BOSTON and MUNICH, February 25, 2026 – Worldwide spending on edge computing reached $265 billion in 2025, expected to nearly double by 2029, reflecting a pivotal expansion fueled by rapid Edge AI advancements that accelerate enterprise transformation and open new opportunities for service providers, according to the IDC Worldwide Edge Spending Guide.

“The combination of maturing edge architectures and rapid AI development is fundamentally redefining how organizations process and act on data,” said Alexandra Rotaru, Data & Analytics Manager and WW Edge Spending Guide Product Lead at IDC. “We see enterprises and service providers shifting toward intelligent, distributed systems capable of real‑time decisioning and automation at scale. Edge AI is no longer experimental, its impact is already visible across industrial automation, smart retail, connected vehicles, and next‑generation healthcare.”

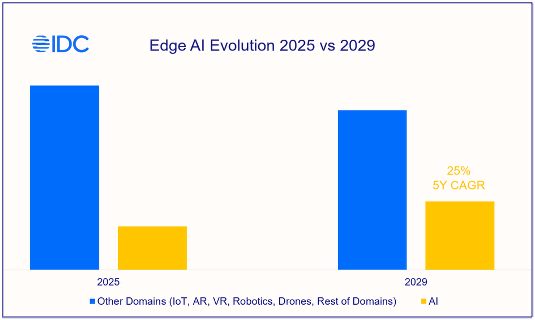

Edge as the foundational layer enabling multiple technology domains

IDC segments edge spending across more than 1,000 named enterprise use cases spanning six domains—AI, IoT, AR, VR, drones, and robotics—highlighting the expanding role of edge infrastructure in enabling advanced intelligent workloads. Artificial Intelligence is one of the fastest‑growing domains in the forecast, reflecting the increasing need to process data and run complex models directly at the edge. As organizations deploy more AI‑driven applications that require low‑latency inference, real‑time context, and resilient distributed architectures, edge computing becomes a critical enabler of innovation and value creation across industries.

Which edge-related technology dominates the market?

Hardware remains the dominant investment category early in the forecast period, propelled by the rapid adoption of AI‑accelerated infrastructure and increasingly sophisticated edge systems. This momentum reflects the growing need for real‑time computing at the point of data creation, as organizations deploy heavier edge architectures capable of supporting advanced AI workloads.

However, the aggregate Services segments (including Provisioned and Professional Services) are expected to surpass hardware’s share by 2029. Within Provisioned Services, Infrastructure as a Service (IaaS) remains the fastest‑growing category as organizations increasingly rely on scalable, flexible, and cost‑efficient consumption models to meet rising AI‑driven compute requirements at the edge. As more workloads shift toward distributed and AI‑enabled environments, as‑a‑service offerings provide a critical foundation for managing capacity, optimizing costs, and accelerating deployment across diverse industry use cases.

Impact across industries

The Retail & Services sector remains the largest contributor to global edge spending, driven by rapid adoption of AI and IoT-related use cases such as video analytics and real‑time operational optimization. Manufacturing & Resources follows, with AI‑enabled quality control, predictive maintenance, and autonomous material handling increasingly dependent on real‑time edge processing. Financial services is the fastest‑growing sector, supported by AI‑driven fraud analysis requiring low‑latency, distributed architectures.

Service Providers also continue to scale investments in AI‑ready edge platforms—including MEC, CDN and virtualized network functions—which are on track to represent nearly one‑third of the total market by 2029.

Regional development driven by the USA and Western Europe

North America will remain the top region for edge spending, driven by rapid adoption of Edge‑AI workloads and advanced infrastructure deployments. Western Europe and China follow, supported by strong industrial and public‑sector investment in AI‑enabled applications. The United States and Latin America are expected to record the fastest growth, as organizations across both regions scale low‑latency, AI‑driven use cases that benefit from distributed edge architectures.

Note: The IDC Worldwide Edge Spending Guide quantifies the edge computing market by forecasting enterprise and service provider spending across 22 technology markets, 7 technology domains, 27 enterprise industries, nine geographic regions, and, newly added, 24 countries. The list for the current release includes the following countries: ANZ (Australia and New Zealand), Argentina, Brazil, Canada, France, Germany, India, Indonesia, Italy, Japan, Korea, Malaysia, Mexico, Poland, PRC, Rest of APeJC, Rest of CEE, Rest of Middle East, Rest of Western Europe, Saudi Arabia, United Arab Emirates, United Kingdom and USA.

About IDC International Data Corporation (IDC) is the premier global provider of trusted technology intelligence, advisory services, and events. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 100 countries. IDC’s analysis and insights help IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. To learn more about IDC, please visit www.idc.com. Follow IDC on X at @IDC and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

All product and company names may be trademarks or registered trademarks of their respective holders.