In times of economic uncertainty, businesses tend to become more cautious and hesitant with buying decisions. This presents a unique opportunity, however, for technology vendors to demonstrate their value as catalysts of growth. By providing a credible economic impact model, tech vendors can offer a clear and data-driven analysis of their impact on the social, economic, and environmental aspects of their business, at a global, regional, or country level. This can help accelerate decision-making processes, and ultimately drive opportunity. Moreover, as consumers and businesses become increasingly aware of their impact on society and the environment, an economic and sustainability impact assessment can be a necessity for doing business in the future. By demonstrating how they positively contribute to the local economy and environment, tech vendors can differentiate themselves from their competitors and attract customers who prioritize sustainability and social responsibility.

When do you need an Economic and Sustainability Impact Study?

An economic and sustainability impact analysis is an important tool when a technology provider wants, or needs, to evaluate the impact of its business on the economy. It provides credible scenarios based on third-party data and research with a deep understanding of both technology and economic impacts, to demonstrate overall value. When technology vendors need to show that their investment in a region, or in a technology, creates spinoff economic and social impacts.

Key Reasons for Creating an Economic Impact Study

Marketing Executives:

- To build brand equity with governments

- To attract and increase media attention

- To create trusted content that demonstrates thought leadership

Partner Marketing Professionals:

- To demonstrate the opportunity their technology provides customers and partners to generate revenue

- To attract and retain partners to their ecosystem and deepen their share of wallet

Sustainability Executives:

- To show that their company is a catalyst for good

- To create awareness that their company is driving growth in a sustainable way, through measurable results

Why is an Economic Impact Study a differentiation tool?

Because the study is created by a third-party research firm, with a deep understanding of technology and industry verticals, they provide a credible, therefore trusted, thought leadership content tool, one that demonstrates a vendor’s overall impact as a catalyst for sustainable economic growth.

Leading subject matter experts author the study’s findings and can quantify exactly how your company will provide growth in three key areas:

- Economic impact

- Specifies increase to GDP

- Quantifies job growth

- Ecosystem impact

- Driving ecosystem opportunity

- Accelerating partner value

- Sustainability impact

- Measured reduction in greenhouse gas emissions

- Investment in social diversity

What is the process involved in building an Economic Impact Study?

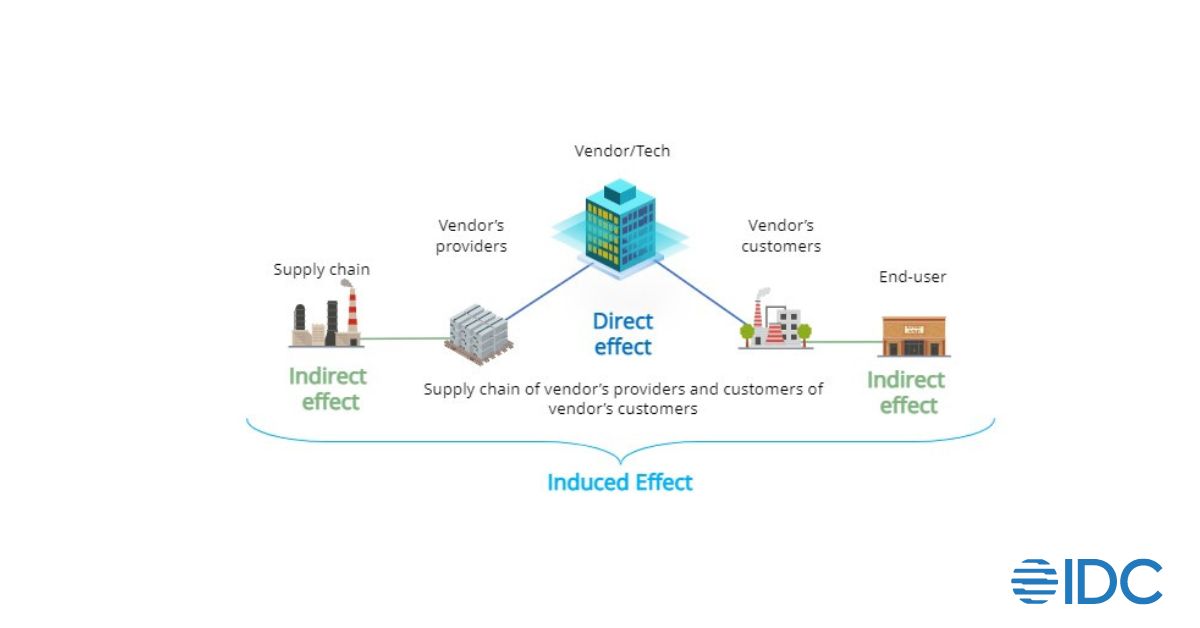

To estimate the overall economic of a technology provider, IDC utilizes a standard analytical framework, an Economic Impact Analysis, which leverages an input-output (I/O) framework.

Standard economic impact analysis evaluates three types of economic and social impact (GDP and job growth), as well as other impacts (such as, taxation):

- Direct: the effect on the direct supply chain for the solution

- Indirect: the effect on the supply chain and customers indirectly related to the solution

- Induced: secondary effects, not directly related to the solution. These can be effects generated in the economy from economic stimulus and the ripple effect on jobs and revenues, as an example.

How can you use an Economic Impact Study?

An economic impact study is a powerful tool that provides clear, quantified proof of your thought leadership. Used in marketing content strategies, it conveys your technology for good, for growth and for innovation.

- As a PR tool to generate increased media exposure and coverage

- In recruitment campaigns to attract and retain sustainability conscious talent

- Marketing and business outreach to show the business value, direct investment and infrastructure, contribution to GDP and employment, as well as tax revenues to support the global growth of the business in new geographies

IDC has been producing Economic Impact Models for more than 20 years. Our Macroeconomic Center of Excellence delivers credible, defensible assessments. Our technology research is fueled by more than 1300 of the world’s leading analysts who create non-bias, data-driven research. Learn More about IDC’s Economic Impact Model and thought leadership content solutions.