Work in 2026 is being rewired around human-AI teams, where people who learn to collaborate with intelligent systems are gaining a clear edge in productivity, creativity, and career growth. IDC’s latest FutureScape and Future of Work insights show that this is no longer a distant trend but the operating reality for leading organisations worldwide.

The new shape of work

According our 2026 Futurescape for the AI-enabled Future of Work around 40% of roles in the G2000 will involve direct engagement with AI agents by 2026, fundamentally reshaping how entry, mid-level, and senior jobs are designed. In Europe specifically, we expect around 70% of new positions to be directly influenced by AI, blending technical fluency with human-centred capabilities like problem solving, empathy, and domain expertise.

AI is simultaneously and subtly absorbing much of the background work. Our analysis suggests AI tools can save workers over 40% of their typical workday, with IT workers gaining up to 45% of their time back as routine tasks are automated. Instead of spending hours on status reports, basic analysis, or rote documentation, employees can focus more on designing solutions, making decisions, and collaborating with customers and colleagues.

Agents as instruments, not co-workers

One of our most important messages though is that AI agents should be treated as instruments that extend human capability, not as synthetic co-workers to be managed like people. When AI is framed as a powerful tool in a human-led process, organisations are less likely to over-automate and more likely to invest in skills, governance, and thoughtful workflow redesign.

This mindset shift is already visible in how leaders talk about AI “co-pilots” across development, operations, and knowledge work. We predict that as agentic AI matures, organisations that focus on measuring and improving AI–human collaboration, rather than just raw productivity, will see margin gains of up to 15% by the end of the decade.

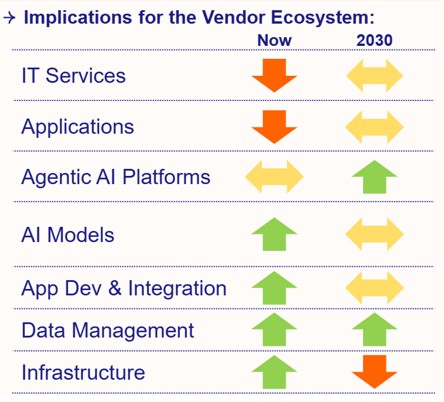

The skills crunch: $5.5 trillion on the line

The biggest drag on this transformation is no longer the technology but the skills to use it well. Our data shows that over 90% of global enterprises will face critical skills shortages by 2026, with AI-related gaps alone putting up to $5.5 trillion of economic value at risk through delays, missed revenue, and quality issues. Yet in our Global Future of Work Decision Maker only about a third of organisations say they are fully ready for AI-driven ways of working, and just a similar share of employees report receiving any AI training in the past year.

This imbalance is already reshaping labour markets. The 2025 IDC Employee Experience survey shows that that 66% of enterprises are reducing entry-level hiring as they deploy AI, and 91% report roles being changed or partially automated. Routine-heavy junior tasks are disappearing fastest, while demand grows for roles that can design, supervise, and continuously improve AI-infused workflows.

How to ride, not resist, the wave

For leaders and professionals, the 2026 question is not “Will AI take my job?” but “How quickly can my organisation and my skills adapt to human–AI collaboration?”. Our research into AI, automation, and Future of Work points to a few practical priorities that separate frontrunners from the rest.

- Build AI literacy for everyone, not just specialists: core skills now include prompt design, interpreting AI output, and knowing when to override or escalate decisions.

- Redesign roles around human strengths: shift job descriptions toward judgment, creativity, relationship-building, and cross-domain problem solving, with AI handling repeatable analysis and orchestration.

- Invest in trustworthy data and governance: companies that neglect high-quality, AI-ready data will see productivity fall behind as they struggle to scale agentic solutions.

- Measure collaboration, not just output: by 2029, organisations that track and optimise human–AI collaboration are projected to enjoy up to 15% higher margins than those that chase automation alone.

Work has been rewired, but the most valuable node in the system is still the human at the centre of an intelligent network of tools, agents, and collaborators. In 2026, the winners will be those who treat AI not as a threat or a crutch, but as a force multiplier for distinctly human ambition.

For more information see IDC FutureScape: Worldwide Future of Work 2026 Predictions

To watch our EMEA FutureScape predictions presentation, click here.

If you have any questions, please drop them in this form.