Worldwide Server Market grew by 30.7% in spending in the first quarter of 2026, driven by the continued mass deployment of GPU servers while keeping a 25.1% CAGR in a Five-Year Period, according to IDC.

The worldwide server market delivered 30.7% spending growth in the first quarter of 2026 while unit growth was modest at 3.3% year over year. The server market continues to be shaped by two distinct but interrelated dynamics: relentless AI infrastructure investment from hyperscalers and large cloud service providers, and an emerging supply-constrained environment in the non-accelerated segment where demand remains robust but component availability, particularly for memory (DRAM) and NAND flash, is limiting near-term shipment volumes. Leading vendors confirm order pipelines are strong and that supply, not demand, represents the primary ceiling for growth in the current environment.

IDC’s baseline assumes continuation of hyperscalers capex at announced levels, ongoing rack-scale GPU deployment with redistribution from ODM custom-rack to OEM rack-scale and standard-rack configurations, and a constrained memory/NAND supply environment with elevated pricing through at least the first half of 2027. Primary upside risks: enterprise AI adoption accelerating faster than measured, new application categories (physical AI, robotics, agent-based systems) creating incremental demand, or earlier resolution of supply constraints enabling unit-volume recovery. Thus, the market is expected to continue in a very positive trajectory of 25.1% compound average growth through 2030.

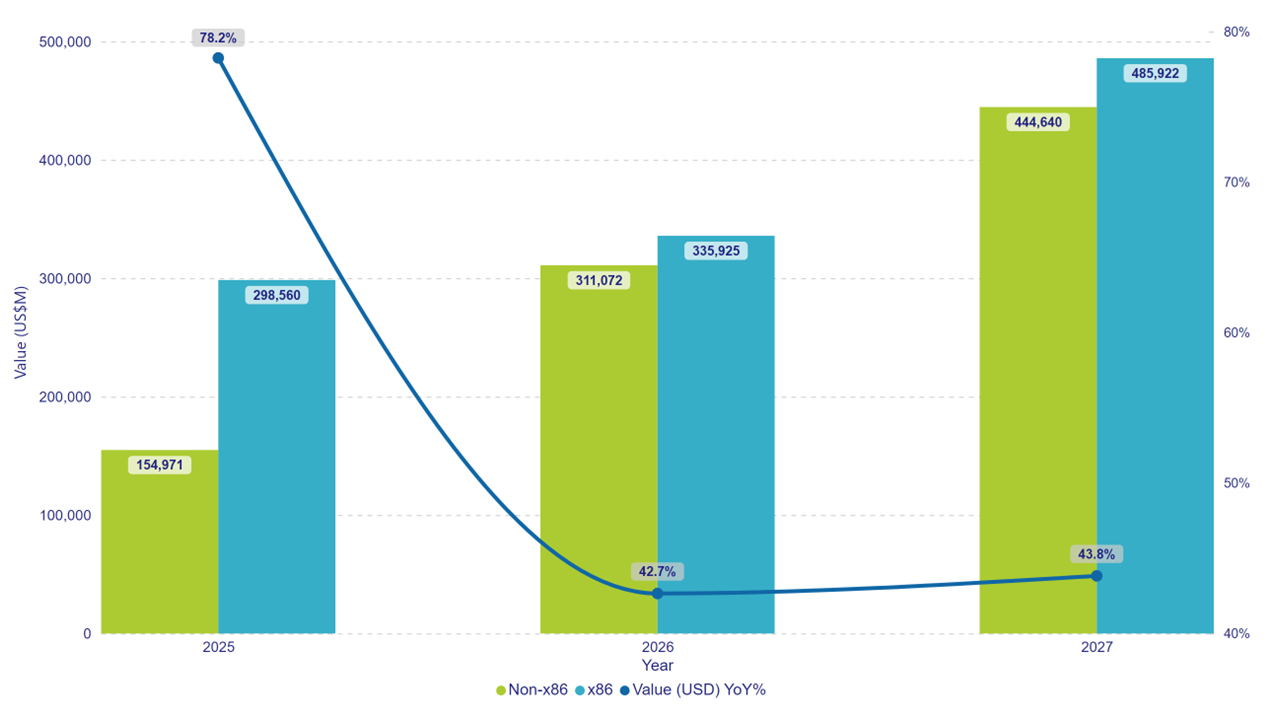

| Product Category | Non-x86 | x86 | Total | |||

| Date – Year | Value (US$M) | Annual Growth % | Value (US$M) | Annual Growth % | Value (US$M) | Annual Growth % |

| 2025 | $154,971 | 209.3% | $298,560 | 46.1% | $453,531 | 78.2% |

| 2026 | $311,072 | 100.7% | $335,925 | 12.5% | $646,998 | 42.7% |

| 2027 | $444,640 | 42.9% | $485,922 | 44.7% | $930,562 | 43.8% |