Key figures at a glance

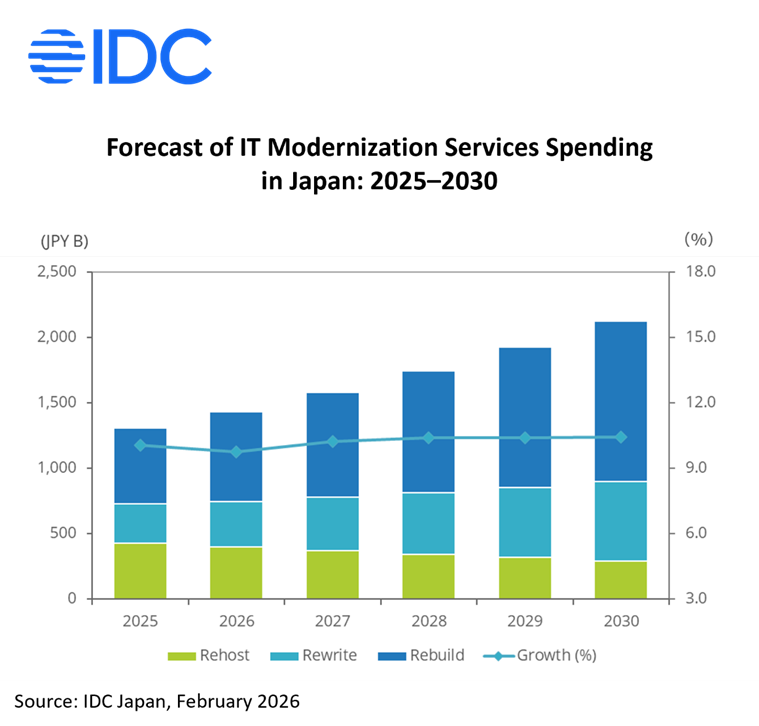

- ¥1,304B – IT modernization services market size, 2025

- 10.2% – Projected average annual growth rate, 2025–2030

- ¥2,123B – Forecast market size by 2030

- ~80% – Large and mid-sized enterprises still running legacy systems

Why Japan is outpacing the world

Japan’s IT services market is forecast to grow at a CAGR of 6.6% from 2024 to 2029, nearly double the global average of 3.6%. The answer is structural. Japan carries a uniquely heavy legacy burden, decades of investment in proprietary mainframe environments, complex bespoke systems, and a workforce that has long maintained them. Now, three forces are converging to make modernization unavoidable:

- Fujitsu Mainframe Sunset – In 2022, Fujitsu announced the end of sales and support for its mainframe and UNIX server products around 2030. This single announcement put more than 1,000 enterprises on an irreversible countdown, accelerating timelines across the entire Japanese market.

- AI Readiness Imperative – AI adoption presupposes tightly integrated data pipelines and modern business process architectures, exactly what legacy systems make impossible. Modernization is no longer optional for companies that want to remain AI-competitive.

- Demographic Pressure – The generation of engineers who built and maintained Japan’s legacy systems is retiring. Organizations face a narrowing window to migrate knowledge and infrastructure before institutional memory disappears entirely.

Three paths to modernization

IDC segments IT modernization services into three execution types, each with distinct implications for services firms:

- Rehost – Lift-and-shift to non-legacy platforms. Preserves existing application assets. The near-term entry point for enterprises constrained by budget or migration timelines.

- Rewrite – Convert legacy source code to modern languages without changing business logic. A middle path for controlled transformation.

- Rebuild – Redefine processes, data models, and architecture from the ground up. The highest-value, highest-complexity path.

Near-term, rehost is the second-largest segment after rebuild, driven by enterprises responding urgently to mainframe end-of-life deadlines — though it has already reached maturity and is forecast to decline. The mid-to-long-term growth opportunity lies in application modernization, rewriting, refactoring, and the adoption of microservices and cloud-native architectures.

What enterprises need from services firms

IDC surveyed large and mid-sized Japanese enterprises and found that organizations with significant legacy exposure do not simply want technical execution, they want transformation partners. Security remains a baseline expectation, but top-ranked needs now include business process redesign and cloud architecture strategy.

Demand signals also diverge meaningfully by sector:

- Financial Services – Prioritizes cloud-native application development capabilities, the ability to innovate rapidly on modern infrastructure.

- Manufacturing and Distribution – Prioritizes business process transformation, embedding efficiency and intelligence into operations, not just upgrading the underlying technology.

Across all sectors, IDC observes a consistent shift in enterprise expectations: business outcomes are becoming the primary purchase criterion. Technical competence is assumed; value creation is the differentiator.

How to build a winning position now

For services firms, the competitive imperative is clear. The service providers best positioned to win this market will do three things:

1. Codify your legacy modernization track record

Past engagements are an underutilized asset. Service providers should build structured libraries of business outcomes achieved, cost reductions, cycle time improvements, AI readiness unlocked and make these the core of their go-to-market narrative.

2. Develop industry-specific reference architectures for the AI era

Generic modernization pitches are losing traction. Enterprises want system architectures and implementation roadmaps calibrated to their sector, their regulatory environment, and their AI ambitions.

3. Invest in application modernization capabilities ahead of demand

The rehost wave is already approaching its peak. The high-margin opportunity – rewrite, refactor, rebuild – is building behind it. Service providers who develop deep cloud-native and microservices capabilities now will be the ones enterprises turn to in the second half of this decade.

About the IDC Report

IDC has published a comprehensive analysis of Japan’s IT modernization market: 2026 Japan IT Modernization Market Analysis. The report provides a medium-term market forecast for IT modernization of legacy systems — a primary growth driver in IDC’s Japan IT services market outlook. Legacy systems are characterized by aging and obsolescence, excessive complexity and scale, and a lack of transparency. It covers enterprises’ IT modernization trends and an analysis of the service vendors’ services trend. Market forecasts are segmented by service type, execution type (rehost, rewrite, rebuild), system type, and industry vertical. Together, these analyses offer a comprehensive view of shifting enterprise needs, emerging market opportunities, and the strategies and service offerings of leading vendors in Japan’s IT modernization landscape.

For more detailed insights and market trends, please contact our analysts by completing this form IDC | Identifying Market Opportunities – Contact Us.