Smart Glasses Surge as XR Market Rewrites Its Own Rules

The global smart glasses category surged 167% year over year in Q1 2026, reaching approximately 2.25 million units shipped in a single quarter, according to new data from IDC’s Worldwide Quarterly Wearable Device Tracker and Worldwide Quarterly Augmented and Virtual Reality Headset Tracker. Eyewear with displays, tracked under IDC’s broader ARVR segment, grew 86% year over year over the same period.

Growth was driven by mainstream adoption of display-less smart glasses, led by Meta’s Ray-Ban partnership, alongside an expanding field of challengers building AI-first, always-on eyewear experiences.

Display-Less Glasses Lead the Shift

Display-less smart glasses shipped roughly the same volume in Q1 2026 alone as the entire category did across all of 2024. IDC forecasts full-year 2026 shipments of approximately 13.6 million units, growing to 27.3 million by 2030, a CAGR of 18.9%. Revenue is expected to reach $5.1 billion in 2026, while average selling prices, currently around $376, are forecast to compress to approximately $229 by 2030 as the category matures and volume expands.

Vendor Landscape: Meta Leads as Competition Broadens

Meta led the global smart glasses market in Q1 2026 with 69.2% share, supported by its EssilorLuxottica partnership and the continued strength of the Ray-Ban Meta lineup. RayNeo followed with 3.4% share, driven by lower-cost display glasses, while Xiaomi held 3.1% share on the strength of China shipments. Viture ranked fourth with 2.5% share following its US retail expansion, and XREAL rounded out the top five with 2.0% ahead of its push into the Android XR platform. The Others category, a long tail of global and Chinese vendors, accounted for 19.8% share.

Despite its lead, Meta faces mounting pressure from Google’s Android XR ecosystem, which enters with deep Gemini integration across email, photos, and search, and from Snap, whose Lens Studio developer base and five generations of Spectacles hardware give it a head start on the social and creative layer of smart glasses.

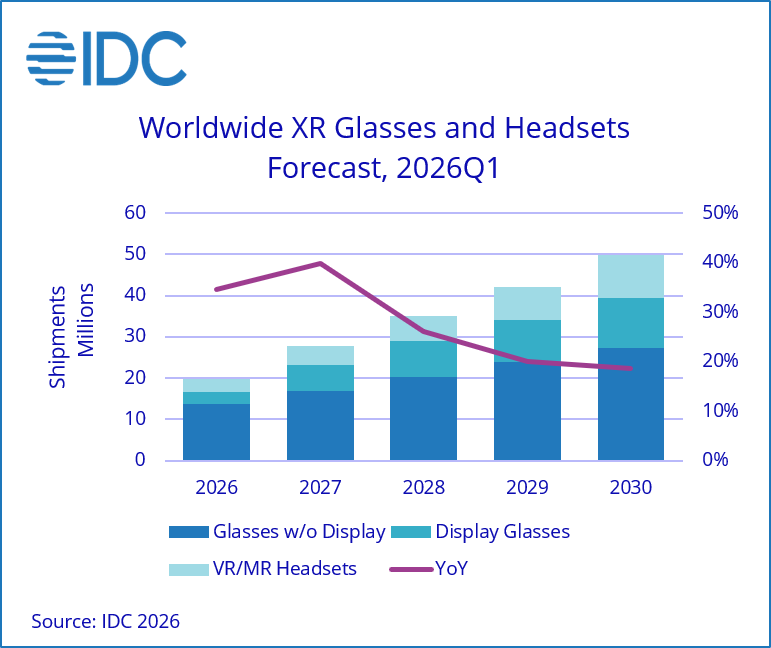

XR Market Outlook: Glasses Outpace Headsets

Mixed reality, anchored by devices like Meta’s Quest series, is forecast to grow from 3.2 million units in 2026 to 10.4 million by 2030, a 34.4% unit CAGR, with revenue reaching $7.1 billion by 2030. Optical see-through display glasses, from vendors including XREAL, Viture, and RayNeo, represent the fastest-growing segment, expanding from 3 million units in 2026 to 12.2 million by 2030, a 41.9% CAGR, as enterprise buyers gravitate toward premium spatial-computing hardware while consumers adopt mid-priced models.

IDC expects smart glasses to continue displacing traditional VR/MR headsets as the primary growth engine for XR through the forecast period, with platform, ecosystem, and AI differentiation determining the next phase of competition.