Climate Week

From September 22-29, New York City hosts Climate Week, an annual event that brings together global leaders, policymakers, businesses, and civil society to tackle the pressing challenges of climate change. The week features a series of conferences, workshops, and exhibitions to promote sustainable practices, address climate justice, encourage international cooperation, and raise public awareness. Each year, we are reminded that the past 12 months have marked yet another “Top 10” high for global temperatures, emphasizing the urgent need for action—though the pace of change remains frustratingly slow.

The Data Center Dilemma

The data center industry has come under increasing scrutiny for its environmental impacts and rapid growth, driven partly by AI technologies’ energy demands. For example, in its sustainability report released in May, Microsoft said its emissions grew by 29% since 2020 due to the construction of more data centers designed and optimized to support AI workloads. Likewise, Google reported increased electricity demand driven by artificial intelligence, and its growing fleet of data centers has caused the company’s greenhouse gas emissions to grow by 48% above its 2019 baseline, creating a challenge for the tech giant in meeting its carbon neutrality goals by 2030.

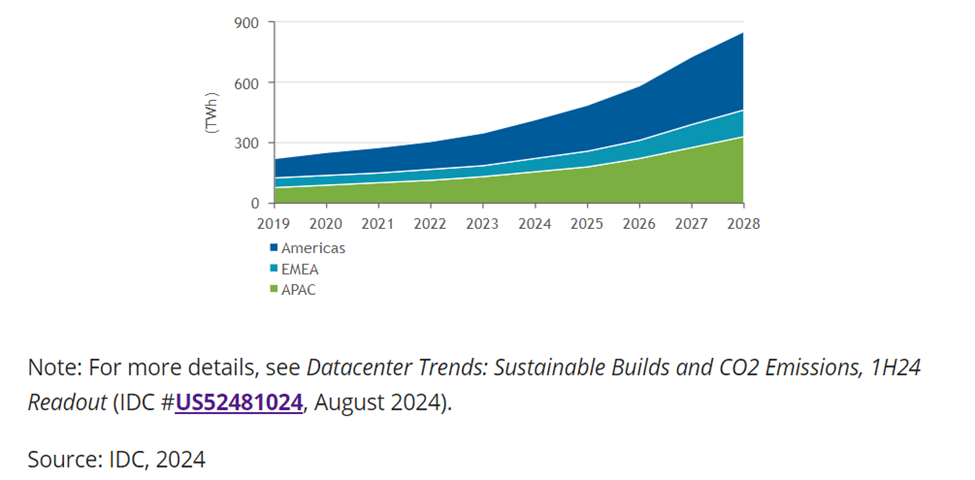

These companies should be applauded for their transparency and courage to tell the facts as they are. It demonstrates leadership, promotes learning and improvement, encourages industry standards, and, most importantly, highlights the problem. This ever-increasing facility growth and electricity consumption poses a significant struggle as data centers strive to balance the need for increased computational power with the imperative to minimize their environmental footprint. IDC calculates worldwide data center energy consumption for 2023 to be 352TWh and projects a 19.5% CAGR, growing to 857TWh by 2028.

While harder to quantify due to of a lack of standards and available information, scope 3 emissions from constructing and outfitting data centers with IT equipment also contributes to industry emission growth.

Why Aren’t We Seeing More Progress?

While AI garners most market attention, when surveyed, datacenter operators indicated that improved environmental sustainability was their second-highest initiative, ahead of AI, but behind business and financial management.

So, if the data center operators know and prioritize the problem, why isn’t more progress being made?

Like most complex problems, there are a multitude of factors that contribute to it.

- Demand – The first is the demand for digital services. As enterprises pursue digital transformation and invest in artificial intelligence to create unique value, the demand for data centers and the associated electricity consumption is rising substantially. Organizations are unwilling to sacrifice operational improvements and gains they expect from these efforts to meet sustainability goals.

- Global political cooperation and policy. It will take a combination of political agreements, like the Paris Agreement, and stricter local regulations on emissions to drive the change in behavior and investment in renewable energy infrastructure.

- Transition to Renewable Energy. As governments and businesses set ambitious targets to reduce carbon emissions, the demand for renewable energy is outpacing supply, and globally, electric demand is outpacing new generation supply. Many electricity grids were built for centralized, fossil-fuel-based power generation and are not yet fully optimized to handle the decentralized and intermittent nature of renewable sources like wind and solar.

Taking Immediate Steps on Energy Efficiency

The phrase “Think globally, act locally” has been part of our collective consciousness since the 1970s, resonating across various societal challenges due to its timeless relevance. Today, this principle particularly applies to datacenter operations. While most datacenter operators may not have the influence to shape global policies or invest directly in large-scale renewable energy initiatives, they can drive change by focusing on energy efficiency at a local level to reduce demand.

While some companies or individual executives prioritize sustainability metrics, viewing environmental responsibility as a critical driver of their decisions, others see these efforts as secondary or “soft” benefits. For this latter group, decision-making is anchored in hard financial metrics, focusing on return on investment (ROI). Energy efficiency initiatives appeal to both types and are aligned with top datacenter priorities.

Electricity costs account for the most significant portion of data center facility operating expenses—ranging from 45% to 60%—depending on location and data center type. Simultaneously, growth in industrialization and electrification have led to higher electricity demand, outpacing generation, which is expected to cause electricity prices to increase. The combination of rising electricity prices and increased electricity consumption is poised to make data centers significantly more expensive to operate.

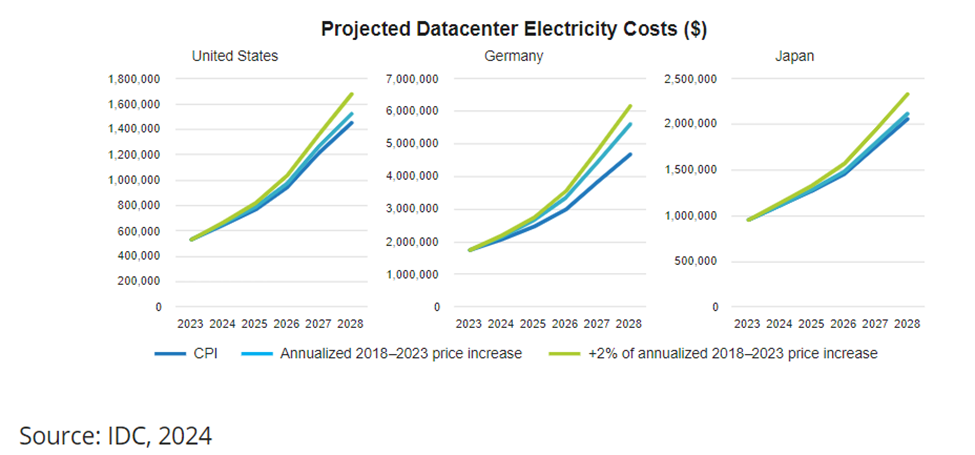

To assist organizations in understanding the potential impact, IDC published The Financial Impact of Increased Consumption and Rising Electricity Rates in Data Center Facilities. The research includes scenario planning for a 1 MW data center in the United States, Germany, and Japan. IDC projects that a typical 1 Megawatt data center consumed 6.6 Gigawatt hours (GWh) of electricity in 2023 and will grow to between 13 to 16 GWh by 2028 through capacity expansion, increased utilization, and higher density deployments. Simultaneously, IDC expects energy costs to continue to grow above historical levels. The percentage growth in electricity spend will exceed a CAGR of 15% in all cases, with most scenarios showing growth of over 20%. When measured in absolute spending increase, it is expected to near or exceed $1,000,000 annually.

While the model assumes energy efficiency improvements, an organization can expect to save between $500K and $1,900K with energy efficiency improvements that are 10% greater than the industry average.

Conclusion

Prioritizing energy efficiency in data centers is no longer just a matter of environmental responsibility—it’s essential for sound datacenter financial management. As the demand for digital services, AI, and cloud computing continues to soar, the pressure on organizations to minimize their carbon footprint while managing rising electricity costs will only intensify. By taking action now—investing in more energy-efficient technologies and optimizing operations- organizations can reduce their environmental impact and significantly cut operating expenses, their top two priorities. The financial and environmental stakes are clear, and the time to act is now. Energy-efficient data centers are essential for the future of business and the planet.