In December 2024, one year ago, Microsoft CEO Satya Nadella declared on the BG2 podcast that “SaaS is dead.” The comment set off a shockwave across the technology industry and many felt provoked. After all, software-as-a-service (SaaS) has defined enterprise computing for nearly two decades, representing a massive share (over 10% according IDC’s Black Book) of IT spending in 2024 and forming the backbone of digital transformation strategies worldwide.

Yet, when we cast a cold IDC analytical eye beyond the provocative statement, a crucial truth emerges: SaaS, as we know it, is being disrupted, not by decline but by evolution.

The Status Quo: SaaS at Its Peak

Today, most of the world’s leading software vendors are, in some form, SaaS companies. Among the ten most valuable software players, including Microsoft, Salesforce, Oracle, SAP, and Shopify, SaaS delivery models dominate. Enterprises have grown dependent on the SaaS ecosystem, licensing countless applications to manage HR, payroll, CRM, expenses, and vertical industry workflows.

However, the sheer sprawl of SaaS adoption has created complexity for business users. Employees navigate dozens of interfaces daily, shifting context between multiple systems that rarely communicate smoothly. Despite efforts to simplify workflows through integrations and APIs, SaaS remains a patchwork of interfaces and data silos, forcing users to adapt to the software rather than the other way around.

The Complexity Problem and the AI Opportunity

This complexity is the Achilles’ heel of the SaaS model. Each SaaS application demands its own learning curve and user interface, often used sporadically and inefficiently. In this environment, AI offers a compelling remedy.

Instead of navigating multiple dashboards, users could interact with agent-driven, conversational interfaces that perform tasks across systems. Imagine instructing an AI agent to “approve last week’s expense reports” or “generate next quarter’s sales forecast” and having the agent orchestrate workflows across HR, finance, and CRM systems behind the scenes.

This agentic, “flow-of-work” user experience could replace much of today’s direct interaction with SaaS applications. The result? AI as the new interface layer, which is one that abstracts away complexity, automates repetitive processes, and redefines how enterprises consume software.

The Disruption: From Seats to Outcomes

Such a shift has profound implications for how SaaS is bought and sold. The traditional per-user, per-month licensing model becomes increasingly obsolete as digital labor replaces manual interaction. IDC predicts that by 2028, pure seat-based pricing will be obsolete, with 70% of software vendors refactoring their pricing strategies around new value metrics, such as consumption, outcomes, or organizational capability (please see IDC FutureScape: Worldwide Agentic Artificial Intelligence 2026 Predictions, IDC #US53860925, October 2025).

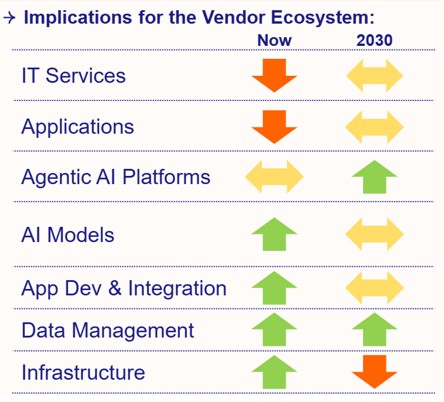

This agentic IT disruption will impact IDC’s existing forecasts for the various levels in the IT stack differently as shown below. Also, the impact will change over time, as for examples SaaS Applications and IT Services will feel a negative impact in the short term, while recovering if we look five years out to 2030.

For infrastructure hardware, IDC sees a different impact with a short term boost, followed by headwinds as inference costs drop exponentially.

Source: Charting the Agentic Future: 10 Vision Statements for 2030 (IDC #US53909225, November 2025)

Inside the enterprises, this evolution changes the economics of enterprise software. Companies optimizing AI agent development to reduce licensing costs will need to revisit their roadmaps as vendors adjust to these emerging pricing paradigms. Meanwhile, process owners may gain more flexibility, designing application-neutral operational efficiencies that transcend the limitations of current SaaS systems.

Business and IT Implications

The rise of AI agents doesn’t just alter pricing, it transforms how technology functions within organizations.

From a business perspective, enterprises may initially lose the tactical benefit of reduced software costs but gain strategic control over innovation and process optimization. Process teams will design workflows around end-to-end outcomes rather than application silos, supported by a new breed of “headless” software modules accessible via APIs and marketplaces.

From an IT standpoint, this means a fundamental re-architecture of the enterprise tech stack. Where today’s stack is built around SaaS interfaces, tomorrow’s will revolve around AI agents that interact with modular backend services. Data lakes and live data connections become critical enablers, while vendor relationships evolve from UI-centric engagement to agentic enablement partnerships.

Guidance for Technology Buyers

For IT and procurement leaders, this transformation demands foresight and experimentation. Buyers should assume that software vendors will increasingly position their offerings to accommodate or counteract the impact of digital labor.

Before adopting agentic systems, IDC advises enterprises to:

- Build proofs of concept (POCs) and define clear ROI metrics around cycle time, productivity, and revenue improvements.

- Evaluate end-to-end process efficiency, not just individual task automation.

- Explore packaged AI agents offered by existing SaaS vendors, integrating them as part of broader operational redesigns.

In other words, the transition to AI-driven enterprise software should be intentional, data-backed, and aligned with measurable business outcomes.

The Road to 2030: SaaS Reimagined

By the end of this decade, the enterprise technology landscape will look radically different. The AI agent will become a new enterprise SKU, purchased via marketplaces and powered by modular backend capabilities rather than monolithic SaaS platforms. User interfaces will still be critical to productivity but so will orchestration of more-or-less autonomous workflows.

SaaS is not dead, but it is metamorphosing. The software industry is entering a new chapter defined by AI, automation, and outcome-based economics. For vendors, it’s a challenge to reinvent their business models. For buyers, it’s an invitation to rethink how software delivers value.

Either way, the next generation of enterprise technology will be less about screens and more about agents.

Got a question? Drop it in here.

You may be interested in listening to IDC EMEA’s predictions for 2026 and beyond.