What Happened in India’s Smartphone Market in Q1 2026?

India’s smartphone market shipments declined 4.1% year over year to 31.0 million units in Q1 2026, according to IDC’s Worldwide Quarterly Mobile Phone Tracker. Rising memory prices drove brands to front-load channel inventory ahead of anticipated cost escalations, pushing shipment volumes above initial expectations. However, underlying consumer demand remained subdued — weighed down by a typical post-festive slowdown, elevated device prices, and cautious spending sentiment. Despite falling volume, the market grew 5.8% in value terms, underscoring India’s ongoing shift from volume-led to value-driven growth.

Why It Matters

The Q1 2026 data signals a structural turning point for one of the world’s largest smartphone markets. Brands, retailers, and investors should take note:

- Device makers relying on entry-level volume face shrinking margins and reduced market viability as memory costs continue to rise.

- Consumers in sub-US$100 brackets are being pushed upmarket by necessity rather than aspiration — a trend that reshapes demand forecasting for 2026 and beyond.

- The gap between channel inventory and actual consumer demand points to a near-term correction risk, particularly in affordable segments.

Market Dynamics: What Drove the Outcome?

The market’s performance was shaped by three converging forces:

- Memory cost inflation → entry-level collapse: A global memory shortage drove up component prices across newly launched and existing models alike. Brands could no longer sustain profitability in the sub-US$100 tier, leading to reduced model availability and weaker channel participation. Shipments in this entry-level segment fell 59% YoY, with segment share collapsing from 18% to just 8%.

- Forced premiumization → mass-budget gains: Consumers who could no longer find affordable sub-US$100 options migrated upward. The mass-budget segment (US$100–200) grew 10% YoY, expanding its share from 39% to 45% — driven more by eroding entry-level value than deliberate upgrade intent.

- Promotional pullback → constrained demand recovery: Rising input costs limited brands’ ability to deploy the aggressive discounting and channel-led promotions that historically fuel mass-market growth. With fewer price interventions, underlying consumer demand stayed soft, particularly online, where shipments fell 14% YoY and share declined from 42% to 38%.

Price Band Performance

- Entry-level (sub-US$100): −59% YoY; share fell from 18% to 8%

- Mass-budget (US$100–200): +10% YoY; share rose from 39% to 45%

- Entry-premium (US$200–400): −3% YoY; share edged up from 26% to 27%

- Mid-premium (US$400–600): +29% YoY; share rose from 6% to 8%

- Premium (US$600–800): +32% YoY; share rose from 4% to 6%

- Super-premium (US$800+): −1% YoY; 7% share maintained

India Smartphone Market at a Glance – Q1 2026

- Total shipments: 31.0 million units (−4.1% YoY)

- Average selling price (ASP): US$302 (+10.4% YoY) — a record high

- Market value growth: +5.8% YoY despite volume decline

- Offline channel: 62% share (up from 58%); +3% YoY

- Online channel: 38% share (down from 42%); −14% YoY

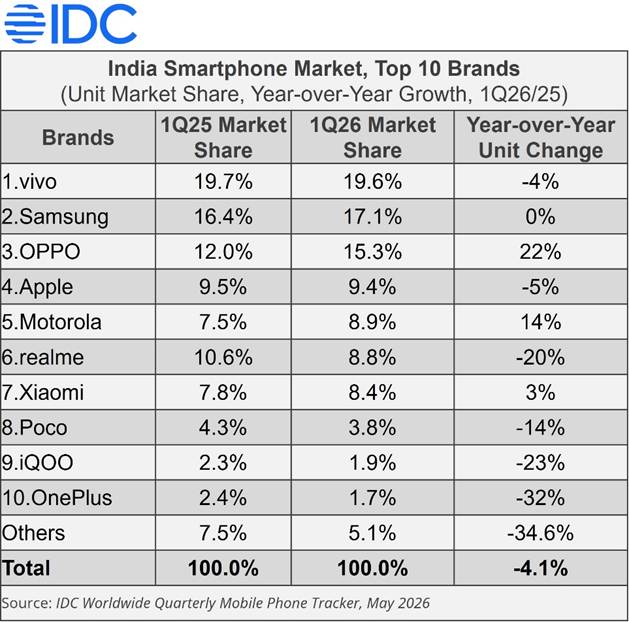

- Top five brands: vivo (#1), Samsung (#2), OPPO (#3), Apple (#4), Motorola (#5, new entrant)

Analyst Insight

“Average selling prices increased 10.4% YoY to a record US$302 in Q1 2026, driven by persistent memory cost inflation across both newly launched devices and existing models. Unlike previous quarters, aggressive discounting and channel-led promotional schemes remained limited, as rising input costs constrained brands’ ability to stimulate demand through pricing interventions. The current environment signals a broader structural shift in the market, where brands may increasingly need to rely on product differentiation, financing offers, and premiumization strategies rather than price-led promotions to drive demand through the remainder of 2026.” said Aditya Rampal, senior research analyst, Devices Research, IDC Asia Pacific.

Note: This chart/table shows data by IDC’s Brand field. Company ranking may differ where Companies own more than one Brand.

*Figures in tables/charts rounded to the first decimal point.

IDC Outlook: What’s Next?

The first half of 2026 is expected to remain relatively resilient as brands draw on existing component inventories to partially offset rising memory costs. However, brands are increasingly revising annual shipment targets downward, with channel inventory managed cautiously — especially in entry-level segments.

Recovery in the second half will depend on how effectively brands balance product innovation, pricing strategy, and cost management against sustained component inflation and uneven consumer demand.

- What could accelerate growth? Stabilization of memory prices, new financing models, and festive-season promotional activity.

- What could slow it down? A prolonged memory shortage, further rupee depreciation, and continued weakness in mass-market consumer confidence.

- What should readers watch next quarter? Whether brands can close the gap between channel inventory and end user sales, and how second-half pricing strategies unfold.

“In a value-conscious market like India, consumers have traditionally delayed purchases in anticipation of festive discounts and promotional offers. However, that pattern is unlikely to hold in the current cycle. With the global memory shortage expected to continue into 2027 and rupee depreciation adding further cost pressure, smartphone prices are set to rise further across segments. Consumers considering an upgrade may find better value in purchasing sooner, as pricing pressures are expected to intensify over the coming quarters,” said Upasana Joshi, senior research manager, Devices Research, IDC Asia/Pacific.

Frequently Asked Questions

Why did the market decline despite strong premium demand?

Growth in higher price bands could not offset the sharp collapse of the entry-level segment. While brands pushed inventory ahead of anticipated price hikes, weak consumer demand and limited promotional activity constrained actual market absorption, leaving supply-side momentum ahead of end-user demand.

Which brands benefited most in Q1 2026?

Motorola and OPPO were the only top-five brands to register YoY growth, with Motorola entering the top five for the first time. Apple held fourth place with a 9% shipment share while leading the market by value with a dominant 28% share. Notably, despite a 5% YoY decline in Apple shipments, the iPhone 17 alone contributed 4% of total smartphone volumes — underscoring Apple’s sustained premium strength amid broader demand softness.

What risks could impact the market in 2026?

A prolonged memory shortage, rupee depreciation, and weakening mass-market viability are the key near-term headwinds. Recovery will increasingly depend on brands’ ability to drive demand through financing and affordability-led models, rather than the aggressive price-led promotions that have historically fueled market growth.

-Ends-

About IDC

International Data Corporation (IDC) is the premier global provider of trusted technology intelligence, advisory services, and events. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 100 countries. IDC’s analysis and insights help IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. To learn more about IDC, please visit www.idc.com. Follow IDC on Twitter at @IDC and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

All product and company names may be trademarks or registered trademarks of their respective holders.