The Middle East War is no longer just a regional risk for technology leaders. It is becoming a global economic stress test — affecting energy prices, supply chains, inflation, business confidence, and IT budget decisions across Asia Pacific.

For CIOs, CFOs, and technology suppliers, the question is not simply whether IT spending will continue to grow in 2026. The sharper question is: which investments will still earn approval when volatility hits the budget?

That is the central signal from IDC’s latest webinar, Asia Pacific IT Spending Outlook 2026: Where to Win Amid Market Volatility. The market is not freezing. It is filtering.

This matters because the disruption is emerging against a market with strong underlying momentum. The opportunity is still there. The rules for winning it are changing.

The Middle East War is the shock

IDC’s earlier point of view on the Middle East War’s impact on IT spending outlined the broader global pressure points, from energy price volatility to supply chain disruption and cloud resiliency.

In Asia Pacific, those pressures are showing up in practical ways. Higher oil and electricity costs can raise operating expenses. Supply chain disruption can increase hardware costs and delay availability. Currency and pricing pressure can make approvals harder. As uncertainty rises, organizations move faster into contingency planning.

The first effect is not always a budget cut. More often, it is hesitation. Organizations start asking which projects are necessary, which can be phased, and which need to prove value faster.

As I noted during the webinar: “IT spending is likely to remain more resilient than in previous downturns because AI investment continues to support both the IT industry and broader economic growth.”

Resilience matters. It keeps the outlook from becoming a slowdown story. But resilience does not remove risk. The longer energy prices and supply chain disruption remain elevated, the more likely selective delays become targeted cuts.

Budget rotation is the signal

The most important shift is not how much organizations spend, but what they are willing to defend.

In a more volatile environment, buyers are becoming more risk-averse. ROI thresholds are rising. Procurement cycles involve more stakeholders. Vendors are seeing longer deal cycles, greater pricing pressure, and less predictable pipelines.

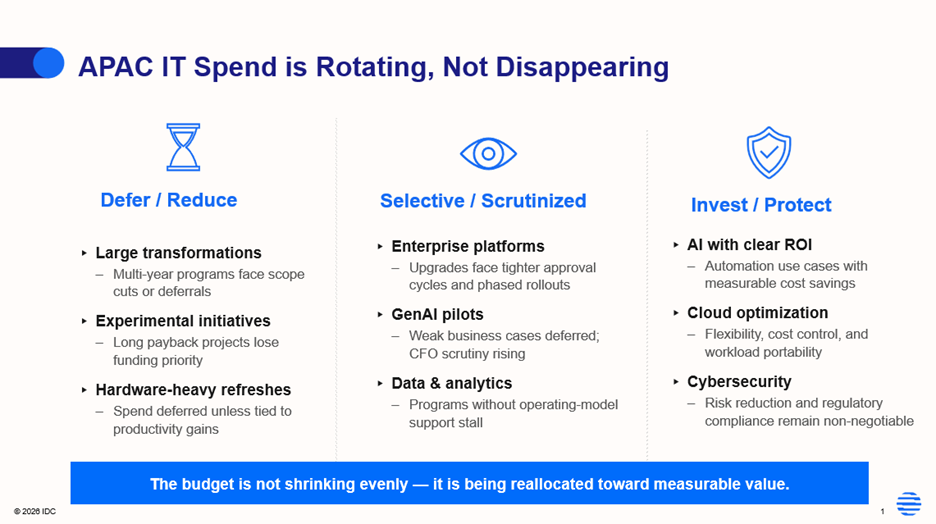

The visual above captures the core market signal: APAC IT spend is rotating, not disappearing.

Large transformations, experimental initiatives, and hardware-heavy refreshes are more likely to be deferred or reduced unless they are directly tied to productivity gains. Enterprise platform upgrades, GenAI pilots, and data and analytics programs are still in play, but they face tighter scrutiny and phased rollouts.

What remains protected? Investments tied to measurable outcomes. AI with clear ROI. Cloud optimization that supports flexibility and cost control. Cybersecurity that reduces risk and supports regulatory compliance. Infrastructure resiliency that helps organizations absorb disruption.

My colleague Vinayaka Venkatesh, summarized the shift directly: “The deals are not disappearing, but they are taking longer and require more effort to close.”

For technology suppliers, that line is the market cue. In 2026, vendors will not win by selling transformation in broad terms. They will win by helping buyers make the case for action now.

AI remains resilient, but proof matters more

AI remains central to the Asia Pacific technology agenda. IDC’s Asia/Pacific AI and GenAI spending outlook shows continued growth momentum as organizations invest in automation, productivity, and new business models.

But resilience does not mean every AI project gets a free pass.

One of the more important nuances from the webinar is the gap between AI infrastructure investment and enterprise AI execution. Hyperscalers and service providers continue to invest aggressively in AI infrastructure. At the same time, some enterprise AI initiatives are being de-scoped, delayed, or challenged on measurable outcomes.

This is where the “year of reckoning” for AI becomes real. AI use cases tied to cost savings, automation, customer experience, risk reduction, and operational efficiency will be easier to defend. Weak GenAI pilots, unclear operating models, or projects without a credible path to production will face more scrutiny from CFOs and cross-functional decision-makers.

AI for AI’s sake will not win the next budget cycle. AI with measurable business impact will.

What to remember for H2 2026 planning

As technology leaders plan for the second half of 2026, three takeaways matter most:

1. APAC IT spending is being disrupted, not derailed

The Middle East War is creating real pressure through energy costs, inflation, supply chain disruption, and weaker business visibility. But priority investments continue to support the market, especially AI infrastructure, cybersecurity, resiliency, and cloud optimization.

2. Budgets are rotating toward measurable value

Lower-priority initiatives, long-payback projects, and unclear business cases are facing delays. Investments that reduce risk, improve efficiency, support compliance, or deliver near-term ROI are better positioned for approval.

3. AI remains resilient, but the proof bar is rising

AI investment remains strong, but enterprise projects need clearer outcomes, stronger business cases, and a faster path from pilot to production.

The path forward is not about spending more for the sake of momentum. It is about knowing where to spend, what to protect, and what to pause.

Register for the on-demand webinar

The Middle East War is the shock. Budget rotation is the signal. Measurable value is the next move.

Register for the on-demand webinar, Asia Pacific IT Spending Outlook 2026 to see IDC’s latest scenario analysis, buyer data, and guidance on where IT spending is holding, where it is slowing, and what it means for H2 2026 planning.