BOSTON, March 3, 2026 – Global security spending is projected to reach $308 billion in 2026 and $430 billion by 2029, according to the latest forecast from the International Data Corporation’s (IDC) Worldwide Security Spending Guide. The global security market is forecast to grow 11.8% in 2026, driven by increasing investments into unified, AI-driven security platforms and related services.

Global Security Market at a Glance

- Total security spending: $308 billion (+11.8% YoY)

- Software: Largest tech group, >50% of spend

- Software: Fastest growth, +14% YoY

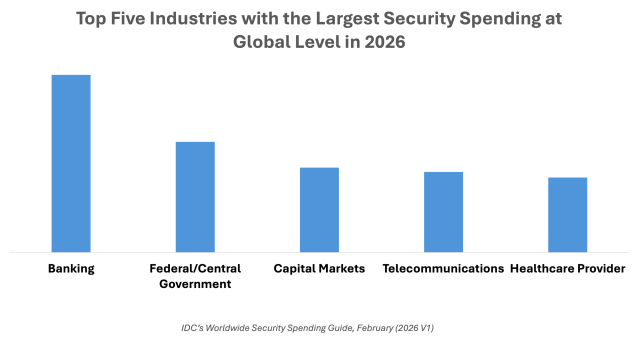

- Top industries: Banking, Federal/Central Government, Capital Markets

- Fastest-growing industries: Capital Markets, Media and Entertainment, Software and Information Services

- Leading regions: USA ($150 billion), Western Europe ($69 billion), APeJC ($26 billion)

- Fastest-growing regions: Middle East and Africa, Latin America, USA

What Are the Main Technology Drivers for Security Spending?

The largest technology group in 2026 is projected to be Software, accounting for more than half of the worldwide security spending. Identity and Access Management Software, Endpoint Security Software, and Security Analytics are expected to represent more than 50% of global Security Software spending this year. As threats—including those fueled by AI —become increasingly sophisticated, companies are prioritizing these tools to prevent breaches, protect critical assets, and gain actionable visibility across their environments.

Software is also forecast to be the fastest growing technology group in 2026, with an estimated year-over-year growth rate of 14% in 2026. Services are projected to follow closely, likewise expected to see double-digit growth this year. Cloud Native Application Protection Platform (CNAPP), Identity and Access Management Software, and Information and Data Security Software will be the fastest growing Security Software technology categories. These technologies constitute the essential defense necessary to protect AI workloads, verify the identity of a non-human workforce, and ensure data safety in an era of AI-driven threats.

Among Services, Managed Security Services are expected to see the highest growth this year, allowing companies to help bridge the gap between escalating cyber-complexity and the persistent global shortage of in-house security talent.

“Organizations are moving beyond isolated security tools toward more integrated and intelligence-driven security architectures as threat complexity, regulatory pressure, and AI adoption accelerate,” says Monika Soltysik, senior research analyst, Security & Trust at IDC. “Investment is increasingly focused on technologies that improve visibility, automate response, and strengthen identity and data protection across hybrid and cloud environments. Over the next several years, security strategies will increasingly prioritize operational resilience and platform consolidation as organizations seek measurable risk reduction rather than incremental tool expansion.”

Key Global Dynamics

The global security market is shaped by AI-driven threats and increasing complexity of cyberattacks, prompting higher investments by companies in advanced security solutions. Geopolitical tensions and state-sponsored cyber operations are also intensifying risk and driving cross-border security spending. The United States will lead worldwide security spending in 2026, reaching $150 billion, driven by significant investments by the Financial Services, Healthcare, and Government industries. Western Europe will be the second largest market at $69 billion, pushed by intensifying regulatory and compliance requirements (e.g. NIS2, DORA, AI Act). APeJC will rank third with $26 billion, as rapid digital transformation and cloud adoption in the region will in turn trigger the required investments in security.

What Are the Key Industry Trends in Security Spending?

Banking, Federal/Central Government, Capital Markets, Telecommunications, and Healthcare Provider will be the top five industries in terms of global security spending in 2026, accounting together for more than one third of the total.

Capital Markets, Media and Entertainment, and Software and Information Services will be the fastest growing industries for security spending in 2026. Capital Markets will still be one of the primary targets for ransomware, fraud, and AI-driven cyberattacks – zero trust adoption, regulatory compliance automation, and AI-driven threat detection will be at the core of the security strategy of companies in this industry.

Media and Entertainment companies significantly rely on digital content distribution and cloud platforms and will increasingly focus their security investments on IP protection, piracy, and service disruption. As Software and Information Services companies are responsible for managing large-scale cloud infrastructure and client data as well for protecting the whole AI supply chain, a significant amount of spending will be dedicated to DevSecOps, CNAPP for multi-tenant environments, identity and access management solutions to secure users and services across platforms, and security analytics and automated incident response to handle large-scale threats.

Other relevant mentions include Aerospace and Defense and High Tech and Electronics. Given their high exposure to cyber espionage and nation-state threats, the two industries will continue increasing their investments in intellectual property and sensitive data protection throughout 2026. Supply chain security and third-party risk management will still be crucial for them to mitigate vulnerabilities across complex, global production ecosystems. Finally, the growing convergence of IT and OT environments will continue to drive demand for advanced protection of connected manufacturing systems and industrial infrastructure.

“The ongoing rise in cyberthreats and regulatory pressure will continue to drive global demand for resilient, sovereign, and compliant cybersecurity capabilities,” says Stefano Perini, research manager, Market & Industries at IDC. “The strongest growth in security spending in 2026 is expected in the industries where protecting sensitive data, intellectual property, and critical infrastructure is most essential, and where the need for industry-specific security solutions is greatest. The growth will be greater for large companies, but it will also be significant for medium-sized and small enterprises, which are realizing that security is becoming an essential business enabler for them as well.”

About IDC Worldwide Security Spending Guide

IDC’s Worldwide Security Spending Guide quantifies both core and next-generation security spending for 28 industries and five company sizes across 38 technology markets and 48 countries.

About IDC

International Data Corporation (IDC) is the premier global provider of trusted technology intelligence, advisory services, and events. With more than 1,000 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 100 countries. IDC’s analysis and insights help IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. To learn more about IDC, please visit www.idc.com. Follow IDC on X at @IDC and LinkedIn. Subscribe to the IDC Blog for industry news and insights.

All product and company names may be trademarks or registered trademarks of their respective holders.