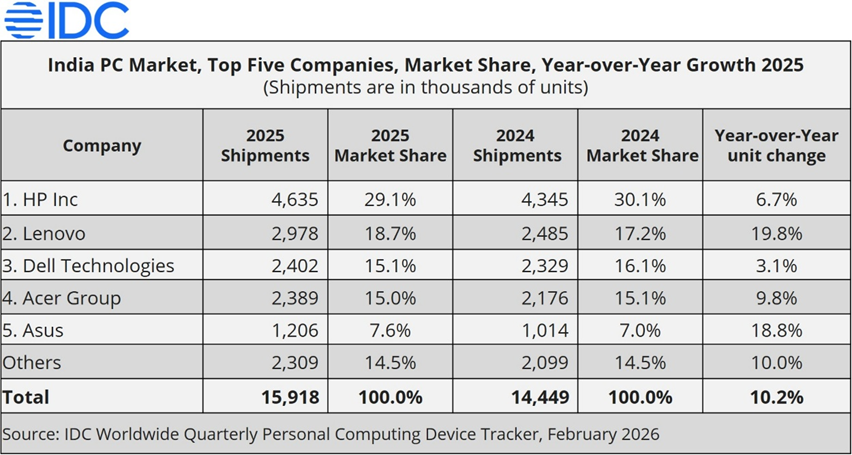

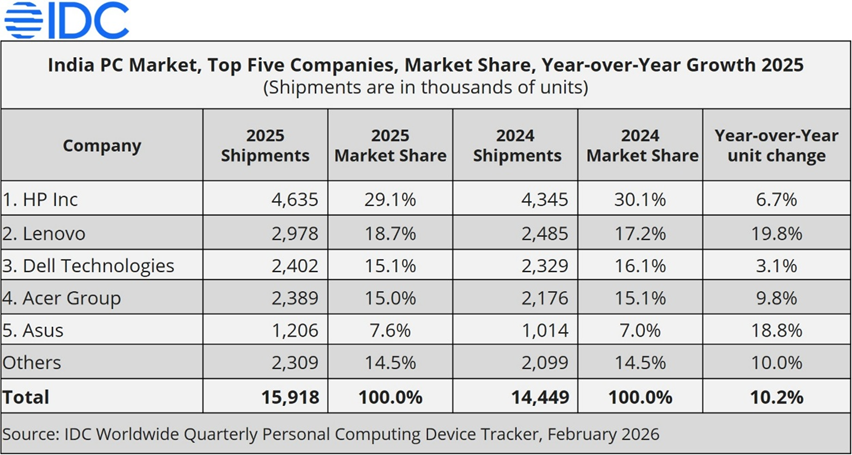

INDIA, March 5, 2026 – India’s traditional PC market—including desktops, notebooks, and workstations—recorded its strongest year ever in 2025, shipping 15.9 million units, growing 10.2% year over year (YoY), according to IDC’s Worldwide Quarterly Personal Computing Device Tracker.

This marks the first time annual shipments have crossed the 15-million-unit milestone, surpassing the pandemic-driven peaks seen in FY2021 and FY2022.

The market also delivered strong momentum in the final quarter, with shipments reaching 4.1 million units in 4Q25, reflecting a robust 18.5% YoY growth.

Category Performance Highlights

- Notebooks: The largest category continued to lead market expansion, growing 12.4% YoY in 2025 and registering a strong 23.9% YoY growth in 4Q25.

- Desktops: Posted moderate gains, increasing 3.6% YoY in 2025 and 6.2% YoY in 4Q25.

- Workstations: Emerged as the fastest-growing category, expanding 24.2% YoY in 2025 and 18.7% YoY in 4Q25, driven by demand from professional and high-performance computing use cases.

Premium notebooks (priced above US$1,000) grew 8.2% YoY, supported by rising demand for high-performance devices despite dollar appreciation and overall price increases.

AI-enabled notebooks stood out as a key growth driver, with shipments surging 129.3% YoY.

Basic AI notebooks accounted for 86.6% of total AI notebook shipments, driven primarily by enterprise adoption and consumer-led promotional incentives. Meanwhile, GenAI notebooks gained notable traction in the consumer segment, led by Apple’s MacBook portfolio, which captured a 70.9% share in this category.

Commercial and Consumer Market Performance

The commercial segment remained the primary growth driver for India’s PC market, shipping 8.6 million units in 2025.

- The enterprise segment expanded 20.9% YoY.

- Small and medium businesses (SMBs) grew 8.2% YoY.

Strong enterprise demand, along with partial fulfilment of the ELCOT manifesto deal, contributed to robust momentum in 4Q25, during which shipments reached 2.6 million units.

The consumer segment shipped 7.3 million units in 2025, growing 3.6% YoY. Strong online demand during festive sales and aggressive channel stocking supported annual performance. However, delayed supplies resulted in a slight 2.6% YoY decline in 4Q25.

The eTail channel continued its rapid expansion, growing 12% YoY in 2025 and 5.2% YoY in 4Q25, driven by wider geographic reach and competitive discounting strategies.

“PC shipments in the consumer segment grew YoY for the second consecutive year, driven by rising demand across use cases such as media consumption, content creation, and gaming,” said Bharath Shenoy, research manager, IDC India & South Asia. “PCs are evolving beyond traditional productivity tasks. Adoption for advanced content creation, high-end gaming, and virtual learning is revitalizing the category. AI PCs and growing vendor investments in AI capabilities are expected to further accelerate demand. However, processor shortages in late 2025 led to temporary supply constraints.”

Top 5 Company Highlights:

HP Inc. led India’s PC market in 2025 with a 29.1% share, maintaining leadership across both consumer and commercial segments. Strong enterprise demand and sustained channel momentum in the SMB segment drove 18.7% YoY growth in its commercial business. However, intensified competition across online and offline channels, along with softer-than-expected traction for its OmniBook series, led to a 9.4% YoY decline in the consumer segment. In 4Q25, HP held a 34.3% share in the commercial segment and 24.8% in the consumer segment.

Lenovo secured the second position in India’s PC market in 2025 with an 18.7% overall share. The company delivered balanced performance across segments, capturing 19.9% share in the commercial segment and 17.3% in the consumer segment. Commercial growth was driven by increased refresh demand, while the consumer business benefited from the growing popularity of Lenovo’s gaming notebooks, expanded retail presence, and competitive eTail pricing. In 4Q25, Lenovo ranked second in the consumer segment with a 20.2% share, while in the commercial segment, it held a 16.9% share.

Dell Technologies ranked third in India’s PC market in 2025 with a 15.1% share. The company recorded strong commercial growth of 18.3% YoY supported by an expanded AMD-powered portfolio and robust enterprise demand, particularly from global accounts. However, inventory clearance during 1H25 and supply constraints in 4Q25 contributed to a sharp 27.7% YoY decline in overall shipments. While the commercial segment remained resilient, consumer shipments were impacted in the latter half of the year. In 4Q25, Dell ranked second in the commercial segment with a 24.0% share, while holding a 9.2% share in the consumer segment.

Acer Group followed with a 15.0% share in India’s PC market in 2025, supported by positive enterprise orders and partial fulfillment of the ELCOT order. The company’s commercial segment grew 5.8% YoY while the consumer segment expanded 15.7% YoY, driven by strong demand for entry-level notebooks and an aggressive push through eTail channels. In 4Q25, Acer captured a 17.7% share in the commercial segment and a 10.2% share in the consumer segment.

ASUS rounded out the top five vendors in India’s PC market in 2025 with a 7.6% share. The company’s consumer segment grew 12.0% YoY, supported by offline expansion through large-format retail (LFR) channels. ASUS also made notable gains in the commercial segment, initially expanding through eTail channel and later strengthening its offline presence, resulting in a strong 98.3% YoY growth. In 4Q25, ASUS recorded healthy shipments across both segments, capturing a 12.1% share in the consumer segment and a 1.9% share in the commercial segment.

Market Outlook: Rising Component Costs to Challenge Growth

India’s PC market outlook for 2026 remains cautious. Rising prices key components, including DDR RAM, GPUs, and processors, are expected to impact device affordability.

“Despite strong performance in 2025, rising component costs are creating significant headwinds,” Navkendar Singh, associate vice president, Devices Research, IDC India, South Asia & ANZ. “PC prices have already increased by over 10% YoY and could rise another 15–20% in the coming quarters, and particularly impact price-sensitive segments such as SMBs and the government. Processor shortages may also limit entry-level PC availability, potentially shifting some demand toward alternative devices like tablets and smartphones.”

Notes:

- Shipments include shipments to distribution channels or end-users. OEM sales are counted under the company/brand under which they are sold.

- Enterprise segment refers to all companies with 500 and above employees, and SMBs refer to companies with fewer than 500 employees.

- Traditional PCs include Desktops, Notebooks, and Workstations and do not include Tablets or x86 Servers. Detachable Tablets and Slate Tablets are part of the Personal Computing Device Tracker but are not addressed in this press release.

-Ends-

For more information about this report, trends, or questions for analysts, please Michael De La Cruz at mdelacruz@idc.com or Miguel Carreon at mcarreon@idc.com. You can also follow IDC India’s Twitter and LinkedIn pages for regular updates on IDC’s research & events.

About IDC Trackers

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC’s Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly Excel deliverables and on-line query tools.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly owned subsidiary of International Data Group (IDG), the world’s leading tech media, data, and marketing services company. To learn more about IDC, please visit www.idc.com. Follow IDC on Twitter at @IDC and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

All product and company names may be trademarks or registered trademarks of their respective holders.