP to a record $550, up $100 from last year. 2026 will be a defining year for the industry as new reality of structurally higher costs take hold. For consumers, it means the era of ultra cheap smartphones is over. For vendors, it means only those that can adapt their strategies to this new cost environment and sustain demand at elevated price points will survive.”

How will different regions perform in 2026?

The decline is not distributed evenly. It is concentrated at the bottom of the market, and that means emerging markets will absorb the most pain.

The sub-$200 segment, where margins are already thin and consumers are most price-sensitive, will shrink the most. Regions with the highest concentration of sub-$200 devices are facing the sharpest declines: Middle East and Africa (MEA) is forecast to drop 23%, Central and Eastern Europe 19%, and Asia Pacific excluding Japan and China (APeJC) 14%.

North America holds up comparatively well, with only a 6.3% decline. The region is dominated by the premium segment, with 60% of shipments in 2026 Q1 above $800, and Apple and Samsung have proven resilient to the crisis at that tier. China is also forecast to decline double digits at 13%, as low-end Android players struggle to compete in the new cost environment.

How will performance differ across vendors and operating systems?

Android as a whole is forecast to see a 21% year-on-year drop, but that number masks two very different stories playing out within it.

Samsung is expected to grow market share in 2026, defying the broader Android decline by expanding in the premium segment and taking share in the mid-range. A combination of secured memory supply, a stronger Galaxy S26 line-up, and aggressive mid-range positioning is allowing Samsung to capture demand that smaller Android vendors simply cannot serve as memory costs squeeze their bill of materials.

iOS tells a different story. Apple’s forecast improved from an 8.1% decline to just 5.2% in 2026, a meaningful divergence at a time when the rest of the market is heading sharply downward. Apple secured the memory supply it needed early and is seeing exceptionally strong demand for the iPhone 17 series across developed markets and especially in China.

“2026 will be a defining year for Apple,” said Francisco Jeronimo, Vice President for Worldwide Client Devices at IDC. “In a year when the broader smartphone market will record its steepest decline in history, iOS will deliver its highest annual share ever, at 22%. Apple has done three things that few of its competitors have managed: it secured memory supply early, it built a portfolio strong enough to drive a remarkable turnaround in China, and it positioned the iPhone 17 to capture demand exactly when consumers in developed markets are extending replacement cycles and trading up. The shift in market share that follows from this crisis will benefit Apple more than any other vendor.”

HarmonyOS is the other bright spot. Huawei’s operating system is forecast to reach 62 million units in 2026, up sharply from the 42 million previously forecasted. Huawei has expanded HarmonyOS into the entry-level segment, sustained or reduced pricing on new models, and continued promotional support for older devices. The strategy has worked particularly well in China’s lower-tier cities, where the affordability gap created by rising Android ASPs has created space for a domestic alternative.

Will foldable smartphones grow in 2026?

Yes, and it is one of the few unambiguously good news stories in this forecast.

For the second consecutive year, foldables are defying the broader downturn. The category is forecast to grow 20% year-on-year in 2026, supported by new models from existing players and, more importantly, Apple’s long-anticipated entry into the segment in the second half of the year. Foldables remain a small share of total smartphone volumes, but they are now the only segment where vendors can credibly defend premium pricing and grow units at the same time.

What does this mean for vendors and the industry?

The forecast draws a clear dividing line. Vendors with scale, supply leverage, and pricing power, namely Apple, Samsung, and Huawei within China, will gain share. Smaller Android brands concentrated in entry-level price bands and emerging markets will face the sharpest contractions and, in some cases, exit the market.

ASPs are unlikely to return to 2025 levels within the forecast horizon. The sub-$100 segment, which accounted for over 170 million devices in 2025, becomes economically unviable as memory and NAND costs settle at a permanently higher level, even after the memory shortage stabilises in 2028.

The next 18 months will determine who emerges from this reset with a sustainable position and who does not.