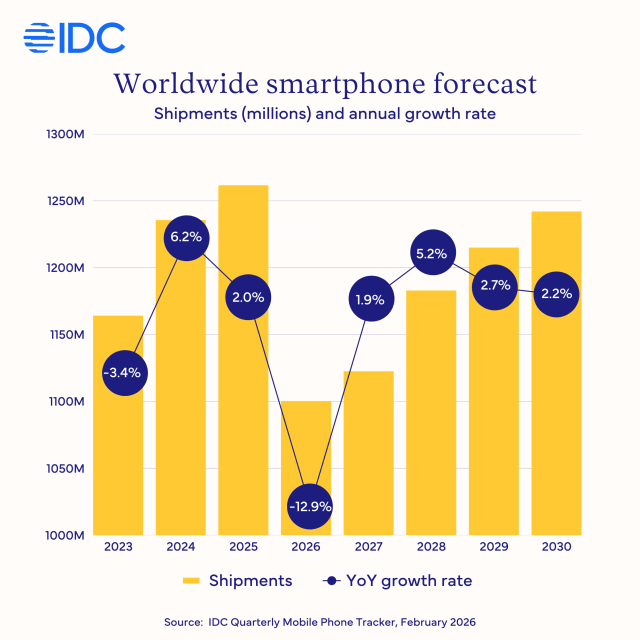

BOSTON, February 26, 2026 – Worldwide smartphone shipments are forecast to decline 12.9% year-on-year (YoY) in 2026 to 1.1 billion units, according to the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker. This decline will bring the smartphone market to its lowest annual shipment volume in more than a decade. The current forecast represents a sharp decline from our November forecast amid the intensifying memory shortage crisis.

“What we are witnessing is not a temporary squeeze, but a tsunami-like shock originating in the memory supply chain, with ripple effects spreading across the entire consumer electronics industry,” said Francisco Jeronimo, vice president for Worldwide Client Devices, IDC. “The global smartphone market, particularly Android manufacturers, faces a significant threat. Vendors whose business is mainly at the low end of the market are likely to suffer the most. Rising component costs will hit their margins, and they will have no choice but to pass the costs on to end users. By contrast, Apple and Samsung are better positioned to navigate this crisis. As smaller and low-end-positioned Android vendors struggle with rising costs, Apple and Samsung could not only weather the storm but potentially expand market share as the competitive landscape tightens.”

“The memory crisis will cause more than a temporary decline; it marks a structural reset of the entire market, fundamentally reshaping long‑term TAM (Total Addressable Market), the vendor landscape, and the product mix,” said Nabila Popal, senior research director with IDC’s Worldwide Quarterly Mobile Phone Tracker. “We expect consolidation as smaller players exit, and low-end vendors face sharp shipment declines amid supply constraints and lower demand at higher price points. Although shipments will witness a record drop, Smartphone ASP is projected to rise 14% to a record $523 this year. While memory prices are projected to stabilize by mid-2027, they are unlikely to return to previous level — making the sub-$100 segment (171 million devices) permanently uneconomical. In short, there is no return to business as usual for vendors and consumers.”

Regionally, markets with a high concentration of low-end smartphones are forecast to decline the most. Middle East & Africa will face the steepest drop at 20.6% YoY, while the world’s largest two markets, China and Asia Pacific (excluding Japan and China), are expected to decline 10.5% and 13.1%, respectively. As the crisis begins to stabilize by mid-2027, IDC forecasts a modest recovery of 2% that year, followed by a stronger rebound of 5.2% YoY in 2028.

About IDC Trackers

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC’s Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly Excel deliverables and on-line query tools.

For more information about IDC’s Worldwide Quarterly Mobile Phone Tracker, please contact Jackie Kliem at 508-988-7984 and jkliem@idc.com.

Click here to learn about IDC’s full suite of data products and how you can leverage them to grow your business.

About IDC

International Data Corporation (IDC) is the premier global provider of trusted technology intelligence, advisory services, and events. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 100 countries. IDC’s analysis and insights help IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. To learn more about IDC, please visit www.idc.com. Follow IDC on X at @IDC and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

All product and company names may be trademarks or registered trademarks of their respective holders.