Higher ASPs Signal Shift Toward Premium Devices Despite Volume Pressure

INDIA, March 2, 2026 – According to International Data Corporation’s (IDC) India Monthly Wearable Device Tracker, India’s wearable device market fell 4.0% year-over-year (YoY) in 2025, to 114.2 million units, marking its second consecutive annual decline. The downturn was driven primarily by a 17.6% YoY drop in smartwatch shipments. Despite softer volumes, average selling prices (ASPs) rose 1.8% to US$20.3 in 2025, reflecting gradual premiumization and easing price erosion.

Key Highlights of 2025:

- Smartwatch shipments declined for the second consecutive year, falling 17.6% YoY to 28.9 million units in 2025. Consequently, the category’s share of the overall wearables market contracted to 25.3%, down from 29.4% in 2024.

Despite lower volumes, the ASPs increased 11.7% YoY, rising from US$23.8 in 2024 to US$26.5 in 2025 as consumers pivoted toward higher-quality, feature-rich devices, partially offsetting shipment declines.

Advanced smartwatch shipments declined 8.7% YoY in 2025, yet the market share rose slightly from 2.9% in 2024 to 3.2% in 2025.

- Earwear category grew 1.4% YoY to 84.7 million units in 2025. Despite growth in select segments, earwear ASP dipped 1.1% YoY to US$17.5. This erosion reflects intense TWS mass-market competition and heavy online promotions.

The Truly Wireless Stereo (TWS) maintained dominance with a 70.2% share, though volumes stayed flat due to market maturity and longer replacement cycles.

Neckband shipments fell 10.2% YoY while Over-the-Ear emerged as the fastest-growing segment, surging 65.4% YoY (7.4M units) behind hybrid work trends and premium audio demand.

Vendor Performance

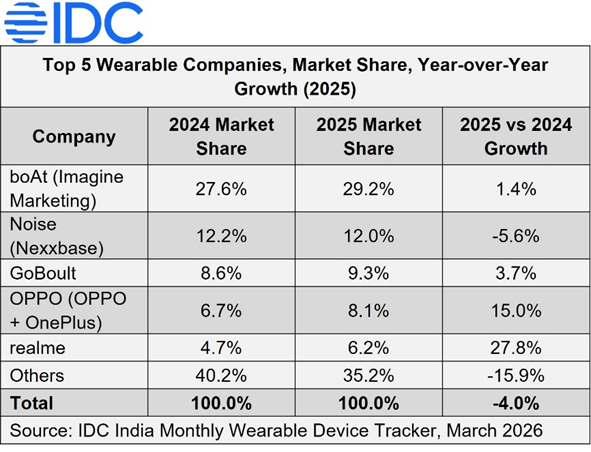

In the overall wearables market, boAt (Imagine Marketing) strengthened its leadership position in 2025, growing share from 27.6% to 29.2% in 2025. Dominating TWS, tethered, and over-the-ear categories with nearly one-third of total shipments, its success is driven by strong brand recall, a diverse portfolio, and effective omnichannel execution.

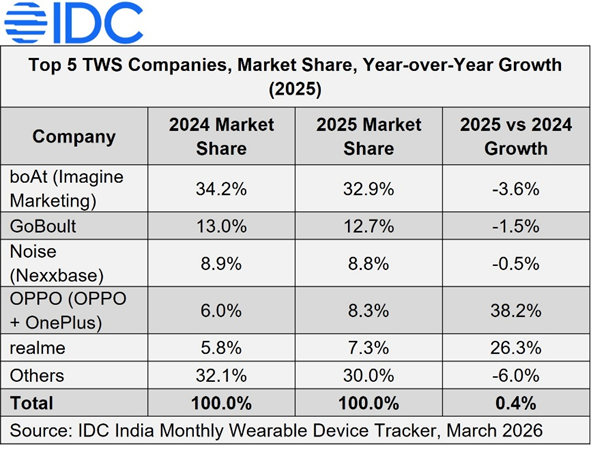

- In the TWS segment, smartphone-led brands gained further traction in 2025, among them Nothing (Including CMF) recorded highest 91.5% YoY growth, while OPPO (including OnePlus) grew 38.2% YoY, supported by stronger ecosystem integration and improved channel presence.

- The over-the-ear headphones segment witnessed strong momentum in 2025, led by boAt (Imagine Marketing), Samsung (JBL) and Zebronics. GoBoult & Noise (Nexxbase) posted an exceptional 698.3% & 276.5% YoY growth, reflecting rising demand for premium and lifestyle-oriented audio products.

- In the smartwatch category, Noise (Nexxbase) led with a 26.6% market share, supported by its strong presence in the mass-market segment. boAt (Imagine Marketing) ranked second with a 14.1% share, while Fire-Boltt shifted to third spot with 9.7% share. GoBoult remained consistent, ranking fifth with 29.8% YoY growth

Channel Performance

In 2025, the offline channel strengthened further, growing 3.1% YoY and expanding its share from 37.8% to 40.7%, while the online channel declined 8.4% YoY.

The online contraction was largely driven by a steep 22.7% YoY drop in smartwatch shipments, with earwear showing a relatively softer 3.2% decline. In contrast, offline earwear recorded 9.4% YoY growth, supported by stronger retail traction, although offline smartwatch shipments fell 10.5% YoY, highlighting a gradual shift toward offline retail channel penetration for stock push.

Emerging wearable categories are also gaining early traction, driven by innovation-led launches and new use cases, signalling gradual expansion beyond traditional form factors.

Smart glasses, the fastest-growing category of 2025, shipments surged 1,541.3% YoY. Lenskart (36.2%), Meta (28.4%), and Fire-Boltt (17.1%) led the segment, while ASP increased 152.4% to US$112.6, fueled by AI and Imaging upgrades.

Smart wristbands staged a 2025 revival, growing 67.0% YoY (0.3M units) behind health-focused launches. Samsung led the year with 59.0% share, while Pebble (SRK Powertech) secured the second spot (14.2%). WHOOP and Amazfit (Zepp) also fueled momentum with screenless design bands.

Smart ring shipments declined 30.6% YoY, though Ultrahuman led the category with 30.4% and Gabit in the second spot with 18.3%. ASP fell 8.7% to US$159.7 as boAt, Aabo, and Fittr joined the push for category adoption.

Smartwatch Market Outlook: 2026

Following a difficult 2025, the 2026 smartwatch market is resetting. Shipments are expected to dip in mid-single digits as the focus shifts from volume to high-value, health-centric platforms and ecosystem integration.

“Smartwatches are evolving beyond basic tracking. AI-led analytics, advanced sensors, and seamless connectivity are enabling predictive health insights, positioning them as proactive digital wellness partners,” said Anand Priya Singh, market analyst, Smart Wearable Devices, IDC India.

Earwear Market Outlook – 2026

In 2026, earwear growth will remain in the low single digits as the market matures. The focus is shifting from volume to high-value upgrades, with innovation centered on AI-led real-time audio and personalized spatial sound.

Commenting on the earwear category, Vikas Sharma, Senior Market Analyst, Smart Wearable Devices, IDC India says, “In a highly competitive pricing environment, brands are intensifying differentiation to support higher ASPs through ergonomic open-ear designs and partnerships with established audio specialists for premium sound. As the market stabilizes, strengthening offline reach and protecting brand credibility will be critical, especially amid increasingly sophisticated counterfeits in physical retail.”

Note:

- Wearable devices that are in the form of a band or watch and capable of processing the data digitally are considered in the wristwear category and it excludes the traditional analog and digital watches.

- The Smartwatch category includes Advanced Smartwatches (e.g., Apple Watch, Wear OS watches), and Basic Smartwatches (e.g., Noise watches, BoAt watches).

— Ends —

For more information about this report, trends, or questions for analysts, please Michael De La Cruz at mdelacruz@idc.com or Miguel Carreon at mcarreon@idc.com. You can also follow IDC India’s Twitter and LinkedIn pages for regular updates on IDC’s research & events.

About IDC Trackers

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC’s Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly Excel deliverables and on-line query tools.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly owned subsidiary of International Data Group (IDG), the world’s leading tech media, data, and marketing services company. To learn more about IDC, please visit www.idc.com. Follow IDC on Twitter at @IDC and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

All product and company names may be trademarks or registered trademarks of their respective holders.