Key Highlights:

- By 2028, CIOs will increase spending on sovereign-ready cloud and data localization by 50% to stay compliant in Asia/Pacific.

- By 2030, 15% of A1000 firms will face lawsuits, fines, or CIO dismissals tied to poor AI agent governance.

- By 2027, AI infrastructure costs will run up to 30% higher than planned, forcing CIOs to expand FinOps practices.

- Most organizations still struggle to demonstrate consistent, measurable AI business value.

What is changing for CIOs in Asia/Pacific as organizations scale agentic AI?

Between 2026 and 2030, CIOs will be judged less on AI experimentation and more on their ability to operationalize AI securely, affordably, and in compliance with local regulations. IDC FutureScape research shows that success will depend on sovereign-ready architectures, transformational AI leadership, formal AI value playbooks, stronger governance of AI agents, and disciplined FinOps practices.

AI has become a board-level priority across Asia/Pacific (excluding Japan). Enterprises are under pressure to use AI to improve productivity, resilience, and growth, while navigating fragmented regulations, uneven cloud maturity, and persistent skills shortages.

For CIOs, the margin for error is shrinking. Poorly governed or poorly justified AI initiatives can quickly lead to cost overruns, regulatory exposure, or operational disruption. As a result, the CIO role is evolving beyond technology delivery toward enterprise leadership, financial accountability, and risk stewardship.

Five Predictions Defining the Shift to Agentic AI

1. Digital sovereignty

By 2028, CIOs at multinationals will boost investments in modular, sovereign-ready cloud and data localization environments by 50% to future proof operations against rising sovereignty demands.

Digital sovereignty is now a structural constraint on IT and AI strategy in Asia/Pacific. Expanding data localization and AI regulations in markets such as India, China, and Australia are forcing CIOs to move away from highly centralized global cloud models. Modular, sovereign-ready architectures allow organizations to localize data, models, and controls while maintaining operational consistency. Although this raises costs through redundancy and regionalization, it reduces regulatory risk and protects long-term market access.

2. Transformational AI leadership

By 2028, 70% of A500 CIO roles will be held by transformational leaders who can implement new AI-fueled business models with enterprise-wide consistency while modernizing IT to meet AI business needs.

As AI reshapes business models, CIOs are increasingly expected to lead enterprise transformation, not just IT modernization. In Asia/Pacific, where CIOs are more likely to report directly to the CEO, this shift reflects rising expectations that AI investments deliver measurable business outcomes. Transformational CIOs distinguish themselves by aligning AI initiatives with corporate strategy while modernizing core systems to support scale and resilience.

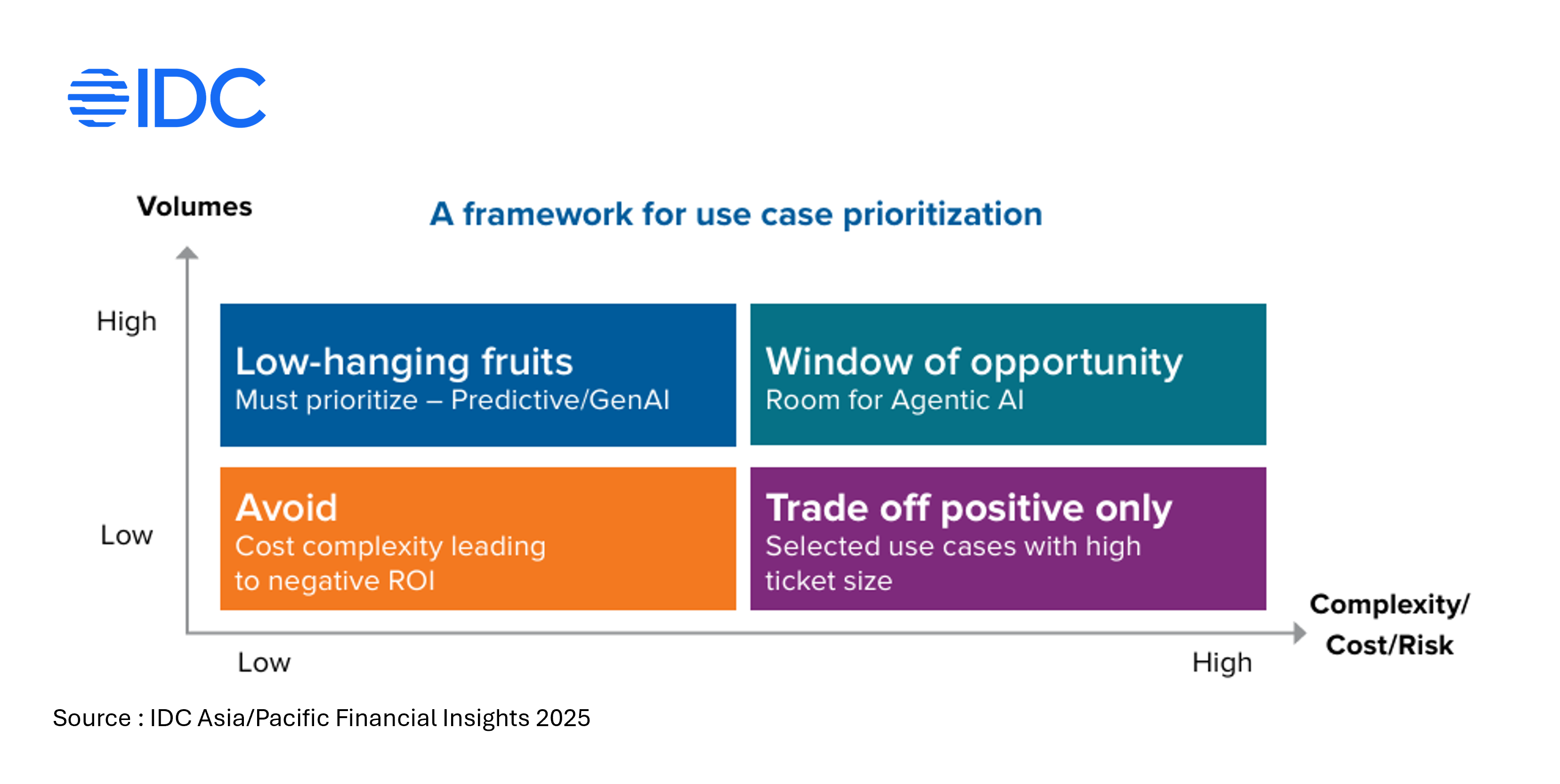

3. AI business value playbooks

By 2027, 60% of A500 CIOs will be tasked to create enterprise AI value playbooks, featuring expanded ROI models to define, measure, and showcase AI impact across efficiency, growth, and innovation.

Despite growing AI investment, most organizations struggle to prove consistent business value. Traditional ROI metrics fail to capture indirect benefits such as faster decision-making, improved customer experience, and resilience. AI value playbooks provide CIOs with a standardized framework to compare use cases, prioritize investment, and communicate impact to executives and boards, helping prevent pilot sprawl and loss of confidence.

4. AI business disruption impact

By 2030, 15% of A1000 organizations will have faced lawsuits, substantial fines, and CIO dismissals because of high-profile disruptions stemming from inadequate controls and governance of AI agents.

Agentic AI introduces new operational and regulatory risks as autonomous systems move into mission-critical workflows. In Asia/Pacific, unified AI governance remains limited, increasing exposure to outages, compliance failures, and reputational damage. CIOs are under growing pressure to implement stronger controls, human-on-the-loop mechanisms, and cross-functional governance before agentic AI scales further.

5. FinOps practices for AI

By 2027, A1000 organizations will face up to 30% rise in underestimated AI infrastructure costs, driving CIOs to expand the scope of FinOps teams to optimize expenses and enhance business value.

AI introduces volatile cost structures across cloud consumption, model training, and AI-infused applications. These costs are often underestimated, particularly in Asia/Pacific’s fragmented hybrid and multicloud environments. Mature FinOps practices are becoming essential to improve cost transparency, align AI spending with business priorities, and prevent unexpected overruns that undermine executive trust.

What Comes Next for CIOs in Asia/Pacific

Over the next three to five years, Asia/Pacific organizations will move from AI experimentation to industrialized, agentic AI operations. Investment will shift toward platforms, governance frameworks, and financial discipline that support repeatability and control. CIOs who establish these foundations early will be better positioned to scale AI while maintaining trust with regulators, customers, and boards.

Key Questions CIOs are Being Asked

- Why is digital sovereignty shaping CIO priorities now?

Regulatory enforcement is increasing across Asia/Pacific, making it essential for organizations to localize data and AI controls without sacrificing operational efficiency. - Why do AI initiatives struggle to show ROI?

Many organizations lack standardized methods to measure indirect and long-term AI benefits, resulting in fragmented pilots and weak executive confidence. - What is the biggest risk as agentic AI scales?

Inadequate governance of autonomous systems, which can lead to operational disruption, compliance failures, and executive accountability.

Explore IDC Research on the Asia/Pacific CIO Agenda and Agentic AI

For CIOs and technology leaders navigating AI at scale, IDC’s FutureScape research provides data-driven insight into how sovereignty, governance, cost discipline, and leadership expectations are reshaping the CIO role across Asia/Pacific.

- Download the full research report: IDC FutureScape: Worldwide CIO Agenda 2026 Predictions — Asia/Pacific (Excluding Japan) Implications

- Download the CIO Agenda 2026 ebook: Top Predictions and Insights for CIOs in 2026