For IT vendors, understanding vertical markets’ dynamics and the associated risks and opportunities relating to their clients’ industries is fundamental for success. But in an economy shaken by wars, volatile political landscapes, and inflation, it may be challenging to pin the pockets of growth.

This blog explores recent developments and ICT spending trends of three key European industries — automotive, software and information services, and banking — to help IT vendors identify key areas where their products and services are essential for customers to achieve their strategic goals.

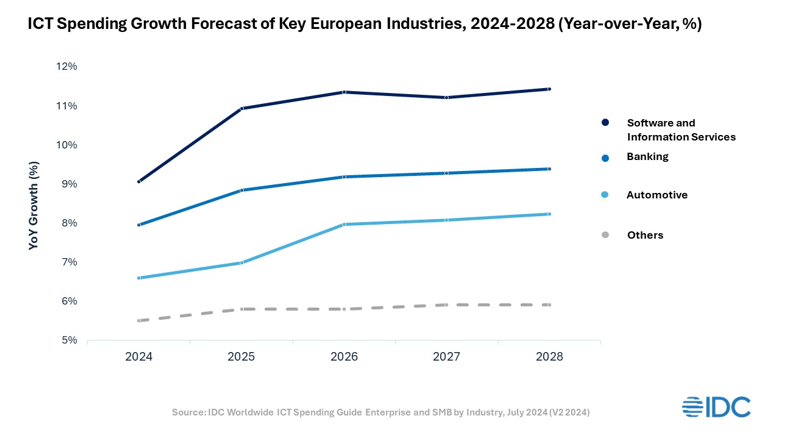

These three industries play a key role in shaping the European economy but are equally important in terms of their ICT spending. The automotive industry is the backbone of the European economy, representing over 7% of the European Union’s GDP. Software and information services, which includes cloud services providers, will continue to be a crucial industry in the years to come as it utilizes the most innovative and disruptive technologies. Banking, the industry with the largest ICT spending in Europe, continues to transform to meet the needs of an ever-changing and digital-savvy customer base.

ICT Spending Retains Robust Growth amid Ailing Economy

Europe’s economy has been weakened by the developments of the last couple of years, and while many indicators are improving, industrial activity is lagging, investments are being reevaluated, and exports have declined, reflecting asluggish foreign demand. On top of this, the conflicts in the Middle East and in Ukraine, the upcoming U.S. presidential election, and the fear of a global recession are fueling business uncertainty.

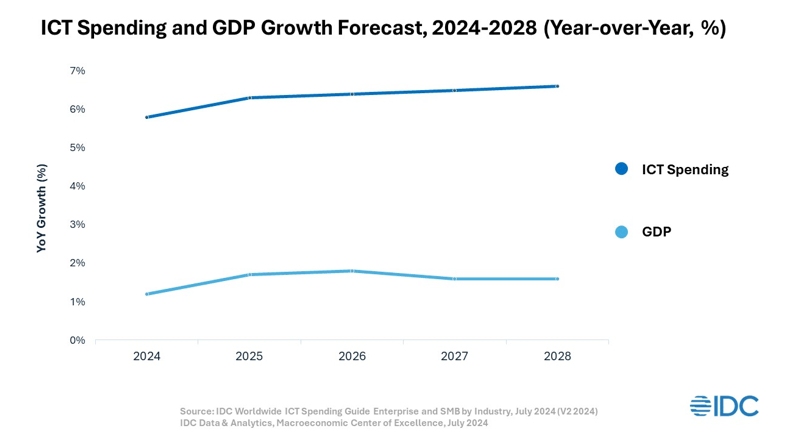

Yet, despite the ailing economy, the European ICT market is expected to reach $1.16 trillion this year, reflecting 5.8% growth compared with 2023, according to IDC’s Worldwide ICT Spending Guide: Enterprise and SMB by Industry. In contrast, the European GDP is expected to grow by 1.2% year on year in 2024.

ICT spending has historically been more resilient to disruptions than Europe’s overall economic performance. This is because organizational strategic priorities, such as efficiency, profitability, and sustainability, require companies to expand their digital capabilities, which cannot be done without investments in new technologies.

As a result, budgets allocated for some technologies, such as software, remain intact even during times of headwinds. Pharmaceutical companies focused on vaccine innovation have ramped up their investments in AI to accelerate drug development processes. Retailers are enhancing ecommerce platforms and in-store experiences as they respond to shoppers’ new behaviors. Central governments are stepping up physical and digital security, to avoid cyberattacks that could compromise the security of citizens’ data.

While IDC forecasts positive ICT spending growth for all European industries, the nature of the impacts and the level of resiliency will vary among them. In the following sections, we will dive into some of the technology spending trends of the key verticals in more detail.

Automotive: Legacy Carmakers Challenged by Lack of Software Capabilities

Automotive is among the European industries that were most impacted by recent headwinds. The Russia-Ukraine war and the Red Sea attacks have been causing supply chain disruptions, skyrocketing energy and material prices made production more expensive, and high inflation and the deterioration of consumer purchasing power slashed demand for both new and used cars. In addition, legacy automakers are dealing with slower-than-expected adoption of electric vehicles (EVs), fueling concerns about the return on their investments in EV development and production. At the same time, more advanced and cheaper products coming from Chinese manufacturers are challenging competitiveness of the European auto industry.

While the business conditions are far from favorable, automakers are still required to comply with the European Union’s sustainability and environmental regulations, which will result in large-scale investments along the entire value chain, leading to a profound transformation of the industry. Enterprise resource management (ERM), supply chain management (SCM), and engineering applications continue to be at the forefront of technology investments, as carmakers are working to reduce the cost, time, and complexity of production while developing safer, more intelligent, and more connected cars.

In parallel, organizations are seeking partners to reduce development costs and tackle the lack of expertise. Several recent announcements indicate that European legacy automakers are turning to technology companies or industry startups that have more experience with automotive software. For example, Volkswagen and Rivian intend to enter a joint venture to create next-generation software-defined vehicles (SDVs) with best-in-class software technology. BMW Group also announced collaboration with Tata Technologies, which will allow the Bavarian manufacturer to leverage its Indian partner’s talent pool and expertise in coding. BMW aims to strengthen its digital capabilities and improve its product portfolio with more advanced automotive software, including automated driving, infotainment, and digital services, which are gaining importance among customers.

Today’s vehicles are software-defined vehicles, often referred to as ‘computers on wheels’, and customers increasingly expect advanced driving assistance systems, in-car virtual assistants, broadband connectivity, over-the-air (OTA) software updates, and other digital functions. However, legacy automakers lack software development expertise and encounter software-related issues more frequently, resulting in postponed product launches. To avoid this, the industry needs to scale up its software capabilities, which will lead to growing investments and new partnerships.

Software and Information Services: Generative AI (GenAI) Remains in Focus to Deliver Increased Value to Clients

The software and information services industry, which includes software vendors, has a long history of bringing disruptive technologies to the market, as well as implementing innovative approaches within their internal processes. This will be the fastest-growing industry by 2028, posting a 10% five-year compound annual growth rate (CAGR). However, the recent crash of tech stocks not only indicates a growing concern about the future of the U.S. economy, but also a shaken confidence in AI projects, as their monetization is taking longer than expected. While some call this crash the long-awaited correction of the overpriced tech stocks, it is unlikely to stand in the way of the ongoing AI hype and technology investments aimed at innovation and bolstering the competitiveness of technology service providers.

GenAI remains the key driver of growth as technology giants aim to accelerate and simplify tasks while delivering extended customer experiences. Tech companies will continue to commit significant resources to refining GenAI deployment, and this will accelerate spending in AI solutions across all verticals. The list of GenAI use cases is extensive, but European businesses are largely using GenAI to generate sales and marketing content, optimize predictive asset operations, support planning and design, and streamline claim-handling processes.

Banking: Cloud Paves a Safe Way Forward

The IDC Worldwide ICT Spending Guide Enterprise and SMB by Industry forecasts that ICT spending in the banking sector will reach almost $120 billion in 2024, higher than in any other industry. In recent years, banks have rushed forward with their digitalizing efforts, prioritizing the optimization of existing systems to save costs and generate more value for clients. This paid off, with many European banks reporting strong H1 2024 and Q2 2024 results, while also catalyzing a surge in cloud spending and datacenter investments across Europe.

One of the most prominent recent examples of cloud investments is Denmark’s Danske Bank, which signed a multi-year agreement with AWS in March. By applying AWS’ technology in the cloud environment, the bank expects to optimize and modernize its applications. UniCredit Group, based in Milan, Italy, announced the acquisition of Vodeno and Aion Bank, with the aim of using cloud platforms to strengthen its competitive advantage in the banking as a service (BaaS) space. According to IDC’s Worldwide Software and Public Cloud Services Spending Guide, the industry’s public cloud spending will record a CAGR exceeding 23% by 2028.

Banking has been implementing AI solutions to support strategic goals, including increased productivity, improved customer experience, enhanced security, and optimized pricing. AI-enabled customer service and self-service is among the top five AI use cases in the banking industry. Banks are also implementing advanced virtual assistants to revolutionize customer engagement and self-service banking. For instance, Romania’s Alpha Bank is now using Druid AI’s conversational AI technology that allows customers to perform various banking operations autonomously.

Conclusion

Rapidly evolving vertical markets and the overall European economy present both opportunities and challenges. More than ever, IT vendors must now fine-tune their go-to-market strategy by aligning to the customers’ vertical-specific needs and priorities. This requires understanding the dynamics, risks, and opportunities of each sector.

Essential Guidance for IT Vendors:

- Adapt rapidly to new dynamics. In an economy dominated by market volatility, IT vendors must remain agile and responsive to market shifts. Understanding how geopolitical developments, economic uncertainty, and inflationary pressures affect industries will help vendors align their offering to their customers’ needs.

- Leverage the power of emerging technologies. IT vendors should continue to drive innovation, investing in solutions such as GenAI to disrupt the market. New tools will allow businesses to unlock new use cases and keep pace with evolving business needs.

- Align your vertical market strategy to customer needs. By focusing on vertical market dynamics and aligning product offerings to meet specific industry needs, IT vendors can position themselves as key partners, driving digital transformation and helping customers achieve their strategic goals even in challenging economic climates.

For a more detailed view of ICT and cloud spending forecasts by industry and company size segments, check out IDC’s Worldwide ICT Spending Guide: Enterprise and SMB by Industry, or Worldwide Software and Public Cloud Services Spending Guide.