At the IDC Quanta launch webinar, Joe Bradley, CTO at IDC, made the case for why trusting an AI-powered answer shouldn’t require faith; it should require an architecture you can actually inspect. You’ve heard “AI-powered” enough times this year that a healthy dose of skepticism is the right response. Fair. So instead of asking you to trust that IDC Quanta gets its answers right, here’s what Bradley says is actually happening under the hood when it does.

Bradley breaks it down into two layers. The first is an MCP server: essentially a pipe that gives Claude direct access to IDC’s data, the trackers, the forecasts, the market figures. It also carries instructions for how that data is structured and how to use it. The second is IDC’s own Claude plugin, which goes further, Bradley explains. It shapes how the AI reasons about that data, tells it what’s relevant for what purpose, and requires it to surface a source before handing over any answer. Put together, when someone asks a question, Claude isn’t searching a phrase in a database, Bradley says. It’s reasoning with IDC’s own methodology built into the process.

That’s the theory. Here’s what it looks like in practice.

The Moment It Earned Trust

In the product demo, Bradley walked through a scenario: an FP&A analyst building a market forecast ahead of a CFO review, projecting 16% growth in a segment his company competes in. He asked IDC Quanta to check that number against an external benchmark, right inside Excel.

In under a minute, Quanta surfaced IDC’s actual forecast for that market: 12.1% growth through 2029, with the category decelerating to single digits in the later years. His model hadn’t caught up to where the market was actually headed. That’s the payoff of the architecture above. The answer arrived with its source attached.

Why Even Build an App

Technical buyers reasonably ask why IDC needs its own app when Claude and ChatGPT already exist. IDC isn’t positioning itself as a competitor to the assistants people already use daily. It’s building something with a narrower job.

The case for IDC Quanta comes down to control over how IDC’s own data gets handled and delivered. It exists because of what only a dedicated app can guarantee: a single place that collects everything relevant across an IDC relationship, a direct line to a live analyst when the automated answer isn’t enough, and data handling built on tenant isolation, enforced access controls, and audit logs that capture every user action. Which raises the next question technical buyers ask first.

Provenance You Can Check Yourself

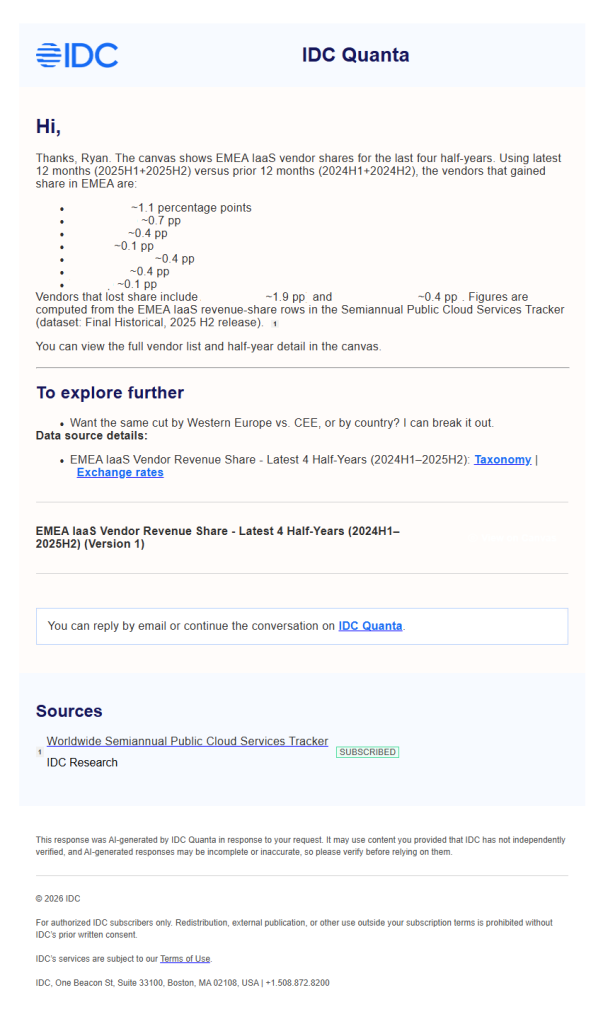

Bradley’s last test for anyone skeptical of AI-generated answers is provenance. Can you verify where it actually came from? In a second demo, he showed IDC Quanta processing a strategy document sent over email, then breaking its answer down into cited data cuts, each one tied explicitly to the filters and definitions behind it.

Nothing here is asserted without a source attached, and nothing requires trusting the AI’s summary over the underlying data itself. That’s the actual answer to “how do you know it’s not confidently wrong”: you don’t have to take Quanta’s word for it. You can check.

See It Yourself

The architecture, the demo, and the sourcing are easier to evaluate firsthand than to take on faith. Request a demo, or talk to your IDC account team if you already have one.