ICT Spending Growth Driven by Accelerated AI Platform Investments in Banking, Software and Information Services, and Public Sector

SINGAPORE, 30 March 2026– According to the latest update of the International Data Corporation’s (IDC) Worldwide ICT Spending Guide Enterprise and SMB by Industry, ICT spending across Asia/Pacific excluding Japan and China (APEJC) is forecast to reach $647 billion in 2026 and is projected to surpass $758 billion by 2029. The APEJC market is set to grow by 5.4% in 2026, outstripping global growth rates as the region aggressively pivots from “experimentation” to “industrial-scale execution”. This surge represents a mandatory technological overhaul—enterprises are no longer spending for growth alone, but to avoid the obsolescence triggered by the “Agentic AI” era.

What Are the Main Technology Drivers for ICT Spending?**

Software continues to remain stable in 2026, capturing 24% of the regional spend. The priority has shifted from generic cloud migration to data sovereignty and security resilience. With the region becoming a primary theater for cyber-warfare, investments in the top two technology detail such as security software and robust enterprise resource management (ERM) applications are surging. These are no longer “back-office” costs, but the fundamental nervous system required to feed the data-hungry AI models for the next three years.

Services has emerged as a critical spending pillar, absorbing over 23% of the ICT budget as organizations face a brutal “execution gap”. The focus is shifting toward technology outsourcing within IT services and key horizontal BPOs within business services, as 60% of APEJC enterprises now require professional “health checks” to determine if their legacy infrastructure can support AI at scale. Furthermore, the expansion of Global Capability Centers (GCCs) in India and Southeast Asia is driving a massive uptick in managed services, as firms outsource complex engineering and AI orchestration to bridge the chronic local talent deficit.

Hardware remains the fastest-growing group at 3.6% YoY, fueled by the “China Plus One” manufacturing exodus. As production shifts to India, Vietnam, and Thailand, there is an urgent demand for non-x86 servers, edge computing nodes and specialized AI-centric infrastructure. This is an “infrastructure arms race” to build the smart factories and high-tech supply chains required to decouple from traditional manufacturing hubs.

Global ICT Market at a Glance

- Total APEJC ICT Spending (2026): $647 Billion (+5.4% YoY)

- Software: Fastest growth, +16.8% YoY (Focus on Data Maturity)

- Services: Critical driver, focused on AI Readiness & GCC Expansion

- Hardware: Largest tech group, >52% of spend (Driven by Regional Reshoring)

- Top Industries: Banking, Software and Information Services, Central Government (>$104B combined)

- 2026–2029 CAGR: Projected >7.4%

“The APEJC region is done with the ‘AI Entrant’ phase,” says Mario Allen Clement, research manager, IDC. “In 2026, the honeymoon is over. Boards are demanding a hard ROI on every dollar spent. We see a massive reallocation of capital away from ‘pilot projects’ and toward the unglamorous foundation—cleaning up toxic data, securing borders, and hiring the services talent that can actually make the machines work. If you haven’t fixed your data architecture by the end of 2026, you won’t survive the 2029 automation wave,” Mario added.

Key Global Dynamics

Geopolitical friction and supply chain re-alignment are the primary catalysts. India is the undisputed engine of the region, driven by its massive Digital Public Infrastructure (DPI) and a move toward “Sovereign AI.” ASEAN nations are prioritizing high-speed connectivity and data residency compliance to attract foreign tech giants fleeing regulatory volatility elsewhere. Meanwhile, Australia and New Zealand are focusing on high-value AI integration within healthcare and professional services to combat aging workforces and rising labor costs.

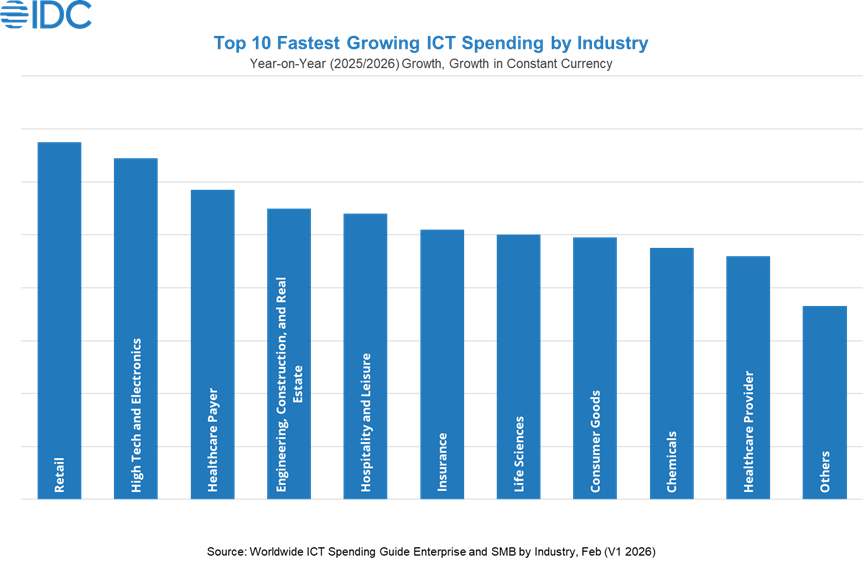

What Are the Key Industry Trends in ICT Spending?

Banking, software and information services, and federal/central government will represent the largest spending blocks in 2026. These industries are moving beyond basic automation into autonomous decisioning.

About IDC’s Worldwide ICT Spending Guide Enterprise and SMB by Industry

The Worldwide ICT Spending Guide: Enterprise and SMB by Industry examines the ICT market opportunity across SMBs and enterprise end users from a technology, industry, company size, and geography perspective. This comprehensive database delivered via IDC’s Customer Insights Query Tool allows the user to easily extract meaningful information by viewing and comparing data trends and relationships across ICT markets and segments.

Explore how escalating tensions in the Middle East are influencing IT spending across Asia Pacific.Register for our upcoming webinar for a scenario-based view of how demand and priorities are evolving.

Join IDC’s leading analysts at IDC Directions 2026 on May 21, 2026 at Conrad Singapore Marina Bay. Explore with them AI Value Creation, Physical AI, and AI Discovery and Commerce – and the opportunities they are creating in a new AI-era. Register for the event today!

*Asia/Pacific excluding Japan and China

**Excluding the telecom services spending

###

About IDC

International Data Corporation (IDC) is the premier global provider of trusted technology intelligence, advisory services, and events. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 100 countries. IDC’s analysis and insights help IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. To learn more about IDC, please visit www.idc.com/ap. Follow IDC on X and LinkedIn. Subscribe to the IDC Blog for industry news and insights. All product and company names may be trademarks or registered trademarks of their respective holders.