Interested in account-based marketing? Be sure to check out IDC’s on-demand webinar The Company is the Key: How Account-Level Intelligence Helps You Gain Share.

Why Competitors Matter to Your Account-Based Marketing Effort

Account-based marketing (“ABM”) is a strategic B2B marketing approach that targets a single company, division, or individual within a company. As such, it deploys far more targeted tactics than general marketing, designing campaigns around names and emails, individualized value propositions, and highly specific personas.

If your firm is engaged in ABM, it’s guaranteed your competitors are as well. This means you need to know what they are saying, how they are positioning themselves, and how they are engaging their prospects and clients so you can better align your own efforts.

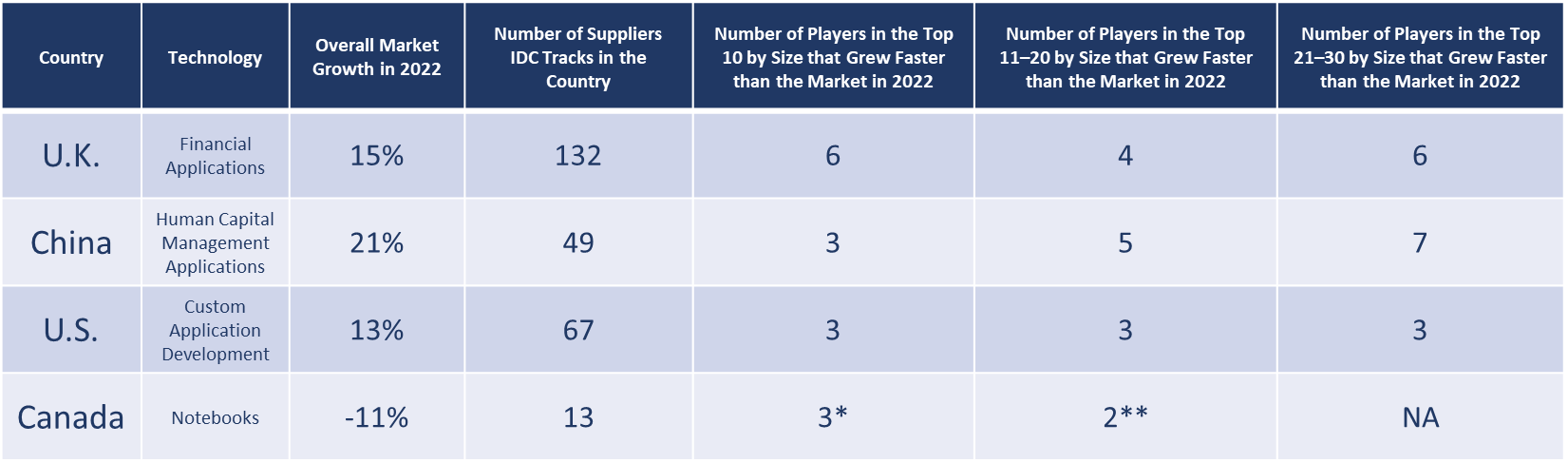

Getting started by identifying the competitors you need to analyze can be a formidable task in crowded IT markets. Granted, for some technology areas, the number of true players is small enough that everyone knows who they are. For instance, in the Canadian market for notebooks, five manufacturers hold more than 85% of the market value.

Identify Key Competitors In Busy IT Markets

For many IT markets, however, the list of competitors is long. For instance, in the U.K., IDC tracks more than 100 players in the market for financial applications. While the top 10 control around 58% of the market, the next 10 control less than 15%, leaving lots of room for ambitious software houses.

In China, the market for human capital management software is wide open, with the largest supplier holding less than 10% of the market. In the U.S., the market for custom application development is both enormous and fragmented, with the top 10 players accounting for only one-third of the value. In all three markets, there are lots of fast-growing players aiming to break into the top 10.

Figure 1: Market Analysis Example

To do ABM right, you need to identify the largest players and the fastest growing players both at the top of the market and in your revenue range. You then analyze their strategy and tactics for best practices and pitfalls.

* Only one supplier grew; the other was simply less negative.

** There are only 3 vendors in the top 11-20. Only one supplier grew; the other was simply less negative.

Source: IDC, 2023

Focus Attention on Priority Competitors

With so many tech suppliers, it can be hard to know on which of your competitors to focus your analysis. This is where market data comes in. IDC believes there are three primary ways you can use data to identify competitors worth your scrutiny:

- Competitors Outperforming the Market: While you will already be aware of your largest competitors, it can be extremely useful to rank them by share. This reveals who has the most visibility and the messaging and approach you’ll need to position yourself against. You should also rank them by growth, as this is a strong indicator of the effectiveness of their go-to-market strategy, including ABM. For instance, in the U.K. market for financial applications, only two of the top 5 gained share in 2022. The rest lost share.

- Fast Growing Competitors In or Near the Top 10: IT suppliers that are rapidly gaining share are doing something right. For smaller companies, a good year can give the illusion of exceptional growth. IDC therefore recommends looking at the fastest-growing suppliers in the top 20–30 (depending on the market), as these organizations are usually large enough to be dangerous. Returning to the U.K. market for financial applications, half of the top 20 software providers expanded much faster than the market; it’d be a good idea to catalog their ABM strategy and tactics for best practices.

- Fast Growing Competitors In Your Revenue Range: If you are among the top performing tech suppliers or a fast-growing company nearing the top 10 or 20, the two points above have you covered. But if you are further down the list, identifying which firms in your revenue range are growing fast tells you who to watch out for — and perhaps who to emulate when it comes to ABM. In Germany, IDC tracks around 70 firms trying to steal share from SAP in the supply chain management space. In 2022, in the $2–5 million revenue range, five beat the market by significant margins. If you were in that range, these five would be worth examination.

In short, the right data can help you quickly identify which of your competitors to analyze for ABM best practices and the positioning and messaging to set yourself apart.

IDC Company Lens provided the data for this post.

Get Started With ABM Resources and IDC Data

ABM planning can be a time consuming and challenging process to get right, especially the first time. To help organize your thinking and make key decisions you can use this account-based marketing starter guide. This step-by-step guide can help you bring together marketing and sales teams to develop a cohesive ABM campaign by asking the right questions and identifying the necessary insights for planning.

Whether you are approaching ABM from the perspective of marketing or sales—or through indirect or direct business channels—in today’s economic climate, objective insight and expert advice about buyers, partners, and competitors is vital to inform and accelerate decision making, campaign production, and account planning cycles. IDC Data & Analytics offer a broad array of solutions which detail company and ecosystem dynamics for the global tech market and that matter most to answering critical ABM planning and execution questions.

To get in contact with us to book a demo, please reach out here.