Agentic AI and Platform Consolidation Shift Market from Experimentation to Scaled Deployment

SINGAPORE, April 13, 2026 – According to the IDC’s Worldwide AI and Generative AI Spending Guide, AI and generative AI (GenAI) spending in Asia/Pacific, including China and Japan, is projected to grow from $73 billion in 2024 to $370 billion by 2029, representing a fivefold increase at a compound annual growth rate (CAGR) of 38.4%. GenAI is the fastest-growing segment, expected to reach approximately $175 billion by 2029 at a 68.2% CAGR, making up nearly half (47.4%) of all AI spending in the region. This growth signals a shift from early adoption to enterprise-wide operationalization of AI.

What is happening in the Asia/Pacific AI and GenAI market through 2029?

AI and GenAI spending in Asia/Pacific is accelerating rapidly, with total investment expected to reach $370 billion by 2029. Growth is driven by enterprise demand for scalable infrastructure, operational efficiency, and AI-enabled applications, while challenges around governance, cost, and integration continue to shape adoption.

Key Market Metrics: Asia/Pacific AI and GenAI Market

- Total AI and GenAI spending: $370 billion by 2029 (from $73 billion in 2024)

- CAGR (2024–2029): 38.4%

- GenAI spending: $175 billion by 2029

- GenAI CAGR: 68.2%

- GenAI share of total AI spending: 47.4%

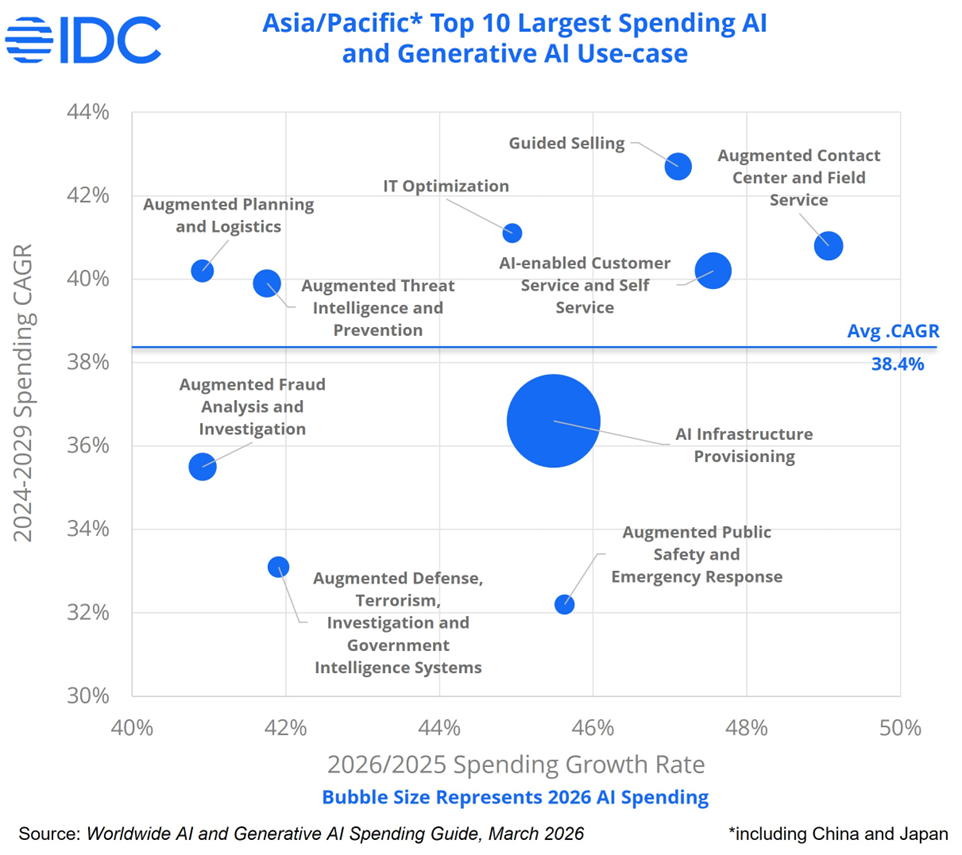

- Leading use case: AI infrastructure provisioning (approximately 39% of total spending)

“The Asia/Pacific AI market has shifted from an infrastructure-building phase to one defined by platform consolidation and operational depth,” says Vinayaka Venkatesh, senior market analyst, Data & Analytics, IDC Asia/Pacific. “Organizations are prioritizing AI platforms that unify generative, predictive, and prescriptive capabilities, with increasing focus on AI agents and orchestration to scale enterprise-wide adoption.”

Why did the market change?

Growth is being driven by a convergence of enterprise priorities. Organizations are investing in AI to support increasingly complex workloads, deliver hyper-personalized customer experiences, and improve operational efficiency. At the same time, rising demand for real-time analytics and security intelligence is reinforcing AI as a core capability rather than a discretionary investment.

Agentic AI is also reshaping the market. Enterprises are embedding autonomous capabilities into applications and platforms, enabling AI systems to move from assisted decision-making toward more autonomous execution across workflows.

IDC Outlook

IDC expects continued strong growth as organizations move from isolated AI use cases to integrated, enterprise-wide AI ecosystems. Investment will increasingly shift toward platforms that support orchestration, governance, and scalability. However, challenges related to cost control, regulatory compliance, and skills availability may moderate the pace of adoption in some markets.

Industry Adoption Trends

AI adoption across Asia/Pacific is expanding in both depth and scope. The software and information services sector remains the largest contributor, accounting for more than 47% of AI spending in 2026, driven by investments in development platforms, training infrastructure, and intelligent applications.

Financial services continues to scale AI usage beyond traditional risk and fraud applications into autonomous advisory, compliance automation, and real-time decisioning. Telecommunications and retail are embedding AI into core operations, including predictive network management, intelligent customer routing, demand forecasting, dynamic pricing, and personalized commerce.

Use Case and Public Sector Momentum

AI infrastructure provisioning remains the largest use case, reflecting sustained investment in accelerated computing, cloud-native services, and data center capacity. At the same time, conversational AI and virtual assistants are evolving toward context-aware, multi-turn interactions that support self-service at scale.

In the public sector, AI is gaining traction in national security and emergency response. Governments are deploying AI for surveillance, predictive threat detection, and real-time data fusion to improve situational awareness and crisis response outcomes.

FAQs

Why is AI infrastructure the largest investment area?

AI workloads require significant compute power, data processing capabilities, and scalable environments. As a result, organizations prioritize infrastructure readiness to enable downstream applications and ensure performance, reliability, and scalability.

Which industries are leading AI adoption in Asia/Pacific?

Software and information services lead in overall spending, followed by financial services, telecommunications, and retail. These industries are embedding AI into core operations to improve decision-making, customer experience, and efficiency.

What risks could impact AI market growth?

Key risks include rising infrastructure and operational costs, regulatory complexity across markets, and challenges in integrating AI into existing systems. Governance and trust in AI systems will also be critical as adoption scales.

Explore how escalating tensions in the Middle East are influencing IT spending across Asia Pacific.Register for our upcoming webinar for a scenario-based view of how demand and priorities are evolving.

Join IDC’s leading analysts at IDC Directions 2026 on May 21, 2026 at Conrad Singapore Marina Bay. Explore with them AI Value Creation, Physical AI, and AI Discovery and Commerce – and the opportunities they are creating in a new AI-era. Register for the event today!

The Worldwide AI and Generative AI Spending Guide sizes spending for technologies that analyze, organize, access, and provide advisory services based on a range of unstructured information. The Spending Guide quantifies the AI opportunity by providing data for 42 use cases across 27 industries in nine regions and 31 countries. Data is also available for the related hardware, software, and services categories.

**Taxonomy Note: The IDC Worldwide AI and Generative AI Spending Guide uses a very precise definition of what constitutes an AI Application in which the application must have an AI component that is crucial to the application – without this AI component the application will not function. This distinction enables the Spending Guide to focus on those software applications that are strongly AI Centric. In comparison, the IDC Worldwide Semiannual Artificial Intelligence Tracker uses a broad definition of AI Applications that includes applications where the AI component is non-centric, or not fundamental, to the application. This enables the inclusion of vendors that have incorporated AI capabilities into their software, but the applications are not exclusively used for AI functions only. In other words, the application will function without the inclusion of the AI component.

-Ends-

About IDC Spending Guides

IDC’s Spending Guides provide a granular view of key technology markets from a regional, vertical industry, use case, buyer, and technology perspective. The spending guides are delivered via pivot table format or custom query tool, allowing the user to easily extract meaningful information about each market by viewing data trends and relationships.

For more information about IDC’s Spending Guides, please contact Vinayaka Venkatesh at vvenkatesh@idc,com

Click here to learn about IDC’s full suite of data products and how you can leverage them to grow your business.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly owned subsidiary of International Data Group (IDG), the world’s leading tech media, data, and marketing services company. To learn more about IDC, please visit www.idc.com. Follow IDC on Twitter at @IDC and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

All product and company names may be trademarks or registered trademarks of their respective holders.