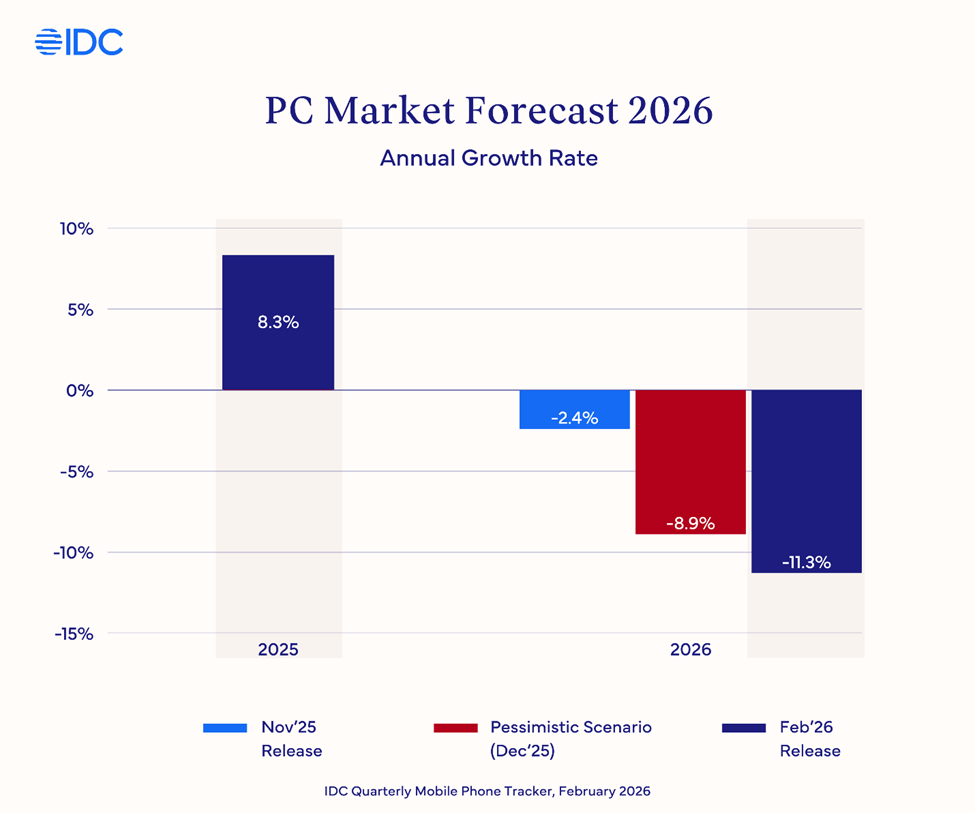

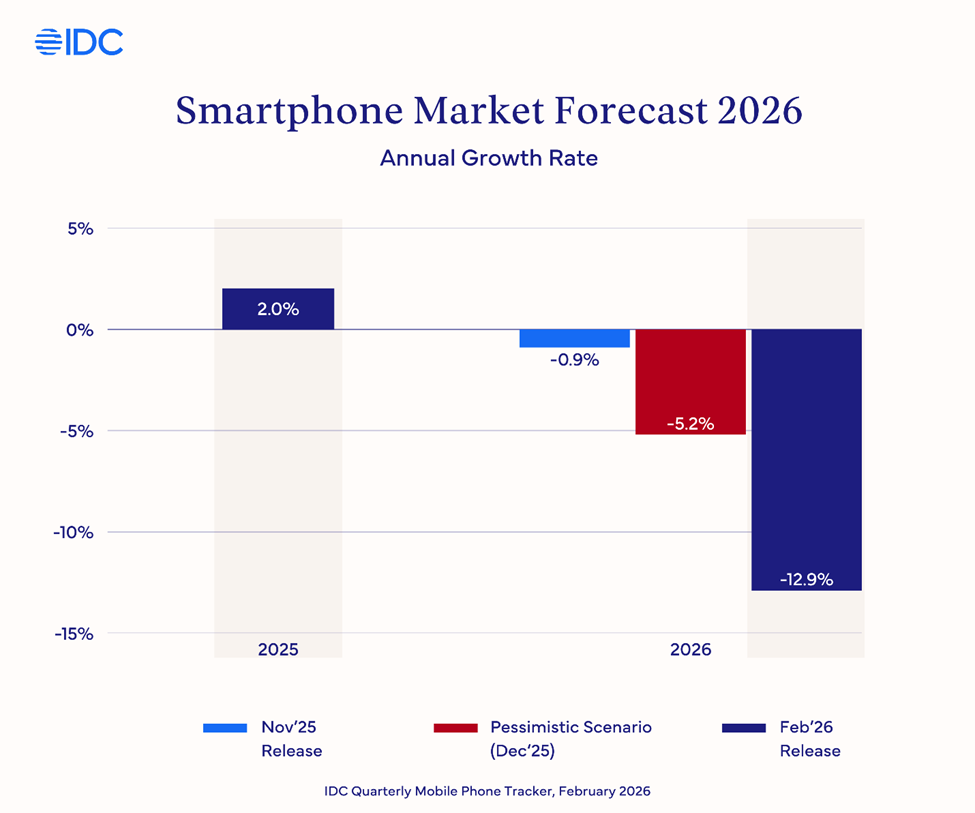

In December 2025, we published our analysis of the global memory shortage crisis and its potential impact on the PC and smartphone markets heading into 2026. At that time, we outlined two negative-impact scenarios, ranging from low single-digit to high single-digit market declines. This week, IDC released updated forecasts for both the worldwide PC and mobile phone markets, and the outlook has become significantly worse. The current situation is now more negative than even our most pessimistic scenarios suggested just a few months ago.

The market pull-forward

As concerns about DRAM and NAND pricing escalated in late 2025, vendors across both the PC and smartphone categories moved aggressively to get ahead of the problem. Shipments ramped significantly in the fourth quarter of 2025, as noted in our recent press releases on Q4 2025 PC historical shipment data and mobile phone historical shipment data. These elevated levels have continued into the first quarter of 2026 for the PC market, as OEMs rush to ship products before memory and storage price increases take full effect. The result is that we now expect Q1 2026, which ends in March, to come in significantly higher than our November forecasts for PCs. For smartphones, the situation is exasperated, with Q1 2026 forecast to decline 6.8%As memory prices climb and some vendors, particularly smaller ones, struggle to secure and/or pay for adequate supply, we expect unit volumes to fall off dramatically beginning in the second quarter. Average selling prices (ASPs) will rise, but volume demand will weaken in response. The net effect will be negative year-over-year unit growth for the full year, even as the revenue picture looks deceptively stable due to inflated ASPs.

For PCs, we are now forecasting the worldwide market to decline by 11.3% in 2026, while revenues grow 1.6% due to increased ASPs. Our current forecast shows the market flattening in 2027, with a rebound now pushed out to 2028. The smartphone market looks even more dire, as we’re currently forecasting the worldwide market to decline by 12.9% in 2026, with revenues declining slightly by 0.5%. We expect 2027 to see a modest 1.9% growth for smartphones, with a stronger 5.2% rebound in 2028.

IDC expects the memory supply challenges to persist throughout 2026 and likely well into 2027. While we do anticipate that the rate of memory price acceleration will slow in the second half of this year, prices will continue to rise and remain elevated. Based on current assumptions, our model does not point to a reversion to 2025 pricing levels within the forecast horizon. The structural dynamics driving the shortage, surging AI infrastructure demand competing with consumer device needs for the same DRAM and NAND capacity, remain firmly in place. There may be some relief as memory capacity buildouts increase and smaller memory suppliers in China come into play. However, we do not expect it to offset the shortage in a meaningful way and change the trajectory of the crisis.

The downstream consequences of the crisis are becoming clearer and will reshape competitive dynamics in the PC and smartphone markets described here, as well as in other device markets such as tablets, XR headsets, wearables, and gaming consoles.

Share shifts favoring larger vendors

Companies with greater purchasing power, stronger supplier relationships, and the ability to commit to large-volume contracts will be better positioned to secure memory allocations at high, but more manageable prices. Smaller and regional vendors, already operating on thinner margins, will find it increasingly difficult to compete for supply. We expect meaningful market share shifts in favor of the largest global OEMs over the course of 2026.

We also expect vendors to begin shipping some new devices with less memory than consumers have grown accustomed to. Rather than absorbing the full cost of higher-priced memory, some OEMs will opt to reduce average DRAM and NAND configurations in their products. A phone that might have shipped with 12GB of RAM and 256GB of storage a year ago may now debut with 8GB of RAM and 128GB of storage at the same price point, or worse. The same dynamic will play out in PCs, where base configurations could see meaningful reductions in RAM and SSD capacity.

The lower end of both markets will bear the brunt of the impact. Budget smartphones and entry-level PCs operate on razor-thin margins, leaving vendors with little room to absorb price increases. The math simply does not work for a $150 smartphone or a $400 laptop when memory costs surge by double and even triple digit percentages quarter over quarter. Many vendors will either exit price points entirely or deliver products with specifications that are noticeably degraded, at likely higher prices. For consumers and small businesses already sensitive to pricing, this will push many to delay planned device purchases, extending replacement cycles and further depressing unit volumes.

For the smartphone market, the implications are especially severe. Last year, more than 360 million smartphones shipped below $150, representing a substantial share of global volumes, with that proportion rising in key emerging markets like Africa and India, to nearly 60% and 30%. As rising memory costs render this price band economically unsustainable, the industry faces a reversal of a decade long trend in which consumers consistently received smartphones with better specifications at lower prices. Most low‑end–focused OEMs plan to defend share by cutting specifications or shifting volume above $200, but demand in that range remains limited across emerging markets, making it impossible to sustain current shipments. They will also face stronger competition from established brands at higher tiers, further limiting their ability to preserve volume and share. As a result, we expect a significant reduction of Total Addressable Market (TAM) through the current forecast period and a consolidation of the competitive landscape. Meanwhile, demand for budget smartphones will persist, pushing price‑sensitive consumers to either extend device lifecycles or turn to affordable used smartphones, where adoption is already accelerating. Consumers in some emerging markets could even revert to feature phones, reversing smartphone penetration gains as ultra-low end smartphones below $50 cease to exist. In short, the smartphone market is headed for a structural reset, in size, product mix, and competitive landscape.

The memory mix-down trend is particularly concerning for the AI PC category. Despite heavy marketing investment and the integration of dedicated Neural Processing Units (NPUs), AI PCs have so far failed to deliver on the transformative capabilities promised to consumers and enterprise buyers. The use cases remain narrow, and the software ecosystem has not kept pace with the hardware. Now, just as the industry needs to build a more compelling AI story around the PC, the memory crisis threatens to undermine the foundation required to do so. Local AI workloads, including the vision of the PC at the center of an Agentic AI future capable of managing and coordinating multiple AI tasks on behalf of the user, are inherently memory intensive. Shipping systems with less RAM does more than just limit today’s AI capabilities. It constrains the potential of these devices to run local models, manage context windows, and handle the data throughput that meaningful on-device AI will demand.

Tariff uncertainty adds another layer of risk

The policy environment is adding its own volatility. Last week, the U.S. Supreme Court struck down the broad reciprocal tariff regime imposed by the Trump administration, ruling that the executive authority exercised exceeded its statutory scope. The administration has since moved to levy a 10% across-the-board tariff on imports using alternative legal authority, and is working to raise it to 15.

For the device industry, this creates deep uncertainty. A 15% tariff on finished goods and components layers additional cost pressure on top of already-inflated memory prices. Vendors cannot plan pricing, sourcing, or inventory strategies with any confidence. Some costs will be passed through to consumers, compounding affordability challenges. Others will be absorbed by vendors and channel partners, further compressing margins.

Buckle up

The bottom line is that 2026 is shaping up to be another challenging year for the PC and smartphone markets. The confluence of a deepening memory supply crisis, aggressive pull-forward activity that has front-loaded volumes, rising ASPs that will suppress unit growth, and a volatile trade policy landscape makes precision forecasting extraordinarily difficult. Organizations across the value chain, from semiconductor suppliers to device OEMs to channel partners and enterprise buyers, should be planning for sustained turbulence. This is not a one-quarter disruption. It is a structural shift that will define the device market narrative well into 2027.