The foundational question for any vendor or service provider operating in Japan’s technology market today is no longer whether AI infrastructure will grow. That is settled. The question is how fast, in what form, and most importantly who will capture the value as Japan’s AI infrastructure market, consisting of servers and storage for AI, approaches and surpasses the ¥1 trillion threshold.

IDC’s latest data and forecasts provide a clear-eyed answer. What follows is the strategic view every vendor in this ecosystem needs to understand.

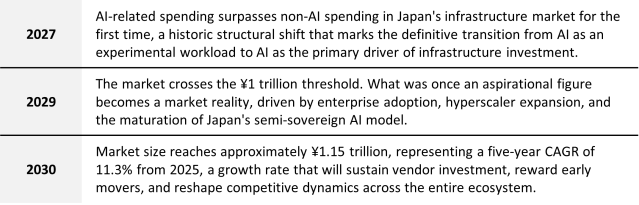

The road to ¥1 trillion: Three milestones that define the opportunity

IDC projects Japan’s AI infrastructure market will follow a clear and compelling trajectory over the next five years. Three milestones stand out:

These are not optimistic projections. They are grounded in structural forces – government policy, enterprise digitalization pressure, hyperscaler commitments, and the irreversible integration of AI into Japan’s economic fabric – that show no signs of reversing.

Where we are today: The foundation that makes this possible

To appreciate the scale of what lies ahead, it helps to understand how quickly Japan’s AI infrastructure market has already moved. In 2025, the domestic market reached ¥670 billion. For accelerator-equipped servers alone, the three-year CAGR from 2023 to 2025 approached 200%, significantly outpacing the global average.

This growth was not accidental. It was driven by a deliberate convergence of government economic security policy and domestic capital mobilization. Under cloud-related policy frameworks designed to advance Japan’s technological sovereignty, domestically capitalized service providers and telecommunications carriers launched large-scale AI infrastructure buildouts at a pace rarely seen in the Japanese market.

Physically, the transformation is equally striking. Rack-scale systems and multi-rack liquid-cooled configurations are becoming the new standard. What was once a 2U GPU server is evolving into an infrastructure architecture where entire data centers are purpose-designed around AI workloads. The ¥670 billion market of 2025 is built on this foundation, and the ¥1 trillion market of 2030 will be built on what comes next.

The structural dynamics vendors must understand

Japan’s AI infrastructure market in 2025 is heavily concentrated in service providers, who accounted for 90.6% of total market spend. With that figure, three dynamics will shape the competitive landscape through 2030:

- Hyperscalers will continue to expand. Their investment share surged from 39.8% in 2022 to 58.9% in 2025, a 19-point gain in three years. Alignment with hyperscaler platforms and roadmaps will remain a prerequisite for relevance in this market.

- Domestic service providers will remain strategically critical. Other service providers including policy-backed Japanese service providers and telcos held 31.6% share in 2025, essentially unchanged from 31.8% in 2022 despite the hyperscaler surge. This is a resilient customer segment that values local trust, regulatory compliance, and sustained partnership over pure price competition.

- Enterprise direct investment is the next growth frontier. At 9.4% of the market today, enterprise direct AI infrastructure investment has more than doubled in absolute terms since 2022, yet it remains nascent. Most large enterprises currently consume AI through generative AI services and SaaS platforms. As enterprises deepen their AI ambitions and move from consumption to ownership, direct infrastructure investment will accelerate. Vendors who build enterprise relationships now will be best positioned to capture this wave.

The semi-sovereign AI model: Japan’s defining strategic architecture

In April 2026, Microsoft announced plans to invest approximately ¥1.6 trillion in Japan between 2026 and 2029. Alongside this commitment came a plan to make AI infrastructure operated domestically by two partner companies available through Microsoft Azure, domestically built and owned infrastructure, connected to a global hyperscaler’s service layer.

This is what IDC describes as “Semi-Sovereign AI” and it is rapidly emerging as the defining model for AI infrastructure strategy in Japan. It represents a pragmatic and politically viable middle path: neither complete dependency on foreign hyperscalers, nor the prohibitive cost of fully independent domestic AI capability.

For vendors, this model is not a constraint. It is a structural opportunity. Semi-Sovereign AI creates a rich and expanding set of market roles in infrastructure design, systems integration, managed services, compliance, and the development of Japan-specific AI platforms. The vendors and integrators who understand this model deeply, and position themselves within it deliberately, will define the competitive landscape of Japan’s AI infrastructure market through 2030 and beyond.

What this means for vendors: Act now, not later

The policy-driven supply wave that built Japan’s AI infrastructure base is transitioning into a demand-driven growth phase. The central question is no longer whether the infrastructure exists, it does. The question is who helps enterprises put it to work, at scale, in ways that generate measurable business value. Three imperatives stand out for vendors competing in this market:

- Accelerate enterprise engagement. The 9.4% enterprise share of today is the growth story of tomorrow. Vendors who invest in enterprise relationships, Japan-specific use cases, and ROI demonstration frameworks now will be positioned to ride the most significant demand wave of the decade.

- Align with the Semi-Sovereign AI model. Understanding the interplay between domestic infrastructure owners, hyperscaler service layers, and government policy frameworks is not optional background knowledge. It is the strategic map for winning in this market.

- Build for depth, not just scale. Japan’s market rewards vendors who demonstrate sustained local commitment, deep technical expertise, and an understanding of Japanese enterprise culture. The ¥1 trillion opportunity will not be captured by volume alone.

Ongoing vendor share and demand analysis is available via the IDC Worldwide Quarterly AI Infrastructure Tracker. For more detailed insights and market trends, please contact our analysts by completing this form IDC | Identifying Market Opportunities – Contact Us.