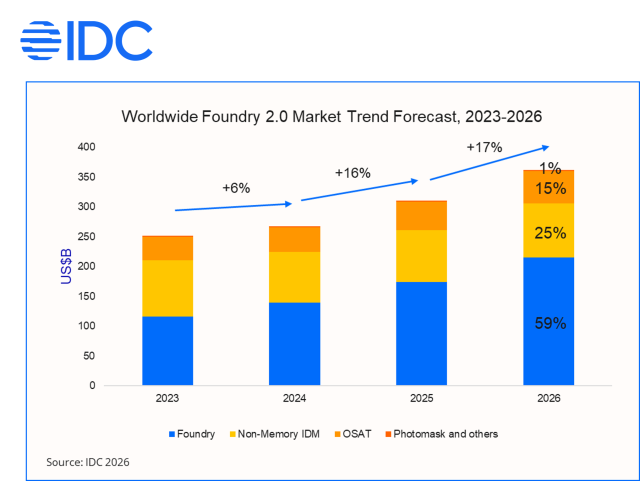

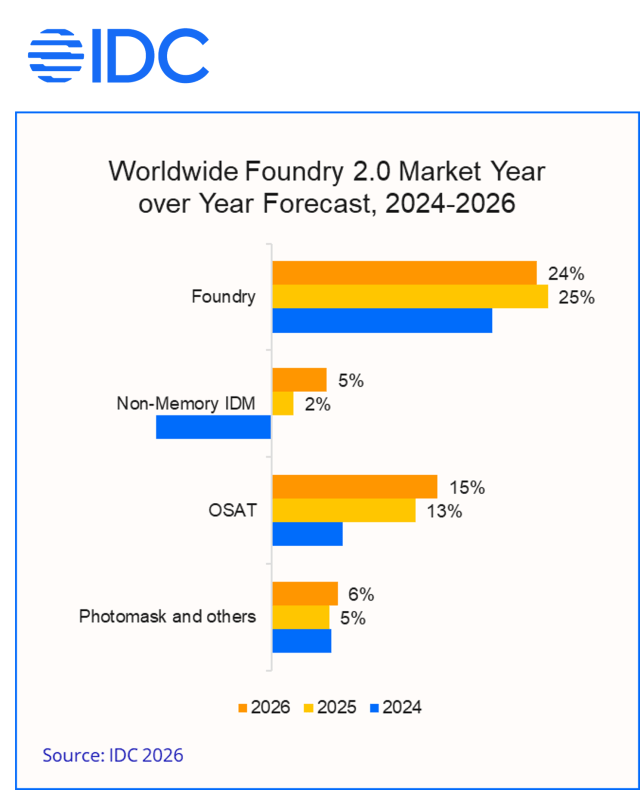

SINGAPORE, 30 March 2026 – According to IDC’s latest Global Semiconductor Supply Chain Tracking Intelligence, the broadly defined Foundry 2.0 market, comprising pure-play foundry, non-memory IDM, outsourced semiconductor assembly and test (OSAT), and photomask fabrication, is projected to surpass USD 360 billion in 2026, representing 17% year-over-year growth.

“The Foundry 2.0 market is entering a steady expansion cycle driven by AI in 2026. Advanced nodes and advanced packaging remain in short supply, while mature nodes are finally leaving behind the era of price competition, supported by accelerating 8-inch capacity reductions and resilient demand growth from AI power-related chips.” said Galen Zeng, senior research manager at IDC Asia/Pacific.

Note: Non-Memory IDM figures primarily reflect manufacturing output value for the segment.

Foundry Industry: TSMC Dominates Advanced Nodes, Mature Node Pricing Cycle Rebounds

Advanced node foundry is benefiting from strong demand from AI GPU and ASIC customers including NVIDIA, AMD, and Broadcom. Leading foundry, TSMC, has raised its 3nm monthly capacity target to 165,000 wafers and CoWoS monthly capacity to 125,000 wafers, with wafer pricing also raised by more than 5%. Supported by sustained full utilization at 3nm, the ramp of 2nm, and CoWoS advanced packaging order spillover, TSMC is expected to further expand its foundry market share to 44% in 2026. Samsung Foundry is also benefiting from gradually improving SF2 process yields, with the Exynos 2600 mobile processor and cryptocurrency mining chips entering supply, and 4nm HBM4 base die production commencing, driving higher advanced node utilization. On the customer front, Samsung holds a USD 16.5 billion long-term agreement with Tesla and has secured orders for AI accelerators including NVIDIA Groq 3 LPU, with order momentum recovering and overall operational trajectory improving.

On the mature node side, as both TSMC and Samsung initiate 8-inch capacity reductions and other mature node players plan 8-inch capacity optimization, global 8-inch total capacity is expected to decline approximately 3% year-over-year in 2026, marking a reversal in supply-demand dynamics. Continued strong demand for server Power ICs and Power Discrete components has prompted select foundries to raise wafer pricing by up to 10%, ending the post-pandemic race-to-the-bottom pricing environment. Overall, IDC forecasts the foundry market to grow 24% year-over-year in 2026.

Non-Memory IDM: Intel 18A Enters Production, Automotive and Analog IDM Supply-Demand Dynamics Improve

The non-memory IDM manufacturing segment is recovering in 2026, with estimated year-over-year growth of 5%. Intel is accelerating its process roadmap. The Panther Lake processor completed its first volume production shipments in late 2025, and the Clearwater Forest data center processor was officially unveiled at MWC 2026, marking the full entry of the 18A product line into mass production. On the external customer front, Intel’s 12nm collaboration with UMC is actively engaging potential customers for tape-outs, while leading US HPC companies have begun evaluating the 18A-P process, further supporting Intel’s gradual expansion of its customer base.

European automotive IDMs including Infineon, NXP, and STMicroelectronics have completed inventory corrections, with demand expected to gradually recover. Some players are also adopting “China for China” localized manufacturing as a strategic option to manage geopolitical risk, deepening their presence in the Chinese market through joint ventures or contract manufacturing with domestic fabs, generating additional growth momentum. Among US IDMs, Texas Instruments continues to see industrial demand recovery, with automotive business maintaining steady growth.

OSAT Industry: CoWoS Spillover Accelerates ASE Order Intake, OSATs Compete for Advanced Packaging Opportunities

The OSAT segment is projected to grow 15% year-over-year in 2026, supported by recovery in both advanced and mainstream packaging markets. The AI chip integration trend continues to elevate the value-add of advanced packaging, with back-end packaging design and system integration now rivaling front-end wafer fabrication in strategic importance. ASE Technology Holding (ASE) is a key driver of the current AI packaging wave, with growth momentum primarily stemming from sustained CoWoS capacity shortfalls at TSMC and the gradual increase in outsourcing share, driving continued volume ramp in on-substrate packaging (oS) and chip probe (CP). Looking ahead, post-package test (FT/SLT) and full-process packaging are expected to become the next growth engines, with AI CPU and AI ASIC products progressively entering the pipeline and further expanding ASE’s growth runway in advanced packaging.

Overall, the global OSAT market is benefiting from multiple tailwinds including compute expansion, the proliferation of heterogeneous integration architectures, and the recovery of automotive and industrial end markets. Rising costs for key packaging materials, including leadframes and substrates, are prompting vendors to renegotiate pricing with customers, pushing overall ASP higher and supporting industry revenue growth. Taiwan and China-based players collectively account for over 70% of global market share, dominating this wave of industry expansion.

“Looking ahead to 2026–2030, the Foundry 2.0 market is projected to achieve a CAGR of 11%, with the long-term capex cycle in AI infrastructure serving as the core engine of sustained industry expansion. However, the ripple effects of semiconductor inflation, the impact of the memory supercycle on downstream end demand, energy supply instability driven by geopolitical conflicts, the evolving policy direction of the US Section 232 investigation, and supply chain restructuring driven by China’s accelerating semiconductor self-sufficiency will all be critical variables shaping the industry’s medium-to-long-term trajectory.” added Zeng.

###

About IDC

International Data Corporation (IDC) is the premier global provider of trusted technology intelligence, advisory services, and events. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 100 countries. IDC’s analysis and insights help IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. To learn more about IDC, please visit www.idc.com/ap. Follow IDC on X and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

Click here to explore IDC’s full suite of data and research, and discover how they can help grow your business.