Asian banks are at a strategic crossroads. Business complexity is rising as new asset classes, digital channels and ecosystem partnerships expand. Meanwhile, banks face softening interest rates, credit pressures, and geopolitical uncertainty. In response, banks are increasing investment in technology, especially AI, to drive efficiency, resilience, and revenue growth. Recent IDC surveys show a clear rise in AI-related spending across the region.

The critical question is no longer whether banks are investing in AI, but how they can monetize that investment to generate measurable ROI and what role agentic AI plays in that equation.

Agentic AI offers banks a path from AI experimentation to measurable returns. By deploying autonomous AI agents across complex, multi-stage banking processes such as credit decisioning, risk management, and compliance, banks can accelerate decisions, improve consistency, and scale automation while maintaining governance. The greatest ROI comes from disciplined use case selection, AI-ready data and infrastructure, and strong trust and governance frameworks.

What Is Agentic AI in Banking?

Agentic AI in banking refers to AI systems composed of multiple autonomous agents that can independently analyze information, make decisions, and execute actions across workflows within defined guardrails and human oversight.

Unlike traditional AI models or copilots that provide recommendations, agentic AI systems can orchestrate end-to-end processes. This makes them well suited to banking operations, which involve multiple handoffs, probabilistic decision-making, regulatory constraints, and risk thresholds.

Why Banking Processes Are Strong Candidates for Agentic AI

Banking processes are often complex, involving multiple decision stages, approvals, and risk checks. Many already rely on probabilistic model-driven decision-making engines, making them well-suited for agentic architectures.

Example: Agentic AI in Credit Approval

Consider a credit approval process:

- One agent specializes in credit checks against defined risk acceptance criteria.

- Another agent estimates the maximum unsecured exposure the bank can underwrite.

- A higher-level supervisory agent evaluates outputs and acts as the approver.

Together, these agents can accelerate credit decisions, improve consistency, and maintain governance and control.

Key Challenges Banks Must Address to Generate ROI

While the opportunity is significant, deploying agentic AI at scale poses several challenges banks must address.

Is the Bank AI-Ready?

Banks must realistically assess their data architecture and infrastructure readiness. Data patching and manual corrections may work during proofs of concept, but are unlikely to succeed in production. Similarly, pilot deployments may run on spare capacity, while scaled agentic AI systems require dedicated, resilient, and secure infrastructure.

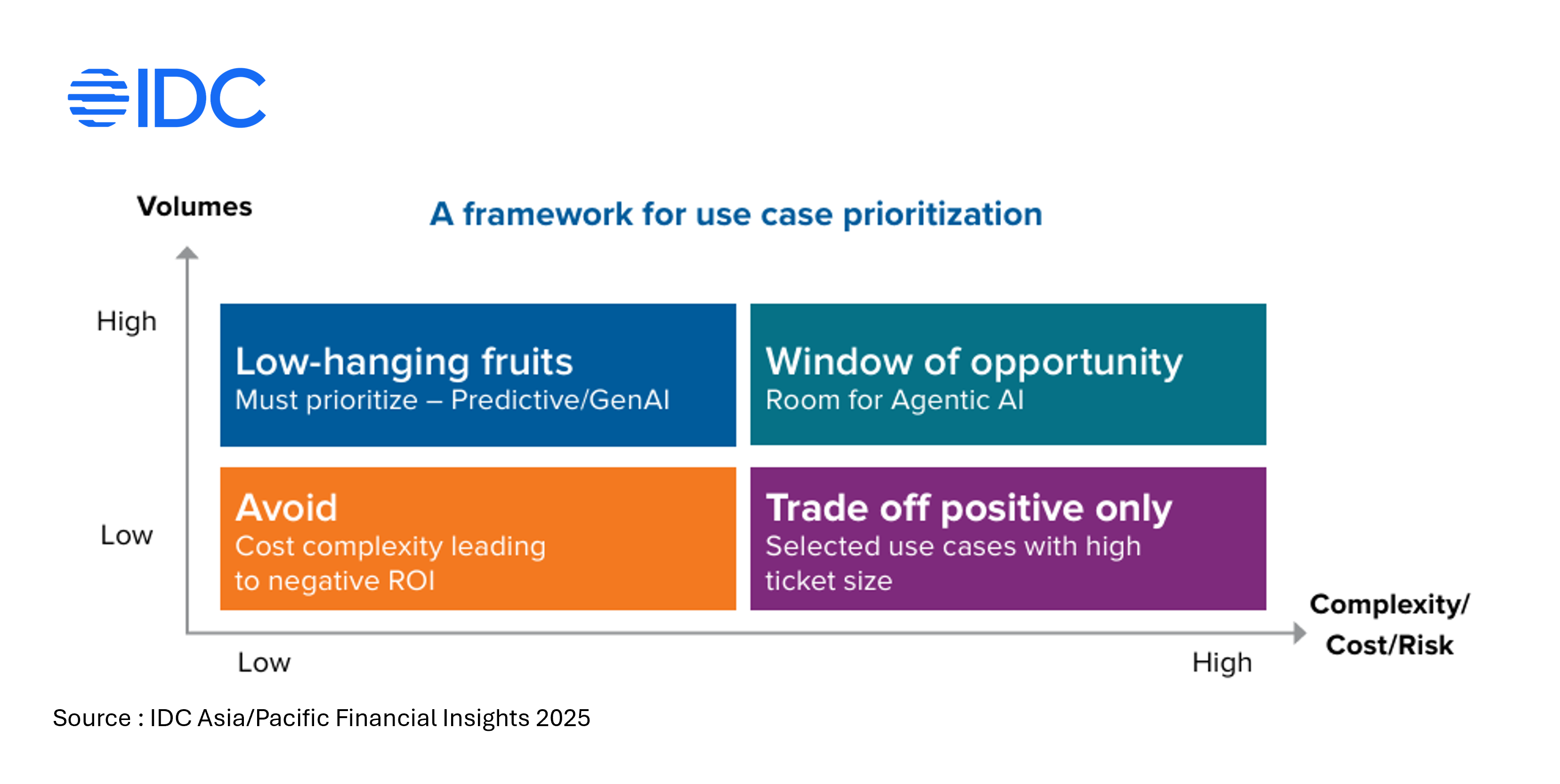

Selecting the Right Use Cases

Use case discipline is critical. Many banks run multiple exploratory or hobby AI projects driven by local enthusiasm rather than measurable business value. Even when proofs of concept show limited ROI, some initiatives still progress.

Prioritization must be anchored in clear business outcomes, such as:

- Revenue growth

- Operational efficiency

- Risk reduction and compliance effectiveness

Establishing Trust and Governance

The AI trust deficit remains a major barrier, especially given the persistence of hallucinations and model errors. Building trust requires governance frameworks, transparency, human-in-the-loop controls, and continuous monitoring.

Turning Agentic AI Investment into an AI Dividend

While these challenges are not insurmountable, overcoming them is essential to generating an AI dividend. IDC research and client engagements include multiple case studies that validate that agentic AI represents a significant opportunity for the banking sector.

According to the IDC FutureScape: Worldwide Banking and Payments 2026 Predictions — Asia/Pacific (Excluding Japan) Implications report, by 2027 in APeJ, the share of AI investments directed toward innovation will rise from 25% to 40%, with increased spending on new products and services.

Banks that act now—focusing on high-impact use cases, readiness, and governance—will be better positioned to translate the potential of agentic AI into measurable business outcomes.

What’s Next

IDC works with banks across Asia/Pacific to assess AI readiness, prioritize agentic AI use cases, and design governance models that support scalable ROI.

Register now for the live webinar on 24 February 2025 at 1:30 pm SGT to join IDC in charting the agentic future with confidence.