Worldwide Enterprise External OEM Storage Systems Market Spending showed a 22.9% growth in Q1 2026 and is expected to grow an average of 7.3% over a 5-year period, according to IDC

The worldwide external OEM enterprise storage systems (ESS) market delivered a sharp acceleration in the first quarter of 2026, reaching $9.9 billion in spending, a 22.9% year-over-year increase compared to the same quarter of 2025. The result represents an important acceleration from the 3.9% full-year 2025 growth rate and the 5.5% expansion recorded in the fourth quarter of 2025, reflecting the convergence of deferred infrastructure refresh spending, component price inflation, and AI-driven storage demand.

The enterprise storage market, which spent much of the prior two years in the shadow of explosive server and GPU investment, is now benefiting from two reinforcing tailwinds: enterprises refreshing storage infrastructure that was deferred while AI server spending took priority, and a new wave of AI-driven storage demand emerging from training pipelines, inferencing workloads, and unstructured data activation use cases. Component supply constraints, particularly for NAND flash and DRAM, continue to push system-level prices upward, further amplifying revenue growth beyond what shipment volumes alone would suggest. Thus, the market is expected to continue in a positive trajectory of 7.3% compound average growth through 2030.

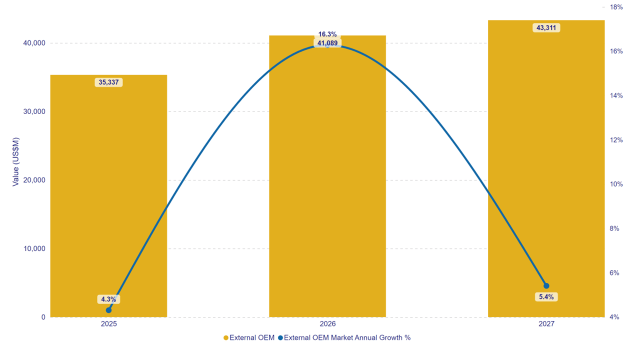

| Data – Year | External OEM | External OEM Market Annual Growth % |

| 2025 | $35,337 | 4.3% |

| 2026 | $41,089 | 16.3% |

| 2027 | $43,311 | 5.4% |